-

@ 4d41a7cb:7d3633cc

2025-02-25 13:53:41

Money is more abstract than most people think, as I will show in this article. Debt slavery stems from financial illiteracy, which occurs intentionally. The biggest secret is how bankers actually create **currency claims out of thin air and transfer the wealth of their clients (including nation states) to themselves for free without risking a cent, real money, or currency.**

## **MONEY**

Money, one of the most important things in our lives, is so important that we exchange wealth to obtain it. Not because we want it but because we need it in order to buy food, shelter, clothes, etc.

Money is not inherently bad, although some may argue that the love for money is the root of all evil, and I'll agree. If you are willing to sacrifice your soul, honor, reputation, family, or friends for money, it indicates a lack of morality and a willingness to engage in harmful actions to satisfy your greed and materialistic desires.

**Money is a technology, a tool, and like any tool or technology, it is impartial**; it cannot be inherently good or bad. It can be used to help others or to destroy them. At the end of the day, it’s all about the intention behind human behavior.

Money is not just a useful tool; it’s **the most important tool** to have for global commerce, division of labor, specialists, and the level of sophistication and comfort we achieve as humanity. All of this will not be possible without this tool working as a common medium of exchange and standard of value, a common language for all humanity: the language of monetary value.

**Money is the cornerstone of civilization.** Money is the bloodstream of commerce, and commerce is the spine of civilization; it’s what made our civilization so prosperous, letting any one of us decide how we want to provide value to society.

Money is half of every transaction, and since we will always need to intermediate between every exchange, money is the perfect intermediary to help achieve millions of different combinations of exchanges. It will be practically impossible to barter on a global scale; even in a small community with a few different products, it will be a mess.

For example, if there were 10 products, there would be 45 combinations; if there were 100, there would be 4950 combinations. Imagine a scenario on a large scale, requiring the exchange of hundreds of thousands of products every second..

This issue **necessitated the development of a new technology: money, which in turn led to the emergence of moneychangers (v4v). Money is a tool to exchange, measure, and store wealth.** Wealth is anything we can sell: our labor (time and energy), our house, a car, a product, a service, etc.

**Gold and silver were money for thousands of years** because of their unique characteristics of scarcity, durability, divisibility, and transportability. The most important characteristic of these metals is that they are scarce, and they can’t be created out of thin air or reproduced with no effort.

**Only God can control the supply of gold and silver found in nature.** Men can only extract it, and it requires investment, work, time, and effort to find and mine it. So the common knowledge and the common sense of the people over thousands of years consensually chose gold and silver as money. And **this money is the only lawful money under common law.**

> “Gold is money, everything else is credit”

>

> J.P. Morgan 1912

As an interesting fact, the word "money" is used 140 times in the King James Bible, the word "gold" is mentioned 417 times, and the word "silver" over 320 times. But the word “currency” is not mentioned a single time.

The most important function of money is to **exchange and store your time and energy**. You work to acquire money and then use that money to acquire other goods and services.

**Our time and energy is our real wealth** because it’s limited. We all have a limited time on earth, and we can do certain things in the 24 hours we have every day, so we have to be conscious about how we administrate and store the fruits of our labor.

Money is a means to an end; we don't want money; we want what money can buy, and guess what, money cannot buy more time.

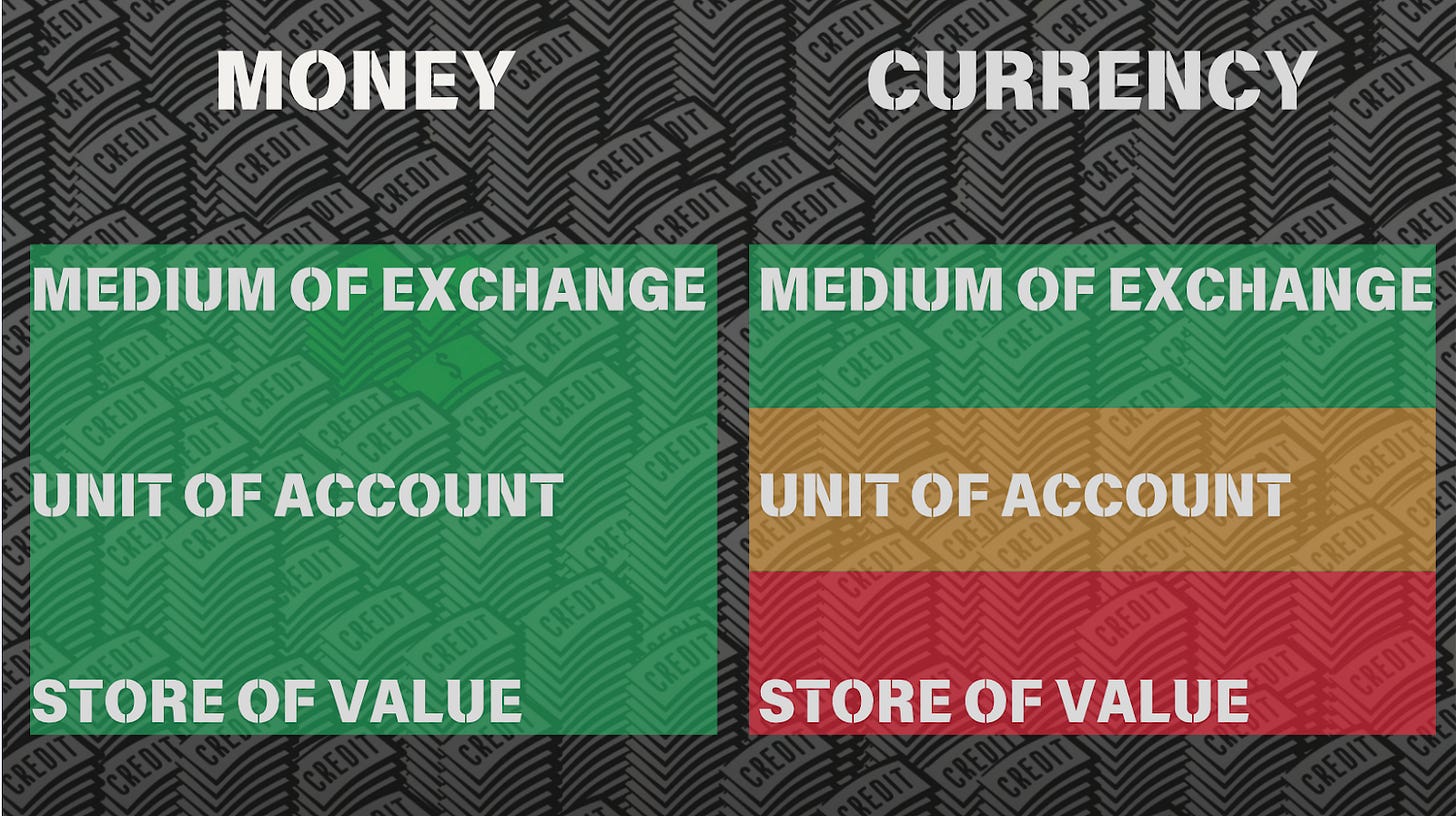

## **CURRENCY = FAKE MONEY**

**Currency exists as a money substitute.** Currencies began as the opposite of money, the **promise to deliver money in the future: debt**. Currencies can be used to exchange wealth, but they are not a fair unit of account and are never a good way to store it because men are tempted to create more and dilute its value (a process known as inflation)

Currencies have almost all the same characteristics of money, but there’s a big difference: **currency is not scarce and durable**. Missing the store of value characteristic of money, since **its supply can be manipulated by men.**

For wealth preservation and measuring, modern currencies make no sense. Men control the supply of currency; **banks and governments can inflate or deflate it in any amount they please, giving them supreme power and control over wealth distribution.** This creates two classes of citizens: those who work to acquire currency and those who create it instantly and for free.

International banks have stolen money (gold and silver) over the past century, replacing its supply with currency or fake money (paper receipts). \[1913, 1933, 1944, 1971\]

Under this monetary game, those with "fixed income," savers, and creditors are the biggest losers, while debtors and asset owners are the winners..

The **most important distinction to keep in mind is that nature controls the money supply, making artificial inflation impossible.** On the other hand, men can inflate currency in unlimited amounts. It is **a manifestation of God's power on earth, as the mediums of exchange serve as the lifeblood of commerce, the backbone of our economic system, and facilitate the division of labor.**

If someone can **inflate the currency supply, this has the same economic effect as counterfeiting,** and he’s effectively stealing from everyone contracting, trading, and saving in that currency. Manipulating the mediums of exchange in an economy enables manipulation of every security, industry, and business.

This is the reason the founding fathers of the United States made gold and silver only lawful money for the payment of debts. To give everyone equal protection under the law and to get rid of the nobility and two types of citizens: bankers and workers or nobles and plebeians.

> Bank-notes are not money. It 's currency. It’s unfair to take banks' currency as a standard for comparison.

>

> Bank-note currency is not “lawful money”. It never could be counted as part of banks cash reserves. ***It would be too much like a man writing and signing his own promissory note for a million and then claiming that this made him a millionaire.***

>

> The very grave evils any currency depreciation always impose upon businesses and the people.

>

> Alfred Owen Crozier, US Money vs Corporate currency, 1912

So money has three very important functions that work as the pillars on which the wellness of our economic system and civilizations relies. Currency is not a store of value because its supply can be easily manipulated, men in power can create more of it, and so using this always-changing currency as a standard of value or a unit of account is like using an always-changing ruler to measure distance. A dollar today does not buy the same as a dollar one year ago. So yesterday prices are not equal to today's prices; this is an unfair business calculation.

So money has three very important functions that work as the pillars on which the wellness of our economic system and civilizations rel**ies. Currency is not a store of value because its supply can be easily manipulated**, men in power can create more of it, and so using this always-changing currency as a standard of value or a unit of account is like using an always-changing ruler to measure distance. **A dollar today does not buy the same as a dollar one year ago**. So yesterday prices are not equal to today's prices; this is an unfair business calculation.

There are several Bible verses that discuss the manipulation of weights and measures, emphasizing the importance of honesty and fairness in commercial dealings.

1. Leviticus 19:35-36 New International Version (NIV): "**Do not use dishonest standards when measuring length, weight, or quantity.** Use honest scales and honest weights, an honest ephah, and an honest hin.

2. Deuteronomy 25:13-15: Do not have two differing weights in your bag—one heavy, one light. Do not have two differing measures in your house—one large, one small. **You must have accurate and honest weights and measures**.

3. Proverbs 11:1—"A "**dishonest scale is an abomination to the Lord**, but a just weight is his delight."

**Fake money (currency) is always and everywhere a dishonest scale.** So if you want a real measure of value or wealth use something with real value instead, like gold, commodities, products, times, etc.

Bankers have redefined the word money to mean fake money, currency, or debt. And this is not the worst part. Let’s introduce another concept: credit.

## **CREDIT = FAKE CURRENCY**

**Real credit is the promise to pay money in the future.** It involves delaying the payment of money. **Currency was born as credit**, as a money certificate or receipt. During the last century, banks gradually replaced 100% of the money with currency and bank credit to further boost their profits and control. \[1913, 1933, 1944, 1971\]

But in order to achieve this goal, **bankers redefined the word money to mean the opposite of money: credit/debt. This is like calling a night a day or evil a good.**

When you take out a loan from a friend, you receive credit from him, but you also incur a debt with him. You promise your friends that you will pay them (asset/right), and you owe them (liability/obligation). The asset and the liability are one and part of the same deal; they cannot exist without the other. There’s no credit with no debt, no debt with no credit, and no liability with no asset.

Federal Reserve notes, commonly known as **“dollars,”** are a private corporate currency; they are **not money** because they are not gold or silver, nor receipts for these metals as many people still believe. They were not redeemable in money from the start, despite being created under the assumption.

The “peso” (Spanish word for weight) used to be a standardized amount of gold or silver, but it’s not any more; it's just a debt denomination. And what's owing? Currency. **How can someone lend the opposite of money and charge interest? O**nly deceiving you into believing that he is lending you money. So they redefined the word money to mean the opposite of it.

But redefining words does not change the economic effect of the transaction.

When currencies first appeared, I can imagine people asking themselves, "How can people trust these paper certificates in exchange for their money?" Who will be that stupid?” And **nowadays, people don’t understand the difference between money and currency, to the point that bankers redefined the word "money" to mean the opposite of "money."**

Lesson: Money is not just a medium of exchange; it is also a store of value and a unit of account. Currency, the opposite of money, is debt. Since it can be created in unlimited amounts, it can't work as a store of value because its value depreciates as more units are created; for this same reason, it is not fair to denominate values in currency units since one currency unit today does not buy the same as a year ago because of inflation, the loss of purchasing power.

Summarize: While money, currency, and credit all serve as effective mediums of exchange, only money serves as a reliable store of value for saving. Currency and credit are not stores of value (not good to save), and there are not fair units of account (not good for price).

In simple terms, money is not currency, because currency is just credit and debt. We can conceptualize it as a ledger, a record of who owes what to whom. Currency is fake money since it’s the opposite of a store of value; it's always depreciating in value while its supply is inflated. This is the definition of inflation.

**Modern credit is not currency; it’s the opposite. It’s the promise to deliver currency in the future, the promise of a promise of money (in theory). But there’s no money behind. It’s an air loan.**

But how did we get here? Is everyone stupid? No, we have been tricked, manipulated, and dictated to use these currencies, and this banking system was forced on us. They stole our money and replaced it with fake substitutes to boost their profits.

## **MODERN MEDIUMS OF EXCHANGE = MONOPOLY MONEY**

**So nowadays we have fake money acting as cash/currency and fake currency acting as bank deposits or credit.** One is worse than the other, but both of them serve only as mediums of exchange. Those who store wealth with them will be robbed, and those who calculate business will be lied to.

Today we use currencies (government notes), coins, bank deposits (currency claims), checks (bank deposit claims), credit cards, and debit cards. All of them are ‘monopoly money’ fake claims based on a big and global fraud.

- *Government notes (government debt)*

Since governments are under the control of central banks, they can only create currency by borrowing. Governments must issue bonds, or debt, and the central bank can generate credit, or currency, to purchase these bonds.

The bond (government liability) is the counterpart of the ‘asset’ (the currency, a central bank asset). Bonds are debt, and currencies are credit.

When the central bank creates currency to lend it to the government at interest, it has literally the economic effect of **transferring the wealth of the nation to the banks for free**. The banks are not lending anything that they had to labor to produce; instead, they are creating it by printing paper notes or digital currency.

On the other side, governments have to collect money from citizens (producers, merchants, and workers) to pay the interest on the debt.

Despite their best efforts, governments are unable to repay the debt due to interest, which makes it bigger than the amount of currency. Let’s say the debt is 100 at 1% interest. So there’s only 100 in currency. But at the end of the year, there’s going to be a debt of 101. In order for the system to keep working, someone else has to go into debt to create more currency units, and governments have to keep borrowing and at least only paying the interest and rolling the debt.

The important thing is that if you have government currency debt free, you own it. This is the new ‘money.’. **Government currency is the ‘real’ cash, liquidity, or water.**

- *Bank deposits (bank debt)*

When you deposit your government currency in the bank, you are legally lending your currency to the bank, and the bank owes you the amount you deposit. This currency is not stored by banks until you request it. Banks use this currency as if it were theirs, and they do business with it. That’s why I said, **‘Your money in the bank’ is not yours; it’s not money; it’s not in the bank.** Its currency, its owe to you, is only registered on the bank ledger as a debt, not in a safe box.

The numbers you get in the bank account, or your balance, are government currency substitutes; they are bank deposits. Your currency deposit is the asset, and the number on your bank account balance is the liability.

But this is not the worst part. Banks lend around 10 times more currency than they have in deposits. So banks have more liabilities than assets (they are literally broke).

People often treat bank deposits, also known as government currency substitutes or bank tokens, as legal tender, allowing banks to create them arbitrarily and 'lend' them to unsuspecting clients who mistakenly believe they are receiving currency.

This is possible only because the bank's deposit has equal cash value.

***Government bonds, government currency, and bank deposits have equal value. But they are not the same.***

All of them have counterparty risk, but **cash, or government currency, is better** or safer than bonds or bank deposits. If interest rates rise, the value of bonds can decrease, and default on bank deposits can result in total loss, a scenario that has frequently occurred.

Keep in mind that bank deposits represent the bank's debts, also known as liabilities. Business activities and risk-taking make your currency unsecured, and they don't compensate you enough for the loan and risk.

- *Debit cards (bank deposit transfer)*

Your bank deposit is your right to get your currency back. When you use a credit card to buy something, you are transferring that right to the seller so he can redeem that bank token for currency if he wishes.

But you have to have had a deposit before you can spend it or transfer it.

- *Checks (bank deposit transfer)*

The same applies to checks. Your bank deposit is your right to get your currency back. When you use a check to buy something, you are transferring that right to the seller so he can redeem that bank token for currency if he wishes.

- *Credit card (bank deposit creator)*

Credit cards are different. When you use a credit card, you are creating a bank deposit backed by your promise of paying it back. By allowing the bank to create a currency substitute out of nothing and charge you high interest, you are essentially working for them for free.

Not only this, but you are also letting them collect fees from the payments processing that cost them nothing and support their fake money as a medium of exchange.

**Using credit cards is literally voting for financial slavery.** This is why companies make credit cards so convenient and offer benefits, with the intention of incentivizing and pushing people into the debt slavery system.

## **BANKS = MONEYCHANGERS**

‘Loans’ = exchanges

**The history of money is the history of moneychangers**, money dealers, or bankers. Money is an inanimate object. Bankers are alive; they are the ones in charge of making the money, currency, and credit flow or stop.

**They have been in existence for thousands of years**, from Egypt to Rome, where Jesus Christ himself threw them out of the temple and called them thieves, and he was not wrong.

Moneychangers played a crucial role in facilitating trade by exchanging different forms of currency and commodities. The profession of moneychangers evolved over time, particularly during the Roman Empire and the Middle Ages when various currencies were in circulation. In these times, moneychangers would set up shop at markets or public spaces to provide their services and **help merchants convert their money into a form that could be used for transactions with other traders.** As banking systems developed over time, the role of moneychangers expanded to include more complex financial services.

Today, moneychangers are still an essential part of the global economy, helping people exchange currencies and facilitating international trade.

**The Knights Templars** were a Christian military order established in 1119 who played a crucial role in the establishment of the financial system in medieval Europe. They established **a gold-backed credit system** that laid the foundation for the modern banking system. Their financial services included deposit accounts, loans, and even a form of early traveler's checks.

**The history of the goldsmiths** starts around 700 years ago in the year 1327. The company became responsible for hallmarking precious metals and played a significant role in regulating the quality and authenticity of gold and silver items. **In exchange for written acknowledgments or "receipts,"** they also provided gold deposit services.

Both groups played significant roles in the development of these early financial instruments, with goldsmiths issuing written acknowledgments for deposited gold and the Knights Templar establishing banking institutions that facilitated the use of such receipts as a form of payment.

This is a brief summary of the beginning of the moneychangers and how they discovered how to multiply money with paper receipts, better understood as counterfeiting. We now refer to it as fractional reserve banking, and let me tell you something: it's based on fraud.

Not only do they create bank deposits when you deposit currency, but they also create them when you "take a loan." Banks do not lend money, and they do not lend currency; they lend bank deposits (bank tokens/IOUs/currency substitutes/ paper receipts).

Banks had to redefine the word money to mean the opposite of money (debt) to trick the people. How can you lend the oposite of money and expect to be paid back plus interest? This took them thousands of years to achieve.

**The fact is that this is not a loan but an exchange.** When you take a loan, you sign a contract that creates a promissory note, which is your promise to pay. The bank then takes this promissory note, without your permission (steals), and sells it for cash (if you requiere it) or government bonds (to earn interest).

Your promissory note has equal value to cash and government bonds. And banks always need an asset to create a bank deposit (liability). So the banks literally steal your asset (promissory note) and sell them to create IOUs that they will ‘lend’ to you.

They ‘lend’ the oposite of money and call it a loan. The truth is that they are acting as moneychangers, and they are exchanging your IOU (promissory note) for a bank IOU (bank deposit) without your permission and pretending that you pay it back, but they never pay back theirs…

How is this possible? This is only possible because most people treat bank deposits (bank tokens, IOUs, and debts) as a medium of exchange because they trust the banks.

This is the root of inequality under the law. While one group can create IOUs from nothing and steal others, the other must work for them or exchange wealth.

If this bank defaults, its IOUs quickly vanish. This is a mathematical certainty; that’s why banks that are 'too big to fail' demand bailouts. **Every bank is bankrupt** since they have 7–10 times more liabilities than assets, and the assets they have are not theirs but their clients' assets. The only thing that keeps them alive is the trust of the public and the bailouts of the government.

**This is legalized slavery and theft.** There’s no other name. Banks own every industry, government, public figure, actor, etc. They have the power of God on earth, and it's time to stop them.

If we let the bank take our wealth for free, we will end up bankrupt, and they will end up owning everything. Every medium of exchange nowadays is an IOU or an IOU of an IOU. Ultimately, it is mathematically impossible to repay all of those IOUs, and banks pretend to keep all the assets.

*Check: IOU = deposit; IOU = cash; IOU = bond; IOU + interest*

The only way this system can continue is to keep creating new IOUs to pay the old ones, but even then (as it has been for over a century), the value of those IOUs keeps falling, causing hyperinflation.

If banks and governments want to ‘avoid’ (imposible) or relent to hyperinflation, they need to incur a great confiscation. So heads you lose, tails they win, playing this game doesn't make any fucking sense.

Buy Bitcoin, self custody, and fuck the government and the banking system.

Live free or die trying.

-

@ f3873798:24b3f2f3

2025-02-25 13:51:32

Estamos próximos a uma das principais premiações da indústria. Vemos não só a perversão de pautas woke e destruição de valores ocidentes, mas também um grande confronto entre o que mais forte o ativismo Lgbt ou o ativismo político entre as atrizes Fernanda Torres e Karla Gascon.

Só evidência o caos que é os conflitos de interesse de diversas vertentes que a esquerda abraça e diz que é sua.

Mas, o que mais impressiona é o fato do Oscar ter um filme no indicado que até o momento não ganhou nada, porém é notório a superioridade aos outros, este filme é Sing Sing.

Porque o filme Sing sing foi ignorado pelos avaliadores?

O filme tem uma narrativa de superação e como a arte pode mudar as pessoas e as realidades mais pertubadoras. Ele retrata o Sistema carcerário americano, onde realidade de vários presos é mudada atraves de um projeto de um teatro na prisão.

Observando friamente a sintese do filme é uma história que se encaixa perfeitamente aos vies de bandidolatria, se não tivesse um questão, a ação transformadora da arte e deixando de serem vítimas e serem artistas.

Porém apesar de ser uma obra de arte que estimula as pessoas pensarem sobre a vida e ter uma pegada inovadora e completamente diferente dos demais filmes que retratam o sistema carcerário, ele é totalmente ignorado por não ser suficientemente lacrativo.

-

@ 9171b08a:8395fd65

2025-02-25 13:27:26

For the price tag on this room, I would've thought my death bed would be more comfortable. Since I've been admitted I've been in a perpetual state of discomfort despite the medicine that is supposed to keep me numb. The room is dark and I'm alone with the sounds of industry that keep this planet churning through the expanse of space.

The unease goes deeper than the surface, beyond the 1000 thread count Earth cotton grating against my skin, deeper than the cracking sinews of my muscles, it lurks in the wake of the vibrations of my heart as it throbs its final throbs.

The holoscreen comes to life at a thoughts command and quickly my unease turns to irritation as my name crawls across the screen. A woman points to the very hospital where I lay and expresses her sorrow as "One of the greatest men of this era awaits his death."

I suppose it couldn't come quicker. I shut off the holoscreen. Plunge myself back into the darkness and simply watch the shadows of the freighter transports cast through the opaque vinyl shutter as they pass by.

The light comes on. It blinds me and all I can hear are the footsteps that approach. The heels clatter loudly, soles of well made shoes. Expensive, probably Earth made like my sheets.

"You don't have to go through with this old man." I know the voice well. My mentee, the man I've groomed to take over my empire speaks again, "It's not too late to take the regenerons. You'd be looking younger than me within the week."

I don't care to explain myself. I turn away from him and he mutters something else then reaches over and rests a vase on the table in front of me.

Inside the vase float two scarlet tulips within a bouquet of gypsophila. The flowers smell freshly cut, a scent that instantly freshens my soul and harkens to a time before anyone could imagine I'd be known as "one of the greatest men of the era."

My mentee speaks, but his voice is nothing more than the ruffling of my sheets as I sit up and draw closer to you.

Precious tulips.

Tulips like these, I picked in the endless fields of Verduia. I, like the others who'd been bred to work on that planet, toiled away endless days to pick flowers just like these for affluent people just like me at this very moment.

I was never supposed to have the life I've lived. My biology was built to pick and die. To work, stay poor, and keep my head buried in the fields, that was my purpose.

I worked hard. My hands pruned and nurtured roots in the dark soil. But I loved harder. The memory of your marble skin against the thick layer of dirt beneath my nails will never fade. I've amassed a wealth that is the envy of entire solar systems, but the memory of you is richer.

My tulip, my eternal blossom. I'd run away from the task masters with you and hide in the tall sunflower fields where we'd make love.

People like us weren't meant to be in love. When you passed, I felt no greater discomfort. I thought wealth could fill that void. It hasn't. Not even a millennia since could wash away the memory of you. Only the closure of time, the death of me can remove this ever long dread. Here the need to revive the feeling only you could inspire ends.

-Art By Surenja Rajawat- Find him on instagram @suren.rajawat

-

@ 57d1a264:69f1fee1

2025-02-25 13:24:49

Galoy released a new product called Lana, a platform for bitcoin loans. The team will provide an introduction and then we'll dive into the design.

To get you up to speed, check out the website, slide deck and podcast interview:

- https://www.galoy.io/lana-bitcoin-loans-platform

- https://docs.google.com/presentation/d/1IQocefpCN5_wKX91EWtLa19IpMS_Ye8goNLAgGQbfdU/edit#slide=id.g31d536107ae_0_0

- https://stephanlivera.com/episode/634/

If you get a chance, please take a peek before the call. That makes the design reviews more useful because we need to spend less time going over the basics.

On `Thu Feb 27th · 15:00 – 16:00 CET`

Join from https://meet.jit.si/bitcoindesign

Check your timezone https://everytimezone.com/s/998e22fc

Track https://github.com/BitcoinDesign/Meta/issues/758

originally posted at https://stacker.news/items/896570

-

@ e5de992e:4a95ef85

2025-02-25 12:46:53

The future of decentralized identity promises a digital landscape where users have full control over their personal data, privacy, and interactions. When users own their digital presence, several transformative changes could reshape the internet:

---

## Empowerment and Control

### Self-Sovereignty

Users will manage their identities through cryptographic keys rather than relying on third-party platforms. This means you decide what data to share, how to share it, and with whom, eliminating reliance on centralized authorities.

### Data Portability

Decentralized identity frameworks enable seamless movement of personal data across various services. Without vendor lock-in, you can maintain a consistent digital persona, regardless of the platform or application you choose to use.

---

## Privacy and Security

### Enhanced Privacy

With decentralized identity, you control the amount and type of information you reveal. This minimizes exposure to data breaches, unauthorized surveillance, and privacy violations that are common in centralized systems.

### Stronger Security

Cryptography plays a central role in decentralized identity, reducing the risk of identity theft and fraud. Since your identity is not stored in a single, vulnerable location, it's much harder for attackers to compromise your personal information.

---

## Interoperability and Innovation

### Interoperable Ecosystems

Decentralized identity standards can pave the way for interoperable systems where different services and platforms recognize and trust your digital credentials. This can lead to smoother user experiences and increased innovation in digital services.

### New Economic Models

Ownership of your digital identity might also enable new ways to monetize personal data. Instead of platforms harvesting data for profit, users could potentially control and even earn from the use of their own information.

---

## Social and Cultural Impact

### Democratizing the Digital Space

A user-owned digital identity reduces the power imbalance between large tech corporations and individuals. It fosters a more democratic online environment where freedom of expression and personal autonomy are respected.

### Resilience Against Censorship

Decentralized systems distribute data across multiple nodes, making it far more resistant to censorship. This ensures that your voice can be heard even in environments where centralized platforms might suppress it.

---

## Challenges Ahead

### Usability and Adoption

While the potential benefits are significant, mainstream adoption will require overcoming technical and usability challenges. Managing cryptographic keys, for instance, may be daunting for non-technical users unless user-friendly solutions are developed.

### Regulatory and Standardization Issues

As decentralized identity becomes more prevalent, there will be a need for clear standards and regulations to ensure interoperability, security, and consumer protection without stifling innovation.

---

## In Summary

When users own their digital presence, the future of decentralized identity is marked by increased privacy, enhanced control, and a more open, interoperable digital ecosystem. This shift not only empowers individuals but also encourages the development of innovative technologies and business models that prioritize user rights and freedoms in the online world.

-

@ 57d1a264:69f1fee1

2025-02-25 12:38:46

I've been pondering how LSPs (lightning service providers) might pan out over time and how that might affect fees, and I am wondering what everyone else is thinking. Some people will always prefer to manage their own channels, and for some specific use cases, that might be preferable. But I am thinking about the broad userbase that does not want to do that. We will need a massive LSP infrastructure to onboard people and to enable insane amounts of payments.

LSPs will need to efficiently open and adjust channels for users, using their own liquidity or sourcing liquidity from other providers, using just-in-time channels, batching and/or splicing to reduce costs and wait times. Across all this, along with facilitating payments, they need to make their business model work and offer different options for users to pay for their services.

Users might be able to:

1. Pay-as-you-go (pay X for Y more liquidity for Z amount of time)

2. Pay X per month for Y inbound liquidity

3. Pay X per month for unlimited liquidity

4. Nothing for liquidity, but higher transaction fees

A wallet might also automatically choose an appropriate LSP based on what is the best and most appropriate deal at the time.

Let's look at user scenarios:

- If someone sends and receives the same amount every month, they will never need more liquidity. They just draw down the same channel and fill it up again. So they would only pay the LSP for them assigning that fixed amount of liquidity to them. Maybe options 1 and 2 are good for them.

- If someone receives more than they send (they save a certain amount every month), they will need more and more inbound liquidity over time. They might choose option 2.

- An online store that receives a ton and can't really estimate how much, might go for option 3.

- For option 4, it depends if the higher transaction fees are fixed or percentage-based.

It's a bit like choosing a data plan for your phone (or for internet at home). You can get a prepaid card, a regular plan with certain limits, or go unlimited. And there are separate plans for small and large businesses, etc. And there are massive amounts of complex infrastructure behind these service providers to make it all work.

So when someone starts using a lightning wallet, maybe they have to first pick an LSP and a plan before being able to receive. Or maybe they get a first channel for free and pay higher fees, and are then prompted to choose a plan. Maybe they need to wait an hour until the LSP has enough channel opens for a batch/splice, to reduce costs. A complex market at work.

Is that how things might pan out? Am I completely off? Is it worth mocking up different scenarios?

```

#bitcoin #LN #BTC #Lightning #LSP #service #zaps #sats #wallet

```

originally posted at https://stacker.news/items/896520

-

@ 2063cd79:57bd1320

2025-02-25 10:44:02

Ich stimme mit Anonymous überein, dass es Probleme mit der tatsächlichen Verwendung von digitalem Bargeld auf kurze Sicht gibt. Aber es hängt in gewissem Maße davon ab, welches Problem man zu lösen versucht.

Eine Sorge, die ich habe, ist, dass der Übergang zum elektronischen Zahlungsverkehr die Privatsphäre einschränken wird, da es einfacher wird, Transaktionen zu protokollieren und aufzuzeichnen. Es könnten Profile angelegt werden, in denen das Ausgabeverhalten eines jeden von uns verfolgt wird.

Schon jetzt wird, wenn ich etwas telefonisch oder elektronisch mit meiner Visa-Karte bestelle, genau aufgezeichnet, wie viel ich ausgegeben habe und wo ich es ausgegeben habe. Im Laufe der Zeit könnten immer mehr Transaktionen auf diese Weise abgewickelt werden, und das Ergebnis könnte einen großen Verlust an Privatsphäre bedeuten.

Die Bezahlung mit Bargeld ist zwar immer noch per Post möglich, aber dies ist unsicher und umständlich. Ich denke, dass die Bequemlichkeit von Kredit- und Debitkarten die Bedenken der meisten Menschen in Bezug auf Privatsphäre ausräumen wird und dass wir uns in einer Situation befinden werden, in der große Mengen an Informationen über das Privatleben aller Leute existieren.

Hier könnte ich mir vorstellen, dass digitales Bargeld eine Rolle spielen könnte. Stellt euch ein Visa-ähnliches System vor, bei dem ich für die Bank nicht anonym bin. Stellt euch in diesem Modell vor, dass mir die Bank einen Kredit gewährt, ganz so wie bei einer Kreditkarte. Allerdings, anstatt mir nur eine Kontonummer zu geben, die ich am Telefon ablese oder in einer E-Mail verschicke, gibt sie mir das Recht, bei Bedarf digitales Bargeld zu verlangen.

Ich habe immer etwas digitales Bargeld beiseite, dass ich für Transaktionen ausgeben kann, wie bereits in früheren Beiträgen beschrieben. Wenn das Geld knapp wird, schicke ich eine E-Mail an die Bank und erhalte mehr digitales Bargeld (dcash). Jeden Monat sende ich einen Check an die Bank, um mein Konto auszugleichen, genauso wie ich es mit meinen Kreditkarten mache. Meine Beziehung zur Bank sind meinen derzeitigen Beziehungen zu den Kreditkartenunternehmen sehr ähnlich: häufige Überweisungen und eine einmalige Rückzahlung jeden Monat per Check.

Das hat mehrere Vorteile gegenüber dem System, auf das wir zusteuern. Es werden keine Aufzeichnungen darüber geführt, wofür ich mein Geld ausgebe. Die Bank weiß nur, wie viel ich jeden Monat abgehoben habe; es könnte sein, dass ich es zu diesem Zeitpunkt ausgegeben habe oder auch nicht. Bei einigen Transaktionen (z.B. Software) könnte ich für den Verkäufer anonym sein; bei anderen könnte der Verkäufer meine wirkliche Adresse kennen, aber dennoch ist keine zentrale Stelle in der Lage, alles zu verfolgen, was ich kaufe.

(Es gibt auch einen Sicherheitsvorteil gegenüber dem lächerlichen aktuellen System, bei dem die Kenntnis über eine 16-stellige Nummer und eines Ablaufdatums es jedem ermöglicht, etwas auf meinen Namen zu bestellen!)

Außerdem sehe ich nicht ein, warum dieses System nicht genauso legal sein sollte wie die derzeitigen Kreditkarten. Der einzige wirkliche Unterschied besteht darin, dass nicht nachverfolgt werden kann, wo die Nutzer ihr Geld ausgeben, und soweit ich weiß, war diese Möglichkeit nie ein wichtiger rechtlicher Aspekt von Kreditkarten. Sicherlich wird heute niemand zugeben, dass die Regierung ein Interesse daran hat, ein Umfeld zu schaffen, in dem jede finanzielle Transaktion nachverfolgt werden kann.

Zugegeben, dies bietet keine vollständige Anonymität. Es ist immer noch möglich, ungefähr zu sehen, wie viel jede Person ausgibt (obwohl nichts eine Person daran hindert, viel mehr Bargeld abzuheben, als sie in einem bestimmten Monat ausgibt, außer vielleicht für Zinsausgaben; aber vielleicht kann sie das zusätzliche digitale Bargel (digicash) selbst verleihen und dafür Zinsen erhalten, um das auszugleichen). Und es orientiert sich an demselben Kunden/ Verkäufer-Modell, das Anonymous kritisierte. Ich behaupte aber, dass dieses Modell heute und in naher Zukunft die Mehrheit der elektronischen Transaktionen ausmachen wird.

Es ist erwähnenswert, dass es nicht trivial ist, ein Anbieter zu werden, der Kreditkarten akzeptiert. Ich habe das mit einem Unternehmen, das ich vor ein paar Jahren betrieben habe, durchgemacht. Wir verkauften Software über den Versandhandel, was die Kreditkartenunternehmen sehr nervös machte. Es gibt zahlreiche Telefonbetrügereien, bei denen Kreditkartennummern über einige Monate hinweg gesammelt werden und dann große Beträge von diesen Karten abgebucht werden. Bis der Kunde seine monatliche Abrechnung erhält und sich beschwert, ist der Verkäufer bereits verschwunden. Um unser Kreditkartenterminal zu bekommen, wandten wir uns an ein Unternehmen, das Start-ups dabei „hilft“. Sie schienen selbst ein ziemlich zwielichtiges Unternehmen zu sein. Wir mussten unseren Antrag dahingehend fälschen, dass wir etwa 50% der Geräte auf Messen verkaufen würden, was offenbar als Verkauf über den Ladentisch zählte. Und wir mussten etwa 3.000 Dollar im Voraus zahlen, als Bestechung, wie es schien. Selbst dann hätten wir es wahrscheinlich nicht geschafft, wenn wir nicht ein Büro im Geschäftsviertel gehabt hätten.

Im Rahmen des digitalen Bargeldsystems könnte dies ein geringeres Problem darstellen. Das Hauptproblem bei digitalem Bargeld sind doppelte Ausgaben, und wenn man bereit ist, eine Online-Überprüfung vorzunehmen (sinnvoll für jedes Unternehmen, das mehr als ein paar Stunden für die Lieferung der Ware benötigt), kann dies vollständig verhindert werden. Es gibt also keine Möglichkeit mehr, dass Händler Kreditkartennummern für spätere Betrügereien sammeln. (Allerdings gibt es immer noch Probleme mit der Nichtlieferung von Waren, so dass nicht alle Risiken beseitigt sind). Dadurch könnte das System schließlich eine größere Verbreitung finden als die derzeitigen Kreditkarten.

Ich weiß nicht, ob dieses System zur Unterstützung von illegalen Aktivitäten, Steuerhinterziehung, Glücksspiel oder Ähnlichem verwendet werden könnte. Das ist nicht der Zweck dieses Vorschlags. Er bietet die Aussicht auf eine Verbesserung der Privatsphäre und der Sicherheit in einem Rahmen, der sogar rechtmäßig sein könnte, und das ist nicht verkehrt.

-----

Englischer Artikel erschienen im Nakamoto Institute: [Digital Cash & Privacy](https://nakamotoinstitute.org/library/digital-cash-and-privacy/here)

-

@ 6a6be47b:3e74e3e1

2025-02-25 10:24:55

Hi frens,

While drawing this fly 🪰, I started thinking about how to make my art stand out. Maybe I should focus on making it more appealing—or at least improving its presentation. Don’t get me wrong, I’m not against making my work more consumable, but the marketing side of things takes so much time away from actually creating art. It’s sad that sometimes it feels less about delivering high-quality work and more about turning it into “content.”

Honestly, that can be exhausting. Like Fall Out Boy said, “all this effort to make it look effortless.”It’s not really my style to turn my art—or the process of creating it—into content. That’s why I sometimes struggle with crafting or presenting it in a way that fits today’s trends.

Sometimes, the pressure to make my art presentable is so overwhelming that it makes me feel like not creating at all. And when it doesn’t yield the kind of recognition or financial support I hope for after all that effort, it can be really disappointing. It’s like watching all that hard work slowly erode my soul. It’s tough to keep going when it feels like my art isn’t being valued in the way I wish it could be.

I want to be clear: this isn’t me dissing anyone. You do you, and I’ll do me. As Crowley would say, “Do what thou wilt.” What I’m really trying to figure out is how to find that sweet spot—where I can keep up with the times and make my art more appealing without losing my soul in the process.

I’m trying my best, and I know I’ll make mistakes along the way, but I’ll keep going. I just wanted to share these thoughts with you because I’m usually pretty upbeat here—maybe even a little superficial at times—but this is me being _more_ real with you.

Art is such a huge part of my life, and through my work, I’m already sharing something raw and personal with you. But now you also know why my presentation might sometimes feel simple or plain. I’m working on finding that balance, and I’ll get there eventually.

Godspeed, my frens

-

@ d360efec:14907b5f

2025-02-25 10:16:18

**ภาพรวม BTCUSDT (OKX):**

Bitcoin (BTCUSDT) แนวโน้มระยะยาว TF Day ยังคงเป็นขาลง แนวโน้มระยะกลาง TF 4H Sideway down และแนวโน้มระยะสั้น TF 15M Sideways Down

**วิเคราะห์ทีละ Timeframe:**

**(1) TF Day (รายวัน):**

* **แนวโน้ม:** ขาลง (Downtrend)

* **SMC:**

* Lower Highs (LH) และ Lower Lows (LL)

* Break of Structure (BOS) ด้านล่าง

* **Liquidity:**

* มี Sellside Liquidity (SSL) อยู่ใต้ Lows ก่อนหน้า

* มี Buyside Liquidity (BSL) อยู่เหนือ Highs ก่อนหน้า

* **ICT:**

* **Order Block** ราคาไม่สามารถผ่าน Order Block ได้

* **EMA:**

* ราคาอยู่ใต้ EMA 50 และ EMA 200

* **Money Flow (LuxAlgo):**

* สีแดง

* **Trend Strength (AlgoAlpha):**

* สีแดง แสดงถึงแนวโน้มขาลง

* **Chart Patterns:** *ไม่มีรูปแบบที่ชัดเจน*

* **Volume Profile:**

* Volume ค่อนข้างนิ่ง

* **แท่งเทียน:** แท่งเทียนล่าสุดเป็นสีแดง

* **แนวรับ:** บริเวณ Low ล่าสุด

* **แนวต้าน:** EMA 50, EMA 200 , Order Block

* **สรุป:** แนวโน้มขาลง

**(2) TF4H (4 ชั่วโมง):**

* **แนวโน้ม:** ขาลง (Downtrend)

* **SMC:**

* Lower Highs (LH) และ Lower Lows (LL)

* Break of Structure (BOS) ด้านล่าง

* **Liquidity:**

* มี SSL อยู่ใต้ Lows ก่อนหน้า

* มี BSL อยู่เหนือ Highs ก่อนหน้า

* **ICT:**

* **Order Block** ราคาไม่สามารถผ่าน Order Block ได้

* **EMA:**

* ราคาอยู่ใต้ EMA 50 และ EMA 200

* **Money Flow (LuxAlgo):**

* สีแดง แสดงถึงแรงขาย

* **Trend Strength (AlgoAlpha):**

* สีแดง แสดงถึงแนวโน้มขาลง

* **Chart Patterns:** *ไม่มีรูปแบบที่ชัดเจน*

* **Volume Profile:**

* Volume ค่อนข้างนิ่ง

* **แนวรับ:** บริเวณ Low ล่าสุด

* **แนวต้าน:** EMA 50, EMA 200, Order Block

* **สรุป:** แนวโน้มขาลง,

**(3) TF15 (15 นาที):**

* **แนวโน้ม:** Sideway Down

* **SMC:**

* Lower High (LH) และ Lower Lows (LL)

* Break of Structure (BOS) ด้านล่าง

* **ICT:**

* **Order Block:** ราคา Sideways ใกล้ Order Block

* **EMA:**

* EMA 50 และ EMA 200 เป็นแนวต้าน

* **Money Flow (LuxAlgo):**

* แดง

* **Trend Strength (AlgoAlpha):**

* แดง/ ไม่มีสัญญาณ

* **Chart Patterns:** *ไม่มีรูปแบบที่ชัดเจน*

* **Volume Profile:** Volume ค่อนข้างสูง

* **แนวรับ:** บริเวณ Low ล่าสุด

* **แนวต้าน:** EMA 50, EMA 200, Order Block

* **สรุป:** แนวโน้ม Sideways Down,

**สรุปภาพรวมและกลยุทธ์ (BTCUSDT):**

* **แนวโน้มหลัก (Day):** ขาลง

* **แนวโน้มรอง (4H):** ขาลง

* **แนวโน้มระยะสั้น (15m):** Sideways Down

* **Liquidity:** มี SSL ทั้งใน Day, 4H, และ 15m

* **Money Flow:** เป็นลบในทุก Timeframes

* **Trend Strength:** Day/4H/15m เป็นขาลง

* **Chart Patterns:** ไม่พบรูปแบบที่ชัดเจน

* **กลยุทธ์:**

1. **Wait & See (ดีที่สุด):** รอความชัดเจน

2. **Short (เสี่ยง):** ถ้าไม่สามารถ Breakout EMA/แนวต้านใน TF ใดๆ ได้ หรือเมื่อเกิดสัญญาณ Bearish Continuation

3. **ไม่แนะนำให้ Buy:** จนกว่าจะมีสัญญาณกลับตัวที่ชัดเจนมากๆ

**Day Trade & การเทรดรายวัน:**

* **Day Trade (TF15):**

* **Short Bias:** หาจังหวะ Short เมื่อราคาเด้งขึ้นไปทดสอบแนวต้าน (EMA, Order Block)

* **Stop Loss:** เหนือแนวต้านที่เข้า Short

* **Take Profit:** แนวรับถัดไป (Low ล่าสุด)

* **ไม่แนะนำให้ Long**

* **Swing Trade (TF4H):**

* **Short Bias:** รอจังหวะ Short เมื่อราคาไม่สามารถผ่านแนวต้าน EMA หรือ Order Block ได้

* **Stop Loss:** เหนือแนวต้านที่เข้า Short

* **Take Profit:** แนวรับถัดไป

* **ไม่แนะนำให้ Long**

**สิ่งที่ต้องระวัง:**

* **Sellside Liquidity (SSL):** มีโอกาสสูงที่ราคาจะถูกลากลงไปแตะ SSL

* **False Breakouts:** ระวัง

* **Volatility:** สูง

**Setup Day Trade แบบ SMC (ตัวอย่าง):**

1. **ระบุ Order Block:** หา Order Block ขาลง (Bearish Order Block) ใน TF15

2. **รอ Pullback:** รอให้ราคา Pullback ขึ้นไปทดสอบ Order Block นั้น

3. **หา Bearish Entry:**

* **Rejection:** รอ Price Action ปฏิเสธ Order Block

* **Break of Structure:** รอให้ราคา Break โครงสร้างย่อยๆ

* **Money Flow:** ดู Money Flow ให้เป็นสีแดง

4. **ตั้ง Stop Loss:** เหนือ Order Block

5. **ตั้ง Take Profit:** แนวรับถัดไป

**คำแนะนำ:**

* **ความขัดแย้งของ Timeframes:** ไม่มีแล้ว ทุก Timeframes สอดคล้องกัน

* **Money Flow:** เป็นลบในทุก Timeframes

* **Trend Strength:** เป็นลบ

* **Order Block TF Day:** หลุด Order Block ขาขึ้นแล้ว

* **ถ้าไม่แน่ใจ อย่าเพิ่งเข้าเทรด**

**Disclaimer:** การวิเคราะห์นี้เป็นเพียงความคิดเห็นส่วนตัว ไม่ถือเป็นคำแนะนำในการลงทุน ผู้ลงทุนควรศึกษาข้อมูลเพิ่มเติมและตัดสินใจด้วยความรอบคอบ

-

@ d360efec:14907b5f

2025-02-25 09:12:44

$OKX:BTCUSDT.P

**Overall Assessment:**

Bitcoin (BTCUSDT) on OKX is currently showing a bearish trend across all analyzed timeframes (Daily, 4-Hour, and 15-Minute). While the long-term trend (Daily) was technically an uptrend, it has *significantly weakened* and broken key support levels, including a major bullish Order Block and the 50-period EMA. The 4-hour and 15-minute charts confirm the downtrend. This analysis focuses on identifying potential areas of Smart Money activity (liquidity pools and order blocks), assessing trend strength, and looking for any emerging chart patterns.

**Detailed Analysis by Timeframe:**

**(1) TF Day (Daily):**

* **Trend:** Downtrend

* **SMC (Smart Money Concepts):**

* The Higher Highs (HH) and Higher Lows (HL) structure is *broken*.

* Prior Breaks of Structure (BOS) to the upside, but now a significant and deep pullback/reversal is underway.

* **Liquidity:**

* **Sellside Liquidity (SSL):** Significant SSL rests below previous lows in the 85,000 - 90,000 range.

* **Buyside Liquidity (BSL):** BSL is present above the all-time high.

* **ICT (Inner Circle Trader Concepts):**

* **Order Block:** The price has *broken below* the prior bullish Order Block. This is a *major bearish signal*.

* **FVG:** No significant Fair Value Gap is apparent at the current price level.

* **EMA (Exponential Moving Average):**

* Price is *below* the 50-period EMA (yellow).

* The 200-period EMA (white) is the next major support level.

* **Money Flow (LuxAlgo):**

* A *long red bar* indicates strong and sustained selling pressure.

* **Trend Strength (AlgoAlpha):**

* Red cloud, indicating a downtrend. No buy/sell signals are present.

* **Chart Patterns:** No readily identifiable chart patterns are dominant.

* **Volume Profile:** Relatively low volume.

* **Candlesticks:** Recent candlesticks are red, confirming selling pressure.

* **Support:** EMA 200, 85,000-90,000 (SSL area).

* **Resistance:** EMA 50, Previous All-Time High.

* **Summary:** The Daily chart has shifted to a downtrend. The break below the Order Block and 50 EMA, combined with negative Money Flow and Trend Strength, are all strong bearish signals.

**(2) TF4H (4-Hour):**

* **Trend:** Downtrend.

* **SMC:**

* Lower Highs (LH) and Lower Lows (LL).

* BOS to the downside.

* **Liquidity:**

* **SSL:** Below previous lows.

* **BSL:** Above previous highs.

* **ICT:**

* **Order Block:** The price was rejected by a bearish Order Block.

* **EMA:**

* Price is below both the 50-period and 200-period EMAs (bearish).

* **Money Flow (LuxAlgo):**

* Predominantly red, confirming selling pressure.

* **Trend Strength (AlgoAlpha):**

* Red cloud, confirming downtrend.

* **Chart Patterns:** No readily identifiable chart patterns.

* **Volume Profile:** Relatively steady volume.

* **Support:** Recent lows.

* **Resistance:** EMA 50, EMA 200, Order Block.

* **Summary:** The 4-hour chart is in a confirmed downtrend. Money Flow and Trend Strength are bearish.

**(3) TF15 (15-Minute):**

* **Trend:** Downtrend / Sideways Down

* **SMC:**

* Lower Highs (LH) and Lower Lows (LL).

* BOS to the downside.

* **ICT:**

* **Order Block** price is near to a bearish Order Block.

* **EMA:**

* The 50-period and 200-period EMAs are acting as resistance.

* **Money Flow (LuxAlgo):**

* Red

* **Trend Strength (AlgoAlpha):**

* Red/No signals

* **Chart Patterns:** None

* **Volume Profile:**

* Relatively High Volume

* **Support:** Recent lows.

* **Resistance:** EMA 50, EMA 200, Order Block.

* **Summary:** The 15-minute chart is clearly bearish, with price action, EMAs, and Money Flow all confirming the downtrend.

**Overall Strategy and Recommendations (BTCUSDT):**

* **Primary Trend (Day):** Downtrend

* **Secondary Trend (4H):** Downtrend.

* **Short-Term Trend (15m):** Downtrend/ Sideways Down.

* **Liquidity:** Significant SSL zones exist below the current price on all timeframes.

* **Money Flow:** Negative on all timeframes.

* **Trend Strength:** Bearish on Day,4H and 15m.

* **Chart Patterns:** None identified.

* **Strategies:**

1. **Wait & See (Best Option):** The strong bearish momentum on all shorter timeframes.

2. **Short (High Risk):** This aligns with the 4H and 15m downtrends.

* **Entry:** On rallies towards resistance levels (EMAs on 15m/4H, previous support levels that have turned into resistance, Order Blocks).

* **Stop Loss:** Above recent highs on the chosen timeframe, or above a key resistance level.

* **Target:** The next support levels (recent lows on 15m, then potentially the SSL zones on the 4H and Daily charts).

3. **Buy (Extremely High Risk - NOT Recommended):** Do *not* attempt to buy until there are *very strong and consistent* bullish reversal signals across *all* timeframes.

**Key Recommendations:**

* **Conflicting Timeframes:** The conflict is resolved toward the downside. The Daily is weakening significantly.

* **Money Flow:** Consistently negative across all timeframes, a major bearish factor.

* **Trend Strength:** Bearish on Day,4h and 15m.

* **Daily Order Block:** The *break* of the bullish Order Block on the Daily chart is a significant bearish development.

* **Sellside Liquidity (SSL):** Be aware that Smart Money may target the SSL zones below. This increases the risk of stop-loss hunting.

* **Risk Management:** Due to the high uncertainty and volatility, *strict risk management is absolutely critical.* Use tight stop-losses, do not overtrade, and be prepared for rapid price swings.

* **Volume:** Confirm any breakout or breakdown with volume.

**Day Trading and Intraday Trading Strategies:**

* **Day Trade (TF15 focus):**

* **Short Bias:** Given the current 15m downtrend and negative Money Flow, the higher probability is to look for shorting opportunities.

* **Entry:** Look for price to rally to resistance levels (EMAs, Order Blocks, previous support levels that have become resistance) and then show signs of rejection (bearish candlestick patterns, increasing volume on the downside).

* **Stop Loss:** Place a stop-loss order above the resistance level where you enter the short position.

* **Take Profit:** Target the next support level (recent lows).

* **Avoid Long positions** until there's a *clear* and *confirmed* bullish reversal on the 15m chart (break above EMAs, positive Money Flow, bullish market structure).

* **Swing Trade (TF4H focus):**

* **Short Bias:** The 4H chart is in a downtrend.

* **Entry:** Wait for price to rally to resistance levels (EMAs, Order Blocks) and show signs of rejection.

* **Stop Loss:** Above the resistance level where you enter the short position.

* **Take Profit:** Target the next support levels (e.g., the 200 EMA on the Daily chart, SSL zones).

* **Avoid Long positions** until there's a *clear* and *confirmed* bullish reversal on the 4H chart.

**SMC Day Trade Setup Example (TF15 - Bearish):**

1. **Identify Bearish Order Block:** Locate a bearish Order Block on the TF15 chart (a bullish candle before a strong downward move).

2. **Wait for Pullback:** Wait for the price to pull back up to test the Order Block (this may or may not happen).

3. **Bearish Entry:**

* **Rejection:** Look for price action to reject the Order Block (e.g., a pin bar, engulfing pattern, or other bearish candlestick pattern).

* **Break of Structure:** Look for a break of a minor support level on a *lower* timeframe (e.g., 1-minute or 5-minute) after the price tests the Order Block. This confirms weakening bullish momentum.

* **Money Flow:** Confirm that Money Flow remains negative (red).

4. **Stop Loss:** Place a stop-loss order *above* the Order Block.

5. **Take Profit:** Target the next support level (e.g., recent lows) or a bullish Order Block on a higher timeframe.

**In conclusion, BTCUSDT is currently in a high-risk, bearish environment. The "Wait & See" approach is strongly recommended for most traders. Shorting is the higher-probability trade *at this moment*, but only for experienced traders who can manage risk extremely effectively. Buying is not recommended at this time.**

**Disclaimer:** This analysis is for informational purposes only and represents a personal opinion. It is not financial advice. Investing in cryptocurrencies involves significant risk. Investors should conduct their own research and exercise due diligence before making any investment decisions.

-

@ 57d1a264:69f1fee1

2025-02-25 07:28:18

@Voltage team will be building a simple implementation of a Lightning gated API service using a Voltage LND Node and the L402 protocol.

📅 Thursday, February 27th 4:00 PM CDT

📷 Live on Voltage Discord, on X, or on YouTube.

- discord.gg/EN93fDfQ

- https://x.com/voltage_cloud/status/1892938201980919985

- https://www.youtube.com/@voltage_cloud

originally posted at https://stacker.news/items/896373

-

@ ef1744f8:96fbc3fe

2025-02-25 05:51:23

kZPO/Pgqm/nOfGtpHNVK3gcDhzs5sSvyVqUZlAJrs95os0xUFhO4VlBC5GuEYF0uYTTGVGe60TjK8sm+ixOIPxpd3eYGGtZs9CjkRzis8vU=?iv=KyDTZEV4fCT/lKJWR4heeQ==

-

@ ef1744f8:96fbc3fe

2025-02-25 05:45:21

B3rafJgfWeHKOv/c2y8pk7thAOvmYYooCN1BMJh+gtmngdanQ7Mnimz048gzTWlV8Ap6wHRtu2rD6W6KDt6r82HlaftHm8jRBH1BGJ8Aw+GYy/PRGuQnUZP3DcjZusRchZSIhWuFBnhonWUHrxwnzrmcolx6yPekWKzxn9DR8Kt2qWIxbg2791EnuQn6orrAdw8MJJQg/hZhEdqib8KuweUrn6YDPi8ICV099rHUAlWBR6NSn/kwyomarCmV6U0bucUiv5y6QrBUSIQGfMTKYGBgmdXdeWTQ4YSYTaF0cZNDCJorksVIxx32dpc8RhYsvooZwk0OAAGg5LO5dekA1rn5jZk6rbmAnRcvnQFcue0=?iv=gZIUGRNTRQULCjSeRae+YQ==