-

@ 2e8970de:63345c7a

2025-02-25 17:16:37

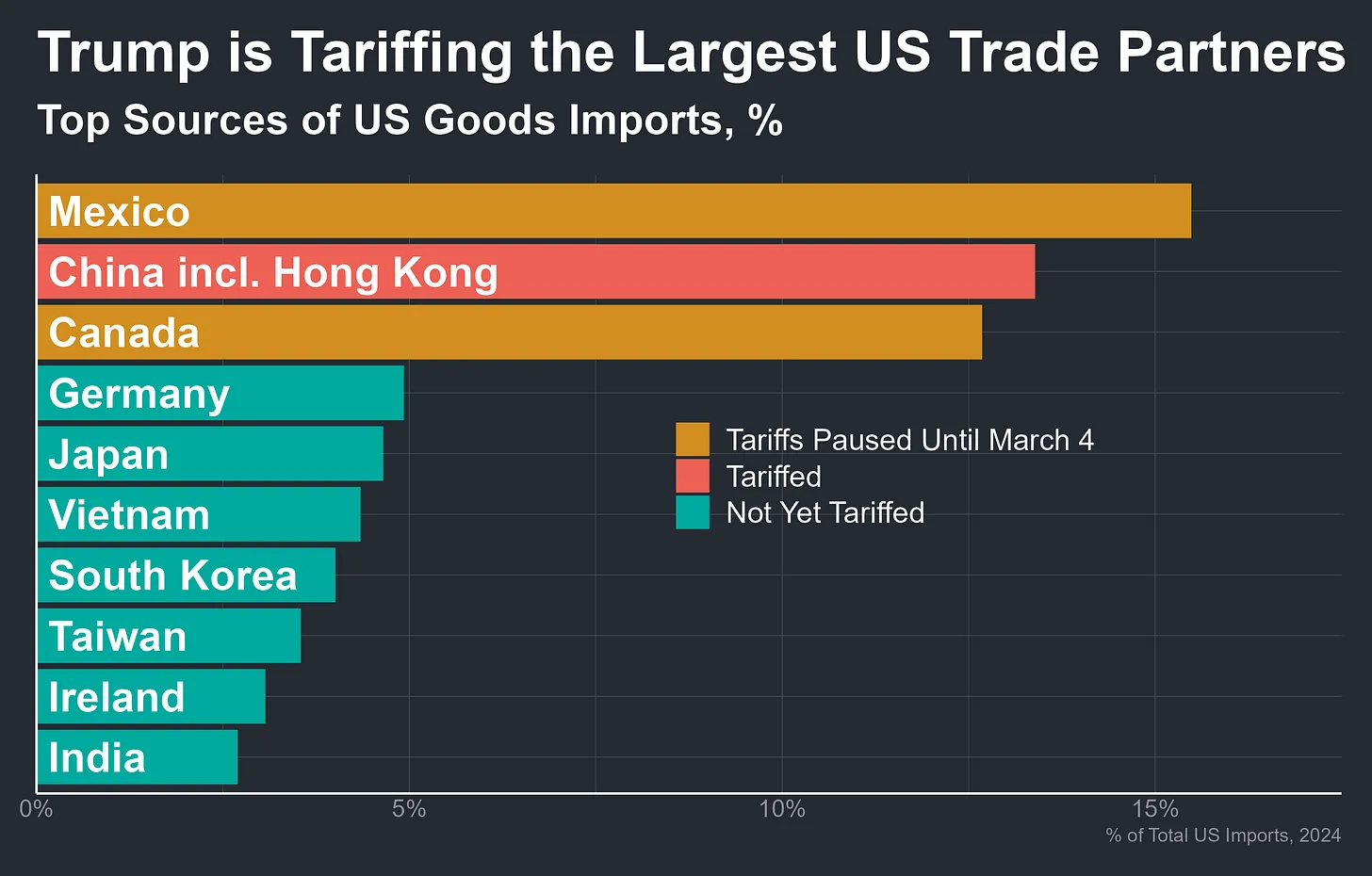

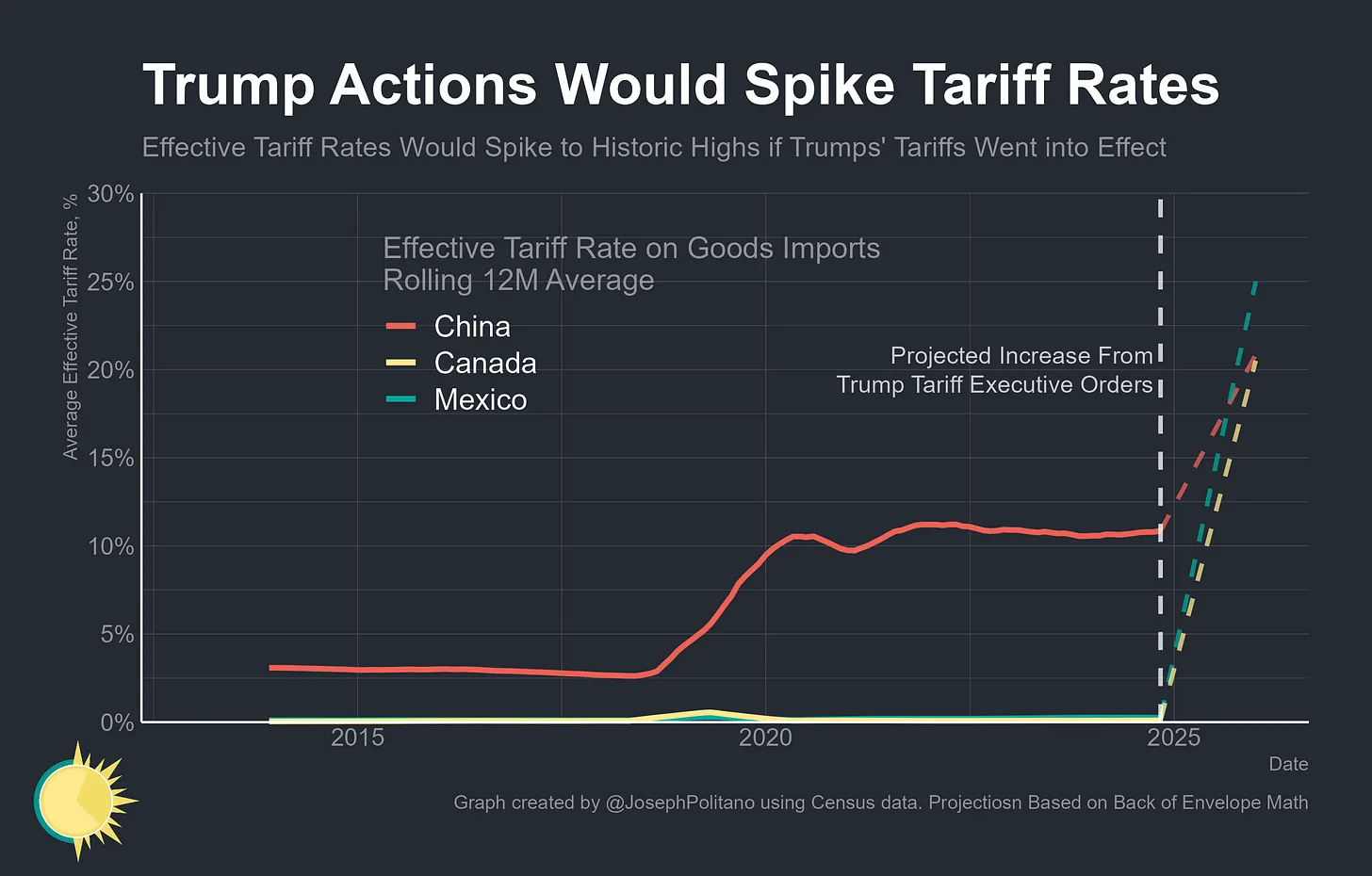

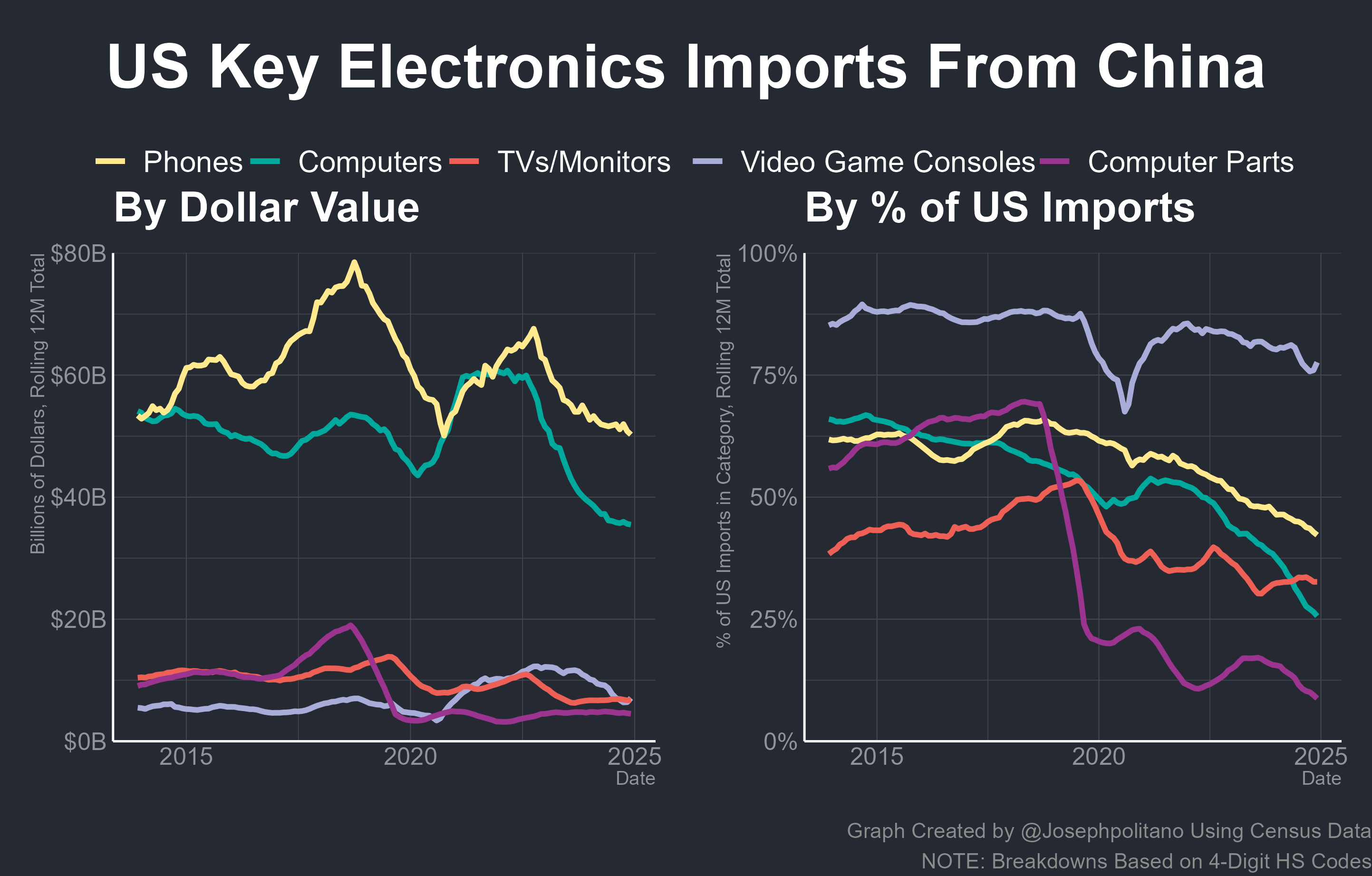

> A Detailed Look at the Economic Impacts of Trump's Wide Ranging New Tariffs on China, Mexico, Canada, Steel, Aluminum, and Much More

https://www.apricitas.io/p/trumps-2nd-trade-war-begins

If you're interested in global trade I recommend looking at the article. It's a real deep dive into many perspectives of US trade esp. with China. What gets imported from China, many individual product categories, what happened in round 1 in 2018 and so so much more. And lots of charts!

originally posted at https://stacker.news/items/896850

-

@ 57d1a264:69f1fee1

2025-02-25 13:24:49

Galoy released a new product called Lana, a platform for bitcoin loans. The team will provide an introduction and then we'll dive into the design.

To get you up to speed, check out the website, slide deck and podcast interview:

- https://www.galoy.io/lana-bitcoin-loans-platform

- https://docs.google.com/presentation/d/1IQocefpCN5_wKX91EWtLa19IpMS_Ye8goNLAgGQbfdU/edit#slide=id.g31d536107ae_0_0

- https://stephanlivera.com/episode/634/

If you get a chance, please take a peek before the call. That makes the design reviews more useful because we need to spend less time going over the basics.

On `Thu Feb 27th · 15:00 – 16:00 CET`

Join from https://meet.jit.si/bitcoindesign

Check your timezone https://everytimezone.com/s/998e22fc

Track https://github.com/BitcoinDesign/Meta/issues/758

originally posted at https://stacker.news/items/896570

-

@ 57d1a264:69f1fee1

2025-02-25 12:38:46

I've been pondering how LSPs (lightning service providers) might pan out over time and how that might affect fees, and I am wondering what everyone else is thinking. Some people will always prefer to manage their own channels, and for some specific use cases, that might be preferable. But I am thinking about the broad userbase that does not want to do that. We will need a massive LSP infrastructure to onboard people and to enable insane amounts of payments.

LSPs will need to efficiently open and adjust channels for users, using their own liquidity or sourcing liquidity from other providers, using just-in-time channels, batching and/or splicing to reduce costs and wait times. Across all this, along with facilitating payments, they need to make their business model work and offer different options for users to pay for their services.

Users might be able to:

1. Pay-as-you-go (pay X for Y more liquidity for Z amount of time)

2. Pay X per month for Y inbound liquidity

3. Pay X per month for unlimited liquidity

4. Nothing for liquidity, but higher transaction fees

A wallet might also automatically choose an appropriate LSP based on what is the best and most appropriate deal at the time.

Let's look at user scenarios:

- If someone sends and receives the same amount every month, they will never need more liquidity. They just draw down the same channel and fill it up again. So they would only pay the LSP for them assigning that fixed amount of liquidity to them. Maybe options 1 and 2 are good for them.

- If someone receives more than they send (they save a certain amount every month), they will need more and more inbound liquidity over time. They might choose option 2.

- An online store that receives a ton and can't really estimate how much, might go for option 3.

- For option 4, it depends if the higher transaction fees are fixed or percentage-based.

It's a bit like choosing a data plan for your phone (or for internet at home). You can get a prepaid card, a regular plan with certain limits, or go unlimited. And there are separate plans for small and large businesses, etc. And there are massive amounts of complex infrastructure behind these service providers to make it all work.

So when someone starts using a lightning wallet, maybe they have to first pick an LSP and a plan before being able to receive. Or maybe they get a first channel for free and pay higher fees, and are then prompted to choose a plan. Maybe they need to wait an hour until the LSP has enough channel opens for a batch/splice, to reduce costs. A complex market at work.

Is that how things might pan out? Am I completely off? Is it worth mocking up different scenarios?

```

#bitcoin #LN #BTC #Lightning #LSP #service #zaps #sats #wallet

```

originally posted at https://stacker.news/items/896520

-

@ 2063cd79:57bd1320

2025-02-25 10:44:02

Ich stimme mit Anonymous überein, dass es Probleme mit der tatsächlichen Verwendung von digitalem Bargeld auf kurze Sicht gibt. Aber es hängt in gewissem Maße davon ab, welches Problem man zu lösen versucht.

Eine Sorge, die ich habe, ist, dass der Übergang zum elektronischen Zahlungsverkehr die Privatsphäre einschränken wird, da es einfacher wird, Transaktionen zu protokollieren und aufzuzeichnen. Es könnten Profile angelegt werden, in denen das Ausgabeverhalten eines jeden von uns verfolgt wird.

Schon jetzt wird, wenn ich etwas telefonisch oder elektronisch mit meiner Visa-Karte bestelle, genau aufgezeichnet, wie viel ich ausgegeben habe und wo ich es ausgegeben habe. Im Laufe der Zeit könnten immer mehr Transaktionen auf diese Weise abgewickelt werden, und das Ergebnis könnte einen großen Verlust an Privatsphäre bedeuten.

Die Bezahlung mit Bargeld ist zwar immer noch per Post möglich, aber dies ist unsicher und umständlich. Ich denke, dass die Bequemlichkeit von Kredit- und Debitkarten die Bedenken der meisten Menschen in Bezug auf Privatsphäre ausräumen wird und dass wir uns in einer Situation befinden werden, in der große Mengen an Informationen über das Privatleben aller Leute existieren.

Hier könnte ich mir vorstellen, dass digitales Bargeld eine Rolle spielen könnte. Stellt euch ein Visa-ähnliches System vor, bei dem ich für die Bank nicht anonym bin. Stellt euch in diesem Modell vor, dass mir die Bank einen Kredit gewährt, ganz so wie bei einer Kreditkarte. Allerdings, anstatt mir nur eine Kontonummer zu geben, die ich am Telefon ablese oder in einer E-Mail verschicke, gibt sie mir das Recht, bei Bedarf digitales Bargeld zu verlangen.

Ich habe immer etwas digitales Bargeld beiseite, dass ich für Transaktionen ausgeben kann, wie bereits in früheren Beiträgen beschrieben. Wenn das Geld knapp wird, schicke ich eine E-Mail an die Bank und erhalte mehr digitales Bargeld (dcash). Jeden Monat sende ich einen Check an die Bank, um mein Konto auszugleichen, genauso wie ich es mit meinen Kreditkarten mache. Meine Beziehung zur Bank sind meinen derzeitigen Beziehungen zu den Kreditkartenunternehmen sehr ähnlich: häufige Überweisungen und eine einmalige Rückzahlung jeden Monat per Check.

Das hat mehrere Vorteile gegenüber dem System, auf das wir zusteuern. Es werden keine Aufzeichnungen darüber geführt, wofür ich mein Geld ausgebe. Die Bank weiß nur, wie viel ich jeden Monat abgehoben habe; es könnte sein, dass ich es zu diesem Zeitpunkt ausgegeben habe oder auch nicht. Bei einigen Transaktionen (z.B. Software) könnte ich für den Verkäufer anonym sein; bei anderen könnte der Verkäufer meine wirkliche Adresse kennen, aber dennoch ist keine zentrale Stelle in der Lage, alles zu verfolgen, was ich kaufe.

(Es gibt auch einen Sicherheitsvorteil gegenüber dem lächerlichen aktuellen System, bei dem die Kenntnis über eine 16-stellige Nummer und eines Ablaufdatums es jedem ermöglicht, etwas auf meinen Namen zu bestellen!)

Außerdem sehe ich nicht ein, warum dieses System nicht genauso legal sein sollte wie die derzeitigen Kreditkarten. Der einzige wirkliche Unterschied besteht darin, dass nicht nachverfolgt werden kann, wo die Nutzer ihr Geld ausgeben, und soweit ich weiß, war diese Möglichkeit nie ein wichtiger rechtlicher Aspekt von Kreditkarten. Sicherlich wird heute niemand zugeben, dass die Regierung ein Interesse daran hat, ein Umfeld zu schaffen, in dem jede finanzielle Transaktion nachverfolgt werden kann.

Zugegeben, dies bietet keine vollständige Anonymität. Es ist immer noch möglich, ungefähr zu sehen, wie viel jede Person ausgibt (obwohl nichts eine Person daran hindert, viel mehr Bargeld abzuheben, als sie in einem bestimmten Monat ausgibt, außer vielleicht für Zinsausgaben; aber vielleicht kann sie das zusätzliche digitale Bargel (digicash) selbst verleihen und dafür Zinsen erhalten, um das auszugleichen). Und es orientiert sich an demselben Kunden/ Verkäufer-Modell, das Anonymous kritisierte. Ich behaupte aber, dass dieses Modell heute und in naher Zukunft die Mehrheit der elektronischen Transaktionen ausmachen wird.

Es ist erwähnenswert, dass es nicht trivial ist, ein Anbieter zu werden, der Kreditkarten akzeptiert. Ich habe das mit einem Unternehmen, das ich vor ein paar Jahren betrieben habe, durchgemacht. Wir verkauften Software über den Versandhandel, was die Kreditkartenunternehmen sehr nervös machte. Es gibt zahlreiche Telefonbetrügereien, bei denen Kreditkartennummern über einige Monate hinweg gesammelt werden und dann große Beträge von diesen Karten abgebucht werden. Bis der Kunde seine monatliche Abrechnung erhält und sich beschwert, ist der Verkäufer bereits verschwunden. Um unser Kreditkartenterminal zu bekommen, wandten wir uns an ein Unternehmen, das Start-ups dabei „hilft“. Sie schienen selbst ein ziemlich zwielichtiges Unternehmen zu sein. Wir mussten unseren Antrag dahingehend fälschen, dass wir etwa 50% der Geräte auf Messen verkaufen würden, was offenbar als Verkauf über den Ladentisch zählte. Und wir mussten etwa 3.000 Dollar im Voraus zahlen, als Bestechung, wie es schien. Selbst dann hätten wir es wahrscheinlich nicht geschafft, wenn wir nicht ein Büro im Geschäftsviertel gehabt hätten.

Im Rahmen des digitalen Bargeldsystems könnte dies ein geringeres Problem darstellen. Das Hauptproblem bei digitalem Bargeld sind doppelte Ausgaben, und wenn man bereit ist, eine Online-Überprüfung vorzunehmen (sinnvoll für jedes Unternehmen, das mehr als ein paar Stunden für die Lieferung der Ware benötigt), kann dies vollständig verhindert werden. Es gibt also keine Möglichkeit mehr, dass Händler Kreditkartennummern für spätere Betrügereien sammeln. (Allerdings gibt es immer noch Probleme mit der Nichtlieferung von Waren, so dass nicht alle Risiken beseitigt sind). Dadurch könnte das System schließlich eine größere Verbreitung finden als die derzeitigen Kreditkarten.

Ich weiß nicht, ob dieses System zur Unterstützung von illegalen Aktivitäten, Steuerhinterziehung, Glücksspiel oder Ähnlichem verwendet werden könnte. Das ist nicht der Zweck dieses Vorschlags. Er bietet die Aussicht auf eine Verbesserung der Privatsphäre und der Sicherheit in einem Rahmen, der sogar rechtmäßig sein könnte, und das ist nicht verkehrt.

-----

Englischer Artikel erschienen im Nakamoto Institute: [Digital Cash & Privacy](https://nakamotoinstitute.org/library/digital-cash-and-privacy/here)

-

@ 57d1a264:69f1fee1

2025-02-25 07:28:18

@Voltage team will be building a simple implementation of a Lightning gated API service using a Voltage LND Node and the L402 protocol.

📅 Thursday, February 27th 4:00 PM CDT

📷 Live on Voltage Discord, on X, or on YouTube.

- discord.gg/EN93fDfQ

- https://x.com/voltage_cloud/status/1892938201980919985

- https://www.youtube.com/@voltage_cloud

originally posted at https://stacker.news/items/896373

-

@ 6389be64:ef439d32

2025-02-25 05:53:41

Biochar in the soil attracts microbes who take up permanent residence in the "coral reef" the biochar provides. Those microbes then attract mycorrhizal fungi to the reef. The mycorrhizal fungi are also attached to plant roots connecting diverse populations to each other, allowing transportation of molecular resources (water, cations, anions etc).

The char surface area attracts positively charged ions like

K+

Ca2+

Mg2+

NH4+

Na+

H+

Al3+

Fe2+

Fe3+

Mn2+

Cu2+

Zn2+

Many of these are transferred to plant roots by mycorrhizal fungi in exchange for photosynthetic products (sugars). Mycorrhizal fungi are connected to both plant roots and biochar. Char adsorbs these cations so, it stands to reason that under periods of minimal need by plants for these cations (stress, low or no sunlight etc.), mycorrhizal fungi could deposit the cations to the char surfaces. The char would be acting as a "bank" for the cations and the deposition would be of low energy cost.

Once the plant starts exuding photosynthetic products again, signaling a need for these cations, the fungi can start "stripping" the cations off of the char surface for immediate exchange of the cations for the sugars. This would be a high energy transaction because the fungi would have to expend energy to strip the cations off of the char surface, in effect, an "interest rate".

The char might act as a reservoir of cations that were mined by the fungi while the sugar flow from the roots was active. It's a bank.

originally posted at https://stacker.news/items/896340

-

@ 04c915da:3dfbecc9

2025-02-25 03:55:08

Here’s a revised timeline of macro-level events from *The Mandibles: A Family, 2029–2047* by Lionel Shriver, reimagined in a world where Bitcoin is adopted as a widely accepted form of money, altering the original narrative’s assumptions about currency collapse and economic control. In Shriver’s original story, the failure of Bitcoin is assumed amid the dominance of the bancor and the dollar’s collapse. Here, Bitcoin’s success reshapes the economic and societal trajectory, decentralizing power and challenging state-driven outcomes.

### Part One: 2029–2032

- **2029 (Early Year)**\

The United States faces economic strain as the dollar weakens against global shifts. However, Bitcoin, having gained traction emerges as a viable alternative. Unlike the original timeline, the bancor—a supranational currency backed by a coalition of nations—struggles to gain footing as Bitcoin’s decentralized adoption grows among individuals and businesses worldwide, undermining both the dollar and the bancor.

- **2029 (Mid-Year: The Great Renunciation)**\

Treasury bonds lose value, and the government bans Bitcoin, labeling it a threat to sovereignty (mirroring the original bancor ban). However, a Bitcoin ban proves unenforceable—its decentralized nature thwarts confiscation efforts, unlike gold in the original story. Hyperinflation hits the dollar as the U.S. prints money, but Bitcoin’s fixed supply shields adopters from currency devaluation, creating a dual-economy split: dollar users suffer, while Bitcoin users thrive.

- **2029 (Late Year)**\

Dollar-based inflation soars, emptying stores of goods priced in fiat currency. Meanwhile, Bitcoin transactions flourish in underground and online markets, stabilizing trade for those plugged into the bitcoin ecosystem. Traditional supply chains falter, but peer-to-peer Bitcoin networks enable local and international exchange, reducing scarcity for early adopters. The government’s gold confiscation fails to bolster the dollar, as Bitcoin’s rise renders gold less relevant.

- **2030–2031**\

Crime spikes in dollar-dependent urban areas, but Bitcoin-friendly regions see less chaos, as digital wallets and smart contracts facilitate secure trade. The U.S. government doubles down on surveillance to crack down on bitcoin use. A cultural divide deepens: centralized authority weakens in Bitcoin-adopting communities, while dollar zones descend into lawlessness.

- **2032**\

By this point, Bitcoin is de facto legal tender in parts of the U.S. and globally, especially in tech-savvy or libertarian-leaning regions. The federal government’s grip slips as tax collection in dollars plummets—Bitcoin’s traceability is low, and citizens evade fiat-based levies. Rural and urban Bitcoin hubs emerge, while the dollar economy remains fractured.

### Time Jump: 2032–2047

- Over 15 years, Bitcoin solidifies as a global reserve currency, eroding centralized control. The U.S. government adapts, grudgingly integrating bitcoin into policy, though regional autonomy grows as Bitcoin empowers local economies.

### Part Two: 2047

- **2047 (Early Year)**\

The U.S. is a hybrid state: Bitcoin is legal tender alongside a diminished dollar. Taxes are lower, collected in BTC, reducing federal overreach. Bitcoin’s adoption has decentralized power nationwide. The bancor has faded, unable to compete with Bitcoin’s grassroots momentum.

- **2047 (Mid-Year)**\

Travel and trade flow freely in Bitcoin zones, with no restrictive checkpoints. The dollar economy lingers in poorer areas, marked by decay, but Bitcoin’s dominance lifts overall prosperity, as its deflationary nature incentivizes saving and investment over consumption. Global supply chains rebound, powered by bitcoin enabled efficiency.

- **2047 (Late Year)**\

The U.S. is a patchwork of semi-autonomous zones, united by Bitcoin’s universal acceptance rather than federal control. Resource scarcity persists due to past disruptions, but economic stability is higher than in Shriver’s original dystopia—Bitcoin’s success prevents the authoritarian slide, fostering a freer, if imperfect, society.

### Key Differences

- **Currency Dynamics**: Bitcoin’s triumph prevents the bancor’s dominance and mitigates hyperinflation’s worst effects, offering a lifeline outside state control.

- **Government Power**: Centralized authority weakens as Bitcoin evades bans and taxation, shifting power to individuals and communities.

- **Societal Outcome**: Instead of a surveillance state, 2047 sees a decentralized, bitcoin driven world—less oppressive, though still stratified between Bitcoin haves and have-nots.

This reimagining assumes Bitcoin overcomes Shriver’s implied skepticism to become a robust, adopted currency by 2029, fundamentally altering the novel’s bleak trajectory.

-

@ d34e832d:383f78d0

2025-02-24 21:09:52

https://blossom.primal.net/af0bc86b52c7f91c26633ed0cba4f151bb74e5a5702b892f7f1efaa9e4640018.mp4

[npub16d8gxt2z4k9e8sdpc0yyqzf5gp0np09ls4lnn630qzxzvwpl0rgq5h4rzv]

### **What is Reticulum?**

Reticulum is a cryptographic networking stack designed for resilient, decentralized, and censorship-resistant communication. Unlike the traditional internet, Reticulum enables fully independent digital communications over various physical mediums, such as radio, LoRa, serial links, and even TCP/IP.

The key advantages of Reticulum include:

- **Decentralization** – No reliance on centralized infrastructure.

- **Encryption & Privacy** – End-to-end encryption built-in.

- **Resilience** – Operates over unreliable and low-bandwidth links.

- **Interoperability** – Works over WiFi, LoRa, Bluetooth, and more.

- **Ease of Use** – Can run on minimal hardware, including Raspberry Pi and embedded devices.

Reticulum is ideal for off-grid, censorship-resistant communications, emergency preparedness, and secure messaging.

---

## **1. Getting Started with Reticulum**

To quickly get started with Reticulum, follow the official guide:

[Reticulum: Getting Started Fast](https://markqvist.github.io/Reticulum/manual/gettingstartedfast.html)

### **Step 1: Install Reticulum**

#### **On Linux (Debian/Ubuntu-based systems)**

```sh

sudo apt update && sudo apt upgrade -y

sudo apt install -y python3-pip

pip3 install rns

```

#### **On Raspberry Pi or ARM-based Systems**

```sh

pip3 install rns

```

#### **On Windows**

Using Windows Subsystem for Linux (WSL) or Python:

```sh

pip install rns

```

#### **On macOS**

```sh

pip3 install rns

```

---

## **2. Configuring Reticulum**

Once installed, Reticulum needs a configuration file. The default location is:

```sh

~/.config/reticulum/config.toml

```

To generate the default configuration:

```sh

rnsd

```

This creates a configuration file with default settings.

---

## **3. Using Reticulum**

### **Starting the Reticulum Daemon**

To run the Reticulum daemon (`rnsd`), use:

```sh

rnsd

```

This starts the network stack, allowing applications to communicate over Reticulum.

### **Testing Your Reticulum Node**

Run the diagnostic tool to ensure your node is functioning:

```sh

rnstatus

```

This shows the status of all connected interfaces and peers.

---

## **4. Adding Interfaces**

### **LoRa Interface (for Off-Grid Communications)**

Reticulum supports long-range LoRa radios like the **RAK Wireless** and **Meshtastic devices**. To add a LoRa interface, edit `config.toml` and add:

```toml

[[interfaces]]

type = "LoRa"

name = "My_LoRa_Interface"

frequency = 868.0

bandwidth = 125

spreading_factor = 9

```

Restart Reticulum to apply the changes.

### **Serial (For Direct Device-to-Device Links)**

For communication over serial links (e.g., between two Raspberry Pis):

```toml

[[interfaces]]

type = "Serial"

port = "/dev/ttyUSB0"

baudrate = 115200

```

### **TCP/IP (For Internet-Based Nodes)**

If you want to bridge your Reticulum node over an existing IP network:

```toml

[[interfaces]]

type = "TCP"

listen = true

bind = "0.0.0.0"

port = 4242

```

---

## **5. Applications Using Reticulum**

### **LXMF (LoRa Mesh Messaging Framework)**

LXMF is a delay-tolerant, fully decentralized messaging system that operates over Reticulum. It allows encrypted, store-and-forward messaging without requiring an always-online server.

To install:

```sh

pip3 install lxmf

```

To start the LXMF node:

```sh

lxmfd

```

### **Nomad Network (Decentralized Chat & File Sharing)**

Nomad is a Reticulum-based chat and file-sharing platform, ideal for **off-grid** communication.

To install:

```sh

pip3 install nomad-network

```

To run:

```sh

nomad

```

### **Mesh Networking with Meshtastic & Reticulum**

Reticulum can work alongside **Meshtastic** for true decentralized long-range communication.

To set up a Meshtastic bridge:

```toml

[[interfaces]]

type = "LoRa"

port = "/dev/ttyUSB0"

baudrate = 115200

```

---

## **6. Security & Privacy Features**

- **Automatic End-to-End Encryption** – Every message is encrypted by default.

- **No Centralized Logging** – Communication leaves no metadata traces.

- **Self-Healing Routing** – Designed to work in unstable or hostile environments.

---

## **7. Practical Use Cases**

- **Off-Grid Communication** – Works in remote areas without cellular service.

- **Censorship Resistance** – Cannot be blocked by ISPs or governments.

- **Emergency Networks** – Enables resilient communication during disasters.

- **Private P2P Networks** – Create a secure, encrypted communication layer.

---

## **8. Further Exploration & Documentation**

- **Reticulum Official Manual**: [https://markqvist.github.io/Reticulum/manual/](https://markqvist.github.io/Reticulum/manual/)

- **Reticulum GitHub Repository**: [https://github.com/markqvist/Reticulum](https://github.com/markqvist/Reticulum)

- **Nomad Network**: [https://github.com/markqvist/NomadNet](https://github.com/markqvist/NomadNet)

- **Meshtastic + Reticulum**: [https://meshtastic.org](https://meshtastic.org)

---

## **Connections (Links to Other Notes)**

- **Mesh Networking for Decentralized Communication**

- **LoRa and Off-Grid Bitcoin Transactions**

- **Censorship-Resistant Communication Using Nostr & Reticulum**

## **Tags**

#Reticulum #DecentralizedComms #MeshNetworking #CensorshipResistance #LoRa

## **Donations via**

- **Bitcoin Lightning**: lightninglayerhash@getalby.com