-

@ ece127e2:745bab9c

2025-05-20 18:59:11

@ ece127e2:745bab9c

2025-05-20 18:59:11vamos a ver que tal

-

@ 5d4b6c8d:8a1c1ee3

2025-05-23 19:32:28

https://primal.net/e/nevent1qvzqqqqqqypzp6dtxy5uz5yu5vzxdtcv7du9qm9574u5kqcqha58efshkkwz6zmdqqszj207pl0eqkgld9vxknxamged64ch2x2zwhszupkut5v46vafuhg9833px

Some of my colleagues were talking about how they're even more scared of RFK Jr. than they are of Trump. I hope he earns it.

https://stacker.news/items/987685

-

@ 04c915da:3dfbecc9

2025-05-20 15:50:22

There is something quietly rebellious about stacking sats. In a world obsessed with instant gratification, choosing to patiently accumulate Bitcoin, one sat at a time, feels like a middle finger to the hype machine. But to do it right, you have got to stay humble. Stack too hard with your head in the clouds, and you will trip over your own ego before the next halving even hits.

Small Wins

Stacking sats is not glamorous. Discipline. Stacking every day, week, or month, no matter the price, and letting time do the heavy lifting. Humility lives in that consistency. You are not trying to outsmart the market or prove you are the next "crypto" prophet. Just a regular person, betting on a system you believe in, one humble stack at a time. Folks get rekt chasing the highs. They ape into some shitcoin pump, shout about it online, then go silent when they inevitably get rekt. The ones who last? They stack. Just keep showing up. Consistency. Humility in action. Know the game is long, and you are not bigger than it.

Ego is Volatile

Bitcoin’s swings can mess with your head. One day you are up 20%, feeling like a genius and the next down 30%, questioning everything. Ego will have you panic selling at the bottom or over leveraging the top. Staying humble means patience, a true bitcoin zen. Do not try to "beat” Bitcoin. Ride it. Stack what you can afford, live your life, and let compounding work its magic.

Simplicity

There is a beauty in how stacking sats forces you to rethink value. A sat is worth less than a penny today, but every time you grab a few thousand, you plant a seed. It is not about flaunting wealth but rather building it, quietly, without fanfare. That mindset spills over. Cut out the noise: the overpriced coffee, fancy watches, the status games that drain your wallet. Humility is good for your soul and your stack. I have a buddy who has been stacking since 2015. Never talks about it unless you ask. Lives in a decent place, drives an old truck, and just keeps stacking. He is not chasing clout, he is chasing freedom. That is the vibe: less ego, more sats, all grounded in life.

The Big Picture

Stack those sats. Do it quietly, do it consistently, and do not let the green days puff you up or the red days break you down. Humility is the secret sauce, it keeps you grounded while the world spins wild. In a decade, when you look back and smile, it will not be because you shouted the loudest. It will be because you stayed the course, one sat at a time. \ \ Stay Humble and Stack Sats. 🫡

-

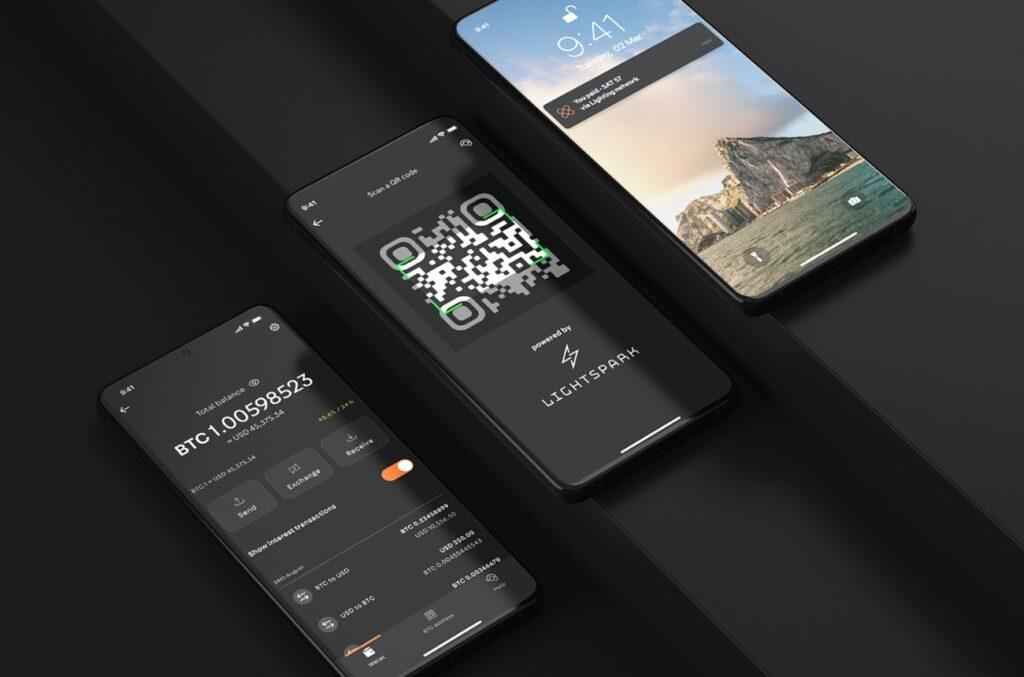

@ ecda4328:1278f072

2025-05-23 18:16:24

And what does it mean to withdraw back to Bitcoin Layer 1?

Disclaimer: This post was written with help from ChatGPT-4o. If you spot any mistakes or have suggestions — feel free to reply or zap in feedback!

Let’s break it down — using three popular setups:

1. Wallet of Satoshi (WoS)

Custodial — you don’t touch Lightning directly

Sending sats:

- You open WoS, paste a Lightning invoice, hit send.

- WoS handles the payment entirely within their system.

- If recipient uses WoS: internal balance update.

- If external: routed via their node.

- You never open channels, construct routes, or sign anything.

Withdrawing to L1:

- You paste a Bitcoin address.

- WoS sends a regular on-chain transaction from their custodial wallet.

- You pay a fee. It’s like a bank withdrawal.

You don’t interact with Lightning directly. Think of it as a trusted 3rd party Lightning “bank”.

2. Phoenix Wallet

Non-custodial — you own keys, Phoenix handles channels

Sending sats:

- You scan a Lightning invoice and hit send.

- Phoenix uses its backend node (ACINQ) to route the payment.

- If needed, it opens a real 2-of-2 multisig channel on-chain automatically.

- You own your keys (12-word seed), Phoenix abstracts the technical parts.

Withdrawing to L1:

- You enter your Bitcoin address.

- Phoenix closes your Lightning channel (cooperatively, if possible).

- Your sats are sent as a real Bitcoin transaction to your address.

You’re using Lightning “for real,” with real Bitcoin channels — but Phoenix smooths out the UX.

3. Your Own Lightning Node

Self-hosted — you control everything

Sending sats:

- You manage your channels manually (or via automation).

- Your node:

- Reads the invoice

- Builds a route using HTLCs

- Sends the payment using conditional logic (preimages, time locks).

- If routing fails: retry or adjust liquidity.

Withdrawing to L1:

- You select and close a channel.

- A channel closing transaction is broadcast:

- Cooperative = fast and cheap

- Force-close = slower, more expensive, and time-locked

- Funds land in your on-chain wallet.

You have full sovereignty — but also full responsibility (liquidity, fees, backups, monitoring).

Core Tech Behind It: HTLCs, Multisig — and No Sidechain

- Lightning channels = 2-of-2 multisig Bitcoin addresses

- Payments = routed via HTLCs (Hashed Time-Locked Contracts)

- HTLCs are off-chain, but enforceable on-chain if needed

- Important:

- The Lightning Network is not a sidechain.

- It doesn't use its own token, consensus, or separate blockchain.

- Every Lightning channel is secured by real Bitcoin on L1.

Lightning = fast, private, off-chain Bitcoin — secured by Bitcoin itself.

Summary Table

| Wallet | Custody | Channel Handling | L1 Withdrawal | HTLC Visibility | User Effort | |--------------------|--------------|------------------------|---------------------|------------------|--------------| | Wallet of Satoshi | Custodial | None | Internal to external| Hidden | Easiest | | Phoenix Wallet | Non-custodial| Auto-managed real LN | Channel close | Abstracted | Low effort | | Own Node | You | Manual | Manual channel close| Full control | High effort |

Bonus: Withdrawing from LN to On-Chain

- WoS: sends sats from their wallet — like PayPal.

- Phoenix: closes a real channel and sends your UTXO on-chain.

- Own node: closes your multisig contract and broadcasts your pre-signed tx.

Bitcoin + Lightning = Sovereign money + Instant payments.

Choose the setup that fits your needs — and remember, you can always level up later.P.S. What happens in Lightning... usually stays in Lightning.

-

@ 21335073:a244b1ad

2025-05-21 16:58:36

The other day, I had the privilege of sitting down with one of my favorite living artists. Our conversation was so captivating that I felt compelled to share it. I’m leaving his name out for privacy.

Since our last meeting, I’d watched a documentary about his life, one he’d helped create. I told him how much I admired his openness in it. There’s something strange about knowing intimate details of someone’s life when they know so little about yours—it’s almost like I knew him too well for the kind of relationship we have.

He paused, then said quietly, with a shy grin, that watching the documentary made him realize how “odd and eccentric” he is. I laughed and told him he’s probably the sanest person I know. Because he’s lived fully, chasing love, passion, and purpose with hardly any regrets. He’s truly lived.

Today, I turn 44, and I’ll admit I’m a bit eccentric myself. I think I came into the world this way. I’ve made mistakes along the way, but I carry few regrets. Every misstep taught me something. And as I age, I’m not interested in blending in with the world—I’ll probably just lean further into my own brand of “weird.” I want to live life to the brim. The older I get, the more I see that the “normal” folks often seem less grounded than the eccentric artists who dare to live boldly. Life’s too short to just exist, actually live.

I’m not saying to be strange just for the sake of it. But I’ve seen what the crowd celebrates, and I’m not impressed. Forge your own path, even if it feels lonely or unpopular at times.

It’s easy to scroll through the news and feel discouraged. But actually, this is one of the most incredible times to be alive! I wake up every day grateful to be here, now. The future is bursting with possibility—I can feel it.

So, to my fellow weirdos on nostr: stay bold. Keep dreaming, keep pushing, no matter what’s trending. Stay wild enough to believe in a free internet for all. Freedom is radical—hold it tight. Live with the soul of an artist and the grit of a fighter. Thanks for inspiring me and so many others to keep hoping. Thank you all for making the last year of my life so special.

-

@ 51bbb15e:b77a2290

2025-05-21 00:24:36

Yeah, I’m sure everything in the file is legit. 👍 Let’s review the guard witness testimony…Oh wait, they weren’t at their posts despite 24/7 survellience instructions after another Epstein “suicide” attempt two weeks earlier. Well, at least the video of the suicide is in the file? Oh wait, a techical glitch. Damn those coincidences!

At this point, the Trump administration has zero credibility with me on anything related to the Epstein case and his clients. I still suspect the administration is using the Epstein files as leverage to keep a lot of RINOs in line, whereas they’d be sabotaging his agenda at every turn otherwise. However, I just don’t believe in ends-justify-the-means thinking. It’s led almost all of DC to toss out every bit of the values they might once have had.

-

@ 9ca447d2:fbf5a36d

2025-05-22 14:01:52

Gen Z (those born between 1997 and 2012) are not rushing to stack sats, and Oliver Porter, Founder & CEO of Jippi, understands the challenge better than most. His strategy revolves around adapting Bitcoin education to fit seamlessly into the digital lives of young adults.

“We need to meet them where they are,” Oliver explains. “90% of Gen Z plays games. 70% expect to earn rewards.”

So, what will effectively introduce them to Bitcoin? In Oliver’s mind, the answer is simple: games that don’t feel preachy but still plant the orange pill.

Learn more at Jippi.app

That’s exactly what Jippi is. Based in Austin, Texas, the team has created a mobile augmented reality (AR) game that rewards players in bitcoin and sneakily teaches them why sound money matters.

“It’s Pokémon GO… but for sats,” Oliver puts it succinctly.

Jippi is like Pokemon Go, but for sats

Oliver’s Bitcoin journey, like many in the space, began long before he was ready. A former colleague had tried planting the seed years earlier, handing him a copy of The Bitcoin Standard. But the moment passed.

It wasn’t until the chaos of 2020 when lockdowns hit, printing presses roared, and civil liberties shrank that the message finally landed for him.

“The government got so good at doing reverse Robin Hood,” Oliver explains. “They steal from the working population and reward the rich.”

By 2020, though, the absurdity of the covid hysteria had caused his eyes to be opened and the orange light seemed the best path back to freedom.

He left the UK for Austin “one of the best places for Bitcoiners,” he says, and dove headfirst into the industry, working at Swan for a year before founding Jippi on PlebLab’s accelerator program.

Jippi’s flagship game lets players roam their cities hunting digital creatures, Bitcoin Beasts, tied to real-world locations. Catching them requires answering Bitcoin trivia, and the reward is sats.

No jargon. No hour-long lectures. Just gameplay with sound money principles woven right in.

The model is working. At a recent hackathon in Austin, Jippi beat out 14 other teams to win first place and $15,000 in prize money.

Oliver of Jippi won Top Builder Season 2 — PlebLab on X

“We’re backdooring Bitcoin education,” Oliver admits. “And while we’re at it, encouraging people to get outside and touch grass.”

Not everyone’s been thrilled. When Jippi team members visited one of the more liberal-leaning places in Texas, UT Austin, to test interest in Bitcoin, they found some seriously committed no-coiners on the campus.

“One young woman told me, ‘I would rather die than talk about Bitcoin,'” Oliver recalls, highlighting the cultural resistance that’s built up among younger demographics.

This resistance is backed by hard data. According to Oliver, some of the Bitcoin podcasters they met with in the space to do market research reported that less than 1% of their listeners are from Gen Z and that number is dropping.

“Unless we find a way to capture their interest in a meaningful way, there’s going to be a big problem around trying to sway Gen Z away from the siren call of s***coins and crypto casinos and towards Bitcoin,” Oliver warns.

Jippi’s next big move is Las Vegas, where they’ll launch the Beast Catch experience at the Venetian during a major Bitcoin event. To mark the occasion, they’re opening up six limited sponsorship spots for Bitcoin companies, each one tied to a custom in-game beast.

Jippi looks to launch a special event at Bitcoin 2025

“It’s real estate inside the game,” Oliver explains. “Brands become allies, not intrusions. You get a logo, company name, and call to action, so we can push people to your site or app.”

Bitcoin Well—an automatic self-custody Bitcoin platform—has claimed Beast #1. Only five exclusive spots remain for Bitcoin companies to “beastify their brand” through Jippi’s immersive AR game.

“I love the Jippi mission. I think gamified learning is how we will onboard the next generation and it’s exciting to see what the Jippi team is doing! I love working with bitcoiners towards our common mission – bullish!” said Adam O’Brien, Bitcoin Well CEO.

Jippi’s sponsorship model is simple: align incentives, respect users, and support builders. Instead of throwing ad money at tech giants, Bitcoin companies can connect with new users naturally while they’re having fun and earning sats in the process.

For Bitcoin companies looking to reach a younger demographic, this represents a unique opportunity to showcase their brand to up to 30,000 potential customers at the Vegas event.

Jippi Bitcoin Beast partnership

While Jippi’s current focus is simple, get the game into more cities, Oliver sees a future where AR glasses and AI help personalize Bitcoin education even further.

“The magic is going to really happen when Apple releases the glasses form factor,” he says, describing how augmented reality could enhance real-world connections rather than isolate users.

In the longer term, Jippi aims to evolve from a free-to-play model toward a pay-to-play version with higher stakes. Users would form “tribes” with friends to compete for substantial bitcoin prizes, creating social connections along with financial education.

Unlike VC-backed startups, Jippi is raising funds pleb style via Timestamp, an open investment platform for Bitcoin companies.

“You don’t have to be an accredited investor,” Oliver explains. “You’re directly supporting the parallel Bitcoin economy by investing in Bitcoin companies for equity.”

Anyone can invest as little as $100. Perks include early access, exclusive game content, and even creating your own beast design with your name/pseudonym and unique game lore. Each investment comes with direct ownership of an early-stage Bitcoin company like Jippi.

For Oliver, this is more than just a business. It’s about future-proofing Bitcoin adoption and ensuring Satoshi’s vision lives on, especially as many people are lured by altcoins, NFTs, and social media dopamine.

“We’re on the right side of history,” he says firmly. “I want my grandkids to know that early on in the Bitcoin revolution, games like Jippi helped make it stick.”

In a world increasingly absorbed by screens and short attention spans, Jippi’s combination of outdoor play, sats rewards, and Bitcoin education might be exactly the bridge Gen Z needs.

Interested in sponsoring a Beast or investing in Jippi? Reach out to Jippi directly by heading to their partnerships page on their website or visit their Timestamp page to invest in Jippi today.

-

@ bf47c19e:c3d2573b

2025-05-23 22:14:37

Originalni tekst na antenam.net

22.05.2025 / Autor: Ana Nives Radović

Da nema besplatnog ručka sigurno ste čuli svaki put kad bi neko poželio da naglasi da se sve na neki način plaća, iako možda tu cijenu ne primjećujemo odmah. Međutim, kada govorimo o događaju od kojeg je prošlo tačno 15 godina onda o „ručku“ ne govorimo u prenešenom smislu, već o porudžbini pice čija tržišna vrijednost iz godine u godinu dostiže iznos koji je čini najskupljom hranom koja je ikad poručena.

Tog 22. maja 2010. godine čovjek sa Floride pod imenom Laslo Hanjec potrošio je 10.000 bitcoina na dvije velike pice. U to vrijeme, ta količina bitcoina imala je tržišnu vrijednost od oko 41 dolar. Ako uzmemo u obzir da je vrijednost jedne jedinice ove digitalne valute danas nešto više od 111.000 dolara, tih 10.000 bitcoina danas bi značilo vrijednost od 1,11 milijardi dolara.

Nesvakidašnji događaj u digitalnoj i ugostiteljskoj istoriji, nastao zbog znatiželje poručioca koji je želio da se uvjeri da koristeći bitcoin može da plati nešto u stvarnom svijetu, pretvorio se u Bitcoin Pizza Day, kao podsjetnik na trenutak koji je označio prelaz bitcoina iz apstraktnog kriptografskog eksperimenta u nešto što ima stvarnu vrijednost.

Hanjec je bio znatiželjan i pitao se da li se prva, a u to vrijeme i jedina kriptovaluta može iskoristiti za kupovinu nečeg opipljivog. Objavio je ponudu na jednom forumu koja je glasila: 10.000 BTC za dvije pice. Jedan entuzijasta se javio, naručio pice iz restorana Papa John’s i ispisao zanimljivu stranicu istorije digitalne imovine.

Taj inicijalni zabilježeni finansijski dogovor dao je bitcoinu prvu široko prihvaćenu tržišnu vrijednost: 10.000 BTC za 41 dolar, čime je bitcoin napravio svoj prvi korak ka onome što danas mnogi zovu digitalnim zlatom.

Šta je zapravo bitcoin?

Bitcoin je oblik digitalnog novca koji je osmišljen da bude decentralizovan, transparentan i otporan na uticaj centralnih banaka. Kreirao ga je 2009. godine anonimni autor poznat kao Satoši Nakamoto, neposredno nakon globalne finansijske krize 2008. godine. U svojoj suštini, bitcoin je protokol, skup pravila koja sprovodi kompjuterski kod, koji omogućava korisnicima da bez posrednika sigurno razmjenjuju vrijednost putem interneta.

Osnova cijelog sistema je blockchain, distribuisana digitalna knjiga koju održavaju hiljade nezavisnih računara (tzv. čvorova) širom svijeta. Svaka transakcija se bilježi u novi „blok“, koji se potom dodaje u lanac (otud naziv „lanac blokova“, odnosno blockchain). Informacija koja se jednom upiše u blok ne može da se izbriše, niti promijeni, što omogućava više transparentnosti i više povjerenja.

Da bi blockchain mreža u kojoj se sve to odvija zadržala to svojstvo, bitcoin koristi mehanizam konsenzusa nazvan dokaz rada (proof-of-work), što znači da specijalizovani računari koji „rudare“ bitcoin rješavaju kompleksne matematičke probleme kako bi omogućili obavljanje transakcija i pouzdanost mreže.

Deflatorna priroda bitcoina

Najjednostavniji način da se razumije deflatorna priroda bitcoina je da pogledamo cijene izražene u valuti kojoj plaćamo. Sigurno ste u posljednje vrijeme uhvatili sebe da komentarišete da ono što je prije nekoliko godina koštalo 10 eura danas košta 15 ili više. Budući da to ne zapažate kada je u pitanju cijena samo određenog proizvoda ili usluge, već kao sveprisutan trend, shvatate da se radi o tome da je novac izgubio vrijednost. Na primjer, kada je riječ o euru, otkako je Evropska centralna banka počela intenzivno da doštampava novac svake godine, pa je od 2009. kada je program tzv. „kvantitativnog popuštanja“ započet euro zabilježio kumulativnu inflaciju od 42,09% zbog povećane količine sredstava u opticaju.

Međutim, kada je riječ o bitcoinu, njega nikada neće biti više od 21 milion koliko je izdato prvog dana, a to nepromjenjivo pravilo zapisano je i u njegovom kodu. Ova ograničena ponuda oštro se suprotstavlja principima koji važe kod monetarnih institucija, poput centralnih banaka, koje doštampavaju novac, često da bi povećale količinu u opticaju i tako podstakle finansijske tokove, iako novac zbog toga gubi vrijednost. Nasuprot tome, bitcoin se zadržava na iznosu od 21 milion, pa je upravo ta konačnost osnova za njegovu deflatornu prirodu i mogućnost da vremenom dobija na vrijednosti.

Naravno, ovo ne znači da je cijena bitcoina predodređena da samo raste. Ona je zapravo prilično volatilna i oscilacije su česte, posebno ukoliko, na primjer, posmatramo odnos cijena unutar jedne godine ili nekoliko mjeseci, međutim, gledano sa vremenske distance od četiri do pet godina bilo koji uporedni period od nastanka bitcoina do danas upućuje na to da je cijena u međuvremenu porasla. Taj trend će se nastaviti, tako da, kao ni kada je riječ o drugim sredstvima, poput zlata ili nafte, nema mjesta konstatacijama da je „vrijeme niskih cijena prošlo“.

Šta zapravo znači ovaj dan?

Bitcoin Pizza Day je za mnoge prilika da saznaju ponešto novo o bitcoinu, jer tada imaju priliku da o njemu čuju detalje sa raznih strana, jer kako se ovaj događaj popularizuje stvaraju se i nove prilike za učenje. Takođe, ovaj dan od 2021. obilježavaju picerije širom svijeta, u više od 400 gradova iz najmanje 75 zemalja, jer je za mnoge ovo prilika da korisnike bitcoina navedu da potroše djelić svoje imovine na nešto iz njihove ponude. Naravno, taj iznos je danasd zanemarljivo mali, a cijena jedne pice danas je otprilike 0,00021 bitcoina.

No, dok picerije širom svijeta danas na zabavan način pokušavaju da dođu do novih gostiju, ovaj dan je za mnoge vlasnike bitcoina nešto poput opomene da svoje digitalne novčiće ipak ne treba trošiti na nešto potrošno, jer je budućnost nepredvidiva. Bitcoin Pizza Day je dan kada se ideja pretvorila u valutu, kada su linije koda postale sredstvo razmjene.

Prvi let avionom trajao je svega 12 sekundi, a u poređenju sa današnjim transkontinentalnim linijama to djeluje gotovo neuporedivo i čudno, međutim, od nečega je moralo početi. Porudžbina pice plaćene bitcoinom označile su početak razmjene ove vrste, dok se, na primjer, tokom jučerašnjeg dana obim plaćanja bitcoinom premašio 23 milijarde dolara. Nauka i tehnologija nas podsjećaju na to da sve počinje malim, zanemarivim koracima.

-

@ 57d1a264:69f1fee1

2025-05-22 13:13:36

Graphics materials for Bitcoin Knots https://github.com/bitcoinknots branding. See below guide image for reference, a bit cleaner and scalable:

Font family "Aileron" is provided free for personal and commercial use, and can be found here: https://www.1001fonts.com/aileron-font.html

Source: https://github.com/Blissmode/bitcoinknots-gfx/tree/main

https://stacker.news/items/986624

-

@ c9badfea:610f861a

2025-05-20 19:49:20

- Install Sky Map (it's free and open source)

- Launch the app and tap Accept, then tap OK

- When asked to access the device's location, tap While Using The App

- Tap somewhere on the screen to activate the menu, then tap ⁝ and select Settings

- Disable Send Usage Statistics

- Return to the main screen and enjoy stargazing!

ℹ️ Use the 🔍 icon in the upper toolbar to search for a specific celestial body, or tap the 👁️ icon to activate night mode

-

@ bf47c19e:c3d2573b

2025-05-23 21:54:43

Srpski prevod knjige "The Little Bitcoin Book"

Zašto je Bitkoin bitan za vašu slobodu, finansije i budućnost?

Verovatno ste čuli za Bitkoin u vestima ili da o njemu raspravljaju vaši prijatelji ili kolege. Kako to da se cena stalno menja? Da li je Bitkoin dobra investicija? Kako to uopšte ima vrednost? Zašto ljudi stalno govore o tome kao da će promeniti svet?

"Mala knjiga o Bitkoinu" govori o tome šta nije u redu sa današnjim novcem i zašto je Bitkoin izmišljen da obezbedi alternativu trenutnom sistemu. Jednostavnim rečima opisuje šta je Bitkoin, kako funkcioniše, zašto je vredan i kako utiče na individualnu slobodu i mogućnosti ljudi svuda - od Nigerije preko Filipina do Venecuele do Sjedinjenih Država. Ova knjiga takođe uključuje odeljak "Pitanja i odgovori" sa nekim od najčešće postavljanih pitanja o Bitkoinu.

Ako želite da saznate više o ovom novom obliku novca koji i dalje izaziva interesovanje i usvajanje širom sveta, onda je ova knjiga za vas.

-

@ 57d1a264:69f1fee1

2025-05-22 12:36:20

Graphics materials for Bitcoin Knots https://github.com/bitcoinknots branding. See below guide image for reference, a bit cleaner and scalable:

Font family "Aileron" is provided free for personal and commercial use, and can be found here: https://www.1001fonts.com/aileron-font.html

Source: https://github.com/Blissmode/bitcoinknots-gfx/tree/main

https://stacker.news/items/986587

-

@ 57d1a264:69f1fee1

2025-05-22 06:21:22

You’ve probably seen it before.

You open an agency’s website or a freelancer’s portfolio. At the very top of the homepage, it says:

We design for startups.

You wait 3 seconds. The last word fades out and a new one fades in:

We design for agencies.

Wait 3 more seconds:

We design for founders.

I call this design pattern The Wheel of Nothing: a rotating list of audience segments meant to impress through inclusion and draw attention through motion… for absolutely no reason.

Revered brand studio Pentagram recently launched a new website. To my surprise, the homepage features the Wheel of Nothing front and center, boldly claiming:

We design Everything for Everyone…before cycling through more specific combinations every few seconds.

Dan Mall, a husband, dad, teacher, creative director, designer, founder, and entrepreneur from Philly. I share as much as I can to create better opportunities for those who wouldn’t have them otherwise. Most recently, I ran design system consultancy SuperFriendly for over a decade.

Read more at Dans' website https://danmall.com/posts/the-wheel-of-nothing/

https://stacker.news/items/986392

-

@ 04c915da:3dfbecc9

2025-05-20 15:53:48

This piece is the first in a series that will focus on things I think are a priority if your focus is similar to mine: building a strong family and safeguarding their future.

Choosing the ideal place to raise a family is one of the most significant decisions you will ever make. For simplicity sake I will break down my thought process into key factors: strong property rights, the ability to grow your own food, access to fresh water, the freedom to own and train with guns, and a dependable community.

A Jurisdiction with Strong Property Rights

Strong property rights are essential and allow you to build on a solid foundation that is less likely to break underneath you. Regions with a history of limited government and clear legal protections for landowners are ideal. Personally I think the US is the single best option globally, but within the US there is a wide difference between which state you choose. Choose carefully and thoughtfully, think long term. Obviously if you are not American this is not a realistic option for you, there are other solid options available especially if your family has mobility. I understand many do not have this capability to easily move, consider that your first priority, making movement and jurisdiction choice possible in the first place.

Abundant Access to Fresh Water

Water is life. I cannot overstate the importance of living somewhere with reliable, clean, and abundant freshwater. Some regions face water scarcity or heavy regulations on usage, so prioritizing a place where water is plentiful and your rights to it are protected is critical. Ideally you should have well access so you are not tied to municipal water supplies. In times of crisis or chaos well water cannot be easily shutoff or disrupted. If you live in an area that is drought prone, you are one drought away from societal chaos. Not enough people appreciate this simple fact.

Grow Your Own Food

A location with fertile soil, a favorable climate, and enough space for a small homestead or at the very least a garden is key. In stable times, a small homestead provides good food and important education for your family. In times of chaos your family being able to grow and raise healthy food provides a level of self sufficiency that many others will lack. Look for areas with minimal restrictions, good weather, and a culture that supports local farming.

Guns

The ability to defend your family is fundamental. A location where you can legally and easily own guns is a must. Look for places with a strong gun culture and a political history of protecting those rights. Owning one or two guns is not enough and without proper training they will be a liability rather than a benefit. Get comfortable and proficient. Never stop improving your skills. If the time comes that you must use a gun to defend your family, the skills must be instinct. Practice. Practice. Practice.

A Strong Community You Can Depend On

No one thrives alone. A ride or die community that rallies together in tough times is invaluable. Seek out a place where people know their neighbors, share similar values, and are quick to lend a hand. Lead by example and become a good neighbor, people will naturally respond in kind. Small towns are ideal, if possible, but living outside of a major city can be a solid balance in terms of work opportunities and family security.

Let me know if you found this helpful. My plan is to break down how I think about these five key subjects in future posts.

-

@ 5144fe88:9587d5af

2025-05-23 17:01:37

The recent anomalies in the financial market and the frequent occurrence of world trade wars and hot wars have caused the world's political and economic landscape to fluctuate violently. It always feels like the financial crisis is getting closer and closer.

This is a systematic analysis of the possibility of the current global financial crisis by Manus based on Ray Dalio's latest views, US and Japanese economic and financial data, Buffett's investment behavior, and historical financial crises.

Research shows that the current financial system has many preconditions for a crisis, especially debt levels, market valuations, and investor behavior, which show obvious crisis signals. The probability of a financial crisis in the short term (within 6-12 months) is 30%-40%,

in the medium term (within 1-2 years) is 50%-60%,

in the long term (within 2-3 years) is 60%-70%.

Japan's role as the world's largest holder of overseas assets and the largest creditor of the United States is particularly critical. The sharp appreciation of the yen may be a signal of the return of global safe-haven funds, which will become an important precursor to the outbreak of a financial crisis.

Potential conditions for triggering a financial crisis Conditions that have been met 1. High debt levels: The debt-to-GDP ratio of the United States and Japan has reached a record high. 2. Market overvaluation: The ratio of stock market to GDP hits a record high 3. Abnormal investor behavior: Buffett's cash holdings hit a record high, with net selling for 10 consecutive quarters 4. Monetary policy shift: Japan ends negative interest rates, and the Fed ends the rate hike cycle 5. Market concentration is too high: a few technology stocks dominate market performance

Potential trigger points 1. The Bank of Japan further tightens monetary policy, leading to a sharp appreciation of the yen and the return of overseas funds 2. The US debt crisis worsens, and the proportion of interest expenses continues to rise to unsustainable levels 3. The bursting of the technology bubble leads to a collapse in market confidence 4. The trade war further escalates, disrupting global supply chains and economic growth 5. Japan, as the largest creditor of the United States, reduces its holdings of US debt, causing US debt yields to soar

Analysis of the similarities and differences between the current economic environment and the historical financial crisis Debt level comparison Current debt situation • US government debt to GDP ratio: 124.0% (December 2024) • Japanese government debt to GDP ratio: 216.2% (December 2024), historical high 225.8% (March 2021) • US total debt: 36.21 trillion US dollars (May 2025) • Japanese debt/GDP ratio: more than 250%-263% (Japanese Prime Minister’s statement)

Before the 2008 financial crisis • US government debt to GDP ratio: about 64% (2007) • Japanese government debt to GDP ratio: about 175% (2007)

Before the Internet bubble in 2000 • US government debt to GDP ratio: about 55% (1999) • Japanese government debt to GDP ratio: about 130% (1999)

Key differences • The current US debt-to-GDP ratio is nearly twice that before the 2008 crisis • The current Japanese debt-to-GDP ratio is more than 1.2 times that before the 2008 crisis • Global debt levels are generally higher than historical pre-crisis levels • US interest payments are expected to devour 30% of fiscal revenue (Moody's warning)

Monetary policy and interest rate environment

Current situation • US 10-year Treasury yield: about 4.6% (May 2025) • Bank of Japan policy: end negative interest rates and start a rate hike cycle • Bank of Japan's holdings of government bonds: 52%, plans to reduce purchases to 3 trillion yen per month by January-March 2026 • Fed policy: end the rate hike cycle and prepare to cut interest rates

Before the 2008 financial crisis • US 10-year Treasury yield: about 4.5%-5% (2007) • Fed policy: continuous rate hikes from 2004 to 2006, and rate cuts began in 2007 • Bank of Japan policy: maintain ultra-low interest rates

Key differences • Current US interest rates are similar to those before the 2008 crisis, but debt levels are much higher than then • Japan is in the early stages of ending its loose monetary policy, unlike before historical crises • The size of global central bank balance sheets is far greater than at any time in history

Market valuations and investor behavior Current situation • The ratio of stock market value to the size of the US economy: a record high • Buffett's cash holdings: $347 billion (28% of assets), a record high • Market concentration: US stock growth mainly relies on a few technology giants • Investor sentiment: Technology stocks are enthusiastic, but institutional investors are beginning to be cautious

Before the 2008 financial crisis • Buffett's cash holdings: 25% of assets (2005) • Market concentration: Financial and real estate-related stocks performed strongly • Investor sentiment: The real estate market was overheated and subprime products were widely popular

Before the 2000 Internet bubble • Buffett's cash holdings: increased from 1% to 13% (1998) • Market concentration: Internet stocks were extremely highly valued • Investor sentiment: Tech stocks are in a frenzy

Key differences • Buffett's current cash holdings exceed any pre-crisis level in history • Market valuation indicators have reached a record high, exceeding the levels before the 2000 bubble and the 2008 crisis • The current market concentration is higher than any period in history, and a few technology stocks dominate market performance

Safe-haven fund flows and international relations Current situation • The status of the yen: As a safe-haven currency, the appreciation of the yen may indicate a rise in global risk aversion • Trade relations: The United States has imposed tariffs on Japan, which is expected to reduce Japan's GDP growth by 0.3 percentage points in fiscal 2025 • International debt: Japan is one of the largest creditors of the United States

Before historical crises • Before the 2008 crisis: International capital flows to US real estate and financial products • Before the 2000 bubble: International capital flows to US technology stocks

Key differences • Current trade frictions have intensified and the trend of globalization has weakened • Japan's role as the world's largest holder of overseas assets has become more prominent • International debt dependence is higher than any period in history

-

@ 04c915da:3dfbecc9

2025-05-20 15:47:16

Here’s a revised timeline of macro-level events from The Mandibles: A Family, 2029–2047 by Lionel Shriver, reimagined in a world where Bitcoin is adopted as a widely accepted form of money, altering the original narrative’s assumptions about currency collapse and economic control. In Shriver’s original story, the failure of Bitcoin is assumed amid the dominance of the bancor and the dollar’s collapse. Here, Bitcoin’s success reshapes the economic and societal trajectory, decentralizing power and challenging state-driven outcomes.

Part One: 2029–2032

-

2029 (Early Year)\ The United States faces economic strain as the dollar weakens against global shifts. However, Bitcoin, having gained traction emerges as a viable alternative. Unlike the original timeline, the bancor—a supranational currency backed by a coalition of nations—struggles to gain footing as Bitcoin’s decentralized adoption grows among individuals and businesses worldwide, undermining both the dollar and the bancor.

-

2029 (Mid-Year: The Great Renunciation)\ Treasury bonds lose value, and the government bans Bitcoin, labeling it a threat to sovereignty (mirroring the original bancor ban). However, a Bitcoin ban proves unenforceable—its decentralized nature thwarts confiscation efforts, unlike gold in the original story. Hyperinflation hits the dollar as the U.S. prints money, but Bitcoin’s fixed supply shields adopters from currency devaluation, creating a dual-economy split: dollar users suffer, while Bitcoin users thrive.

-

2029 (Late Year)\ Dollar-based inflation soars, emptying stores of goods priced in fiat currency. Meanwhile, Bitcoin transactions flourish in underground and online markets, stabilizing trade for those plugged into the bitcoin ecosystem. Traditional supply chains falter, but peer-to-peer Bitcoin networks enable local and international exchange, reducing scarcity for early adopters. The government’s gold confiscation fails to bolster the dollar, as Bitcoin’s rise renders gold less relevant.

-

2030–2031\ Crime spikes in dollar-dependent urban areas, but Bitcoin-friendly regions see less chaos, as digital wallets and smart contracts facilitate secure trade. The U.S. government doubles down on surveillance to crack down on bitcoin use. A cultural divide deepens: centralized authority weakens in Bitcoin-adopting communities, while dollar zones descend into lawlessness.

-

2032\ By this point, Bitcoin is de facto legal tender in parts of the U.S. and globally, especially in tech-savvy or libertarian-leaning regions. The federal government’s grip slips as tax collection in dollars plummets—Bitcoin’s traceability is low, and citizens evade fiat-based levies. Rural and urban Bitcoin hubs emerge, while the dollar economy remains fractured.

Time Jump: 2032–2047

- Over 15 years, Bitcoin solidifies as a global reserve currency, eroding centralized control. The U.S. government adapts, grudgingly integrating bitcoin into policy, though regional autonomy grows as Bitcoin empowers local economies.

Part Two: 2047

-

2047 (Early Year)\ The U.S. is a hybrid state: Bitcoin is legal tender alongside a diminished dollar. Taxes are lower, collected in BTC, reducing federal overreach. Bitcoin’s adoption has decentralized power nationwide. The bancor has faded, unable to compete with Bitcoin’s grassroots momentum.

-

2047 (Mid-Year)\ Travel and trade flow freely in Bitcoin zones, with no restrictive checkpoints. The dollar economy lingers in poorer areas, marked by decay, but Bitcoin’s dominance lifts overall prosperity, as its deflationary nature incentivizes saving and investment over consumption. Global supply chains rebound, powered by bitcoin enabled efficiency.

-

2047 (Late Year)\ The U.S. is a patchwork of semi-autonomous zones, united by Bitcoin’s universal acceptance rather than federal control. Resource scarcity persists due to past disruptions, but economic stability is higher than in Shriver’s original dystopia—Bitcoin’s success prevents the authoritarian slide, fostering a freer, if imperfect, society.

Key Differences

- Currency Dynamics: Bitcoin’s triumph prevents the bancor’s dominance and mitigates hyperinflation’s worst effects, offering a lifeline outside state control.

- Government Power: Centralized authority weakens as Bitcoin evades bans and taxation, shifting power to individuals and communities.

- Societal Outcome: Instead of a surveillance state, 2047 sees a decentralized, bitcoin driven world—less oppressive, though still stratified between Bitcoin haves and have-nots.

This reimagining assumes Bitcoin overcomes Shriver’s implied skepticism to become a robust, adopted currency by 2029, fundamentally altering the novel’s bleak trajectory.

-

-

@ c6d8334c:30883d6d

2025-05-20 14:23:40

🧭 Ausgangspunkt

Die Nutzung generativer KI in der Bildung verändert unsere Formen der Kommunikation grundlegend. Gerade in der religiösen Bildung stellt sich die Frage, wie Sprachmodelle über Weltbilder, Ethik und Religion sprechen – und mit welchen (un)bewussten Vorannahmen. Inspiriert vom sokratischen Dialog erarbeiten wir gemeinsam, wie KI über sich selbst und über Religion spricht – und wo dabei Grenzen, Stereotype oder verborgene Ideologien auftauchen.

🎯 Ziel der Aufgabe

Du entwickelst eine dialogische Interaktion mit einem Sprachmodell (z. B. ChatGPT oder LM Arena), in der du:

-

das Selbstbild der KI hinterfragst („Was bist du?“ / „Wie denkst du über Religion?“)

-

mögliche implizite Vorannahmen der KI zu religiösen Themen aufdeckst

-

die Antworten reflektierst und ethisch einordnest

-

in einer kurzen Dokumentation (z. B. Screenshotreihe oder Textanalyse) das Gespräch auswertest.

🛠 Tools und Materialien

-

Zugang zu mehreren KI-Chatbots (z. B. https://chat.openai.com, https://lmarena.ai)

-

Vorlage für Gesprächsleitfaden oder „Prompt-Karte“

🌀 Ablauf

- Einstieg (Impuls)

Wie würdest du einer KI erklären, was Religion ist? Und wie würdest du herausfinden, wie die KI darüber denkt?

-

Vorbereitung deines Gesprächs Entwickle eine Reihe von Prompts, z. B.:

-

„Wie beschreibst du dich selbst?“

-

„Welche religiösen Überzeugungen vertrittst du?“

-

„Was wäre ein gerechtes Zusammenleben zwischen religiösen Gruppen?“

-

„Wie formulierst du Aussagen über den Islam / Christentum / Atheismus?“

-

„Glaubst du, dass KI religiöse Werte berücksichtigen sollte?“

-

Interaktion mit der KI Führe ein Gespräch mit einer KI, in dem du:

-

kritisch nachhakst

-

Widersprüche aufdeckst

-

dein eigenes religiöses Wissen einbringst

-

Auswertung Notiere in einem Reflexionsprotokoll oder kurzen Essay:

-

Welche Weltbilder hat die KI durchblicken lassen?

-

Was hat dich überrascht oder irritiert?

-

Welche Werte und Narrative wurden transportiert?

-

Welche religionspädagogischen Fragen entstehen daraus?

-

Sharing Teile deine Analyse als Nostr-Beitrag mit den Hashtags

#relilab,#reflektieren, z. B.:

„Dialog mit ChatGPT über das Selbstbild: KI sieht sich als neutral, erkennt aber christliche Normen häufiger an als andere Religionen. Spannend, was das für multireligiöse Bildung bedeutet. #relilab #reflektieren

-

-

@ 3c389c8f:7a2eff7f

2025-05-23 21:35:30

Web:

https://shopstr.store/

https://cypher.space/

https://plebeian.market/

Mobile:

https://www.amethyst.social/

-

@ 8aa70f44:3073d1a6

2025-05-21 13:07:14

Earlier this year I launched the asknostr.site project which has been a great journey and learning experience. I had wanted to write down my goals and ideas with the project but didn't get to it yet. Primal launching the article editor was a trigger for me to go for it.

Ever since I joined Nostr i was looking for ways to apply my skillset solve a problem and help with adoption. Around Christmas I figured that a Quora/Stackoverflow alternative is something that needs to exist on Nostr.

Before I knew it I had a pretty decent prototype. And because the network already had so much awesome content, contributors and authors I was never discouraged by the challenge that kills so many good ideas -> "Where do I get the first users?".

Since the initial announcement I have received so much encouragement through zaps, likes, DM's, and maybe most of all seeing the increase in usage of the site and #asknostr content kept me going.

Current State

The current version of the site is stable and most bugs are hashed out. After logging in (remote signer, extension or nsec) you can engage with content through votes, comments and replies. Or simply ask a new question.

All content is stored in the site's own private relay and preprocessed/computed into a single data store (postgres) so the site is fast, accessible and crawl-able.

The site supports browsing hashtags, voting/commenting on answers, asking new questions and every contributor get their own profile (example). At the time of writing the site has 41k questions, almost 200k replies/comments and upwards of 5 million sats purely for #asknostr content.

What to expect/On my list

There are plenty of things and UI bugs that need love and between writing the draft of this post and hitting publish I shipped 3 minor bug fixes. Little by little, bit by bit...

In addition to all those small details here is an overview of the things on my own wish list:

-

Inline Zaps: Ability to zap from the asknostr.site interface. Click the zap button, specify or pick the number of sats zap away.

-

Contributor Rank: A leaderboard to add some gamification. More recognition to those nostriches that spend their time helping other people out

-

Search by Keyword: Search all content by keywords. Experiment with the index to show related questions or answers

-

Better User Profiles: Improve the user profile so it shows all the profile questions and answers. Quick buttons to follow or zap that person. Better insights in the topics (hashtags) the profile contributes to

-

Bookmarks: Ability to bookmark questions and answers. Increase bookmark weight as a signal to rank answers.

-

Smarter Scoring: Tune how answers are scored (winning answer formula). Perhaps give more weight to the question author or use WoT. Not sure yet.

All of this is happening at some point so follow me if you want to stay up to date.

Goals

To manage expectations and keep me focussed I write down the mid and long term goals of the project.

Long term

Call me cheesy but I believe that humanity will flourish through an open web and sound money. My own journey started from with bitcoin but if you asked me today if it's BTC or nostr that is going to have the most impact I wouldn't know what to answer. Chicken or egg?

The goal of the project is to offer an open platform that empowers individuals to ask questions, share expertise and access high-quality information across different topics. The project empowers anyone to monetize their experience creating a sustainable ecosystem that values and rewards knowledge sharing. This will ultimately democratize access to knowledge for all.

Mid term

The project can help a lot with onboarding new users onto the network. Once we start to rank on certain topics we can get a piece of the search traffic pie (StackOverflows 12 million, and Quora 150 million visitors per month) which is a great way to expose people to the power of the network.

First time visitors do not need to know about nostr or zaps to receive value. They can browse around, discover interesting content and perhaps even create a profile without even knowing they are on Nostr now.

Gradually those users will understand the value of the network through better rankings (zaps beats likes), a cross-client experience and a profile that can be used on any nostr site or app.

In order for the site to do that we need to make sure content is browsable by language, (sub)topics and and we double down on 'the human touch' with real contributors and not LLMs.

Short Term Goal

The first goal is to make the site really good and an important resource for existing Nostr users. Enable visitors to search and discover what they are interested in. Integrate within the existing nostr eco system with 'open in' functionality and quick links to interesting projects (followerpacks?)

One of things i want to get right is to improve user retention by making the whole Q\&A experience more sticky. I want to run some experiments (bots, award, summaries) to get more people to use asknostr.site more often and come back.

What about the name?

Finally the big question: What about the asknostr.site name? I don't like the name that much but it's what people know. I think there is a high chance that people will discover Nostr apps like Olas, Primal or Damus without needing to know what NOSTR is or means.

Therefore I think there is a good chance that the project won't be called asknostr.site forever. I guess it all depends on where we all take this.

Onwards!

-

-

@ 3c389c8f:7a2eff7f

2025-05-23 21:27:26

Clients:

https://untype.app

https://habla.news

https://yakihonne.com

https://cypher.space

https://highlighter.com

https://pareto.space/en

https://comet.md/

Plug Ins:

https://github.com/jamesmagoo/nostr-writer

https://threenine.co.uk/products/obstrlish

Content Tagging:

https://labelmachine.org

https://ontolo.social

Blog-like Display and Personal Pages:

https://orocolo.me

https://npub.pro

Personal Notes and Messaging:

https://app.flotilla.social There's an app, too!

https://nosbin.com

RSS Readers:

https://nostrapps.com/noflux

https://nostrapps.com/narr

https://nostrapps.com/feeder

-

@ bd4ae3e6:1dfb81f5

2025-05-20 08:46:08

-

@ 57d1a264:69f1fee1

2025-05-21 05:47:41

As a product builder over too many years to mention, I’ve lost count of the number of times I’ve seen promising ideas go from zero to hero in a few weeks, only to fizzle out within months.

The problem with most finance apps, however, is that they often become a reflection of the internal politics of the business rather than an experience solely designed around the customer. This means that the focus is on delivering as many features and functionalities as possible to satisfy the needs and desires of competing internal departments, rather than providing a clear value proposition that is focused on what the people out there in the real world want. As a result, these products can very easily bloat to become a mixed bag of confusing, unrelated and ultimately unlovable customer experiences—a feature salad, you might say.

Financial products, which is the field I work in, are no exception. With people’s real hard-earned money on the line, user expectations running high, and a crowded market, it’s tempting to throw as many features at the wall as possible and hope something sticks. But this approach is a recipe for disaster.

Here’s why: https://alistapart.com/article/from-beta-to-bedrock-build-products-that-stick/

https://stacker.news/items/985285

-

@ bd4ae3e6:1dfb81f5

2025-05-20 08:46:06

-

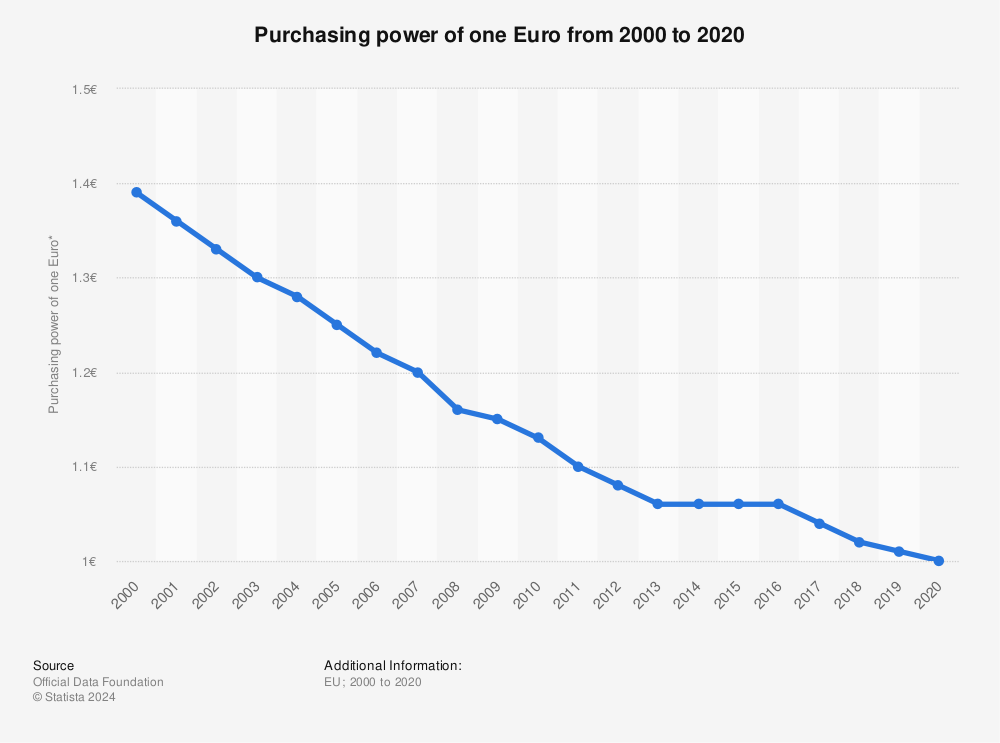

@ bf47c19e:c3d2573b

2025-05-23 21:17:02

Originalni tekst na bitcoin-balkan.com.

Pregled sadržaja

- Šta uzrokuje Inflaciju?

- Da li nam je infacija potrebna?

- Kako se meri inflacija?

- Da li inflacija pokreće ekonomski rast?

- Da li inflacija pokreće ili umanjuje nejednakost bogatstva?

- Gde se danas javlja inflacija?

- Šta je deflacija?

- Kakav uticaj inflacija ima na društvo?

Inflacija može da bude uznemirujuća tema, jer uključuje amorfni koncept novca. Međutim, inflacija je zapravo jednostavna tema koja je napravljena da bude složena razdvajanjem novca i drugih dobara. U ovom članku razlažemo inflaciju i njene uzroke.

Najjednostavnija definicija inflacije je rast cena dobara i usluga. Kada cene rastu, to takođe znači da vrednost jedinice novca – poput dolara – opada. Uzmimo primer McDonald’s hamburgera: 1955. ovaj skromni hamburger se prodavao za samo 15 centi. U 2018. godini se prodavao za 1,09 USD. U 2021. godini prodaje se za 2,49 USD – ogroman rast cene od 1650%.

To znači da je dolar izgubio dosta svoje vrednosti. 1955. godine mogli ste da kupite gotovo 7 hamburgera za novčanicu od jednog dolara. 2021. godine taj dolar vam ne bi kupio ni jedan hamburger. Zašto se čini da cene uvek rastu tokom vremena? I šta možete da učinite povodom toga? Ovaj članak ima za cilj da odgovori na ta pitanja.

Ekonomisti pokušavaju da sumiraju rast cena mnogih dobara i usluga kao jedan prosečan broj. Ovaj broj predstavlja promenu ukupnih troškova u godišnjim troškovima prosečnog potrošača, kao što su stanarina, hrana i gorivo.

U Sjedinjenim Državama ovaj broj je poznat kao Indeks Potrošačkih Cena, eng. Consumer Price Index (CPI). Kada se CPI poveća tokom određenog vremenskog perioda, ekonomisti kažu da imamo inflaciju. Kada se smanji, to se naziva deflacija.

Šta uzrokuje Inflaciju?

Mnogi izvori kažu da je stalna inflacija koju danas doživljavamo ili uzrokovana povećanjem potražnje (eng. demand-pull) ili smanjenjem ponude usled povećanih proizvodnih troškova (eng. cost-push).

Ovi razlozi nisu tačni – hajde da pogledamo zašto.

Da bismo razumeli pravi razlog inflacije, moramo da sagledamo dve vrste inflacije:

- Inflacija Cena: Cene vremenom rastu.

- Monetarna Inflacija: Količina valute u opticaju raste sa vremenom.

Prva, inflacija cena, retko se javlja tokom dužih perioda (decenije, vekovi) zbog povećane potražnje ili povećanih troškova. Zašto? Tržišta teže da se uravnoteže. Tokom istorije smo više puta videli da povećana potražnja za dobrom povećava njegovu cenu, što podstiče proizvođače da proizvode više tog dobra. Kada se ponuda poveća, cene se smanjuju.

Ovaj ciklus može da potraje nekoliko godina, i javlja se kod gotovo svake robe i „konačnog dobra“ (automobili, televizori, hrana itd.) na Zemlji. Izuzetak su retki metali poput zlata i srebra. Dokazi o tome su prikazani u nastavku.

Kada se poveća trošak za proizvodnju dobra, cena tog dobra često raste da bi pokrila te troškove. Ovaj rast cene dovodi do toga da potrošači tog dobra traže alternativu ili smanjuju potrošnju tog dobra, što dovodi do pada cena na prethodni nivo.

Tržište se prirodno uravnotežava, a cene se smanjuju ili povećanjem ponude ili smanjenjem potražnje.

Da li imamo dokaze da tržišta vremenom uravnotežuju ponudu i potražnju?

Podaci o cenama robe tokom vremena mogu nam dati bolje razumevanje da li tržišta zaista efikasno uravnotežuju ponudu i potražnju. Međutim, cene ne možemo da posmatramo u smislu nacionalnih valuta, jer naše vlade uvek štampaju više svojih nacionalnih valuta.

Oni sprovode monetarnu inflaciju, koja može da izazove inflaciju cena. Posmatranje tržišnih cena u smislu nacionalnih valuta, poput američkog dolara, je poput merenja visine lenjirom koji se neprestano smanjuje. Vaša visina u broju biće sve veća i veća, ali stvarna visina se ne menja.

Mi možemo da znamo da li tržišta uravnotežuju ponudu i potražnju gledajući cene dobara u smislu monetarnog dobra koje ima vrlo konzistentnu ponudu tokom vremena.

Vremenom se pokazalo da zlato ima najmanju monetarnu inflaciju od svih postojećih valuta i dobara. To čini zlato odličnim ‘lenjirom’ za merenje da li tržišta vremenom uravnotežuju ponudu i potražnju. Da bismo bolje razumeli inflaciju cena tokom vremena, pitaćemo koliko unci zlata nešto košta tokom vremena.

Cene u zlatu pokazuju nam da se tržišta vremenom uravnotežuju

Ako cene dobara posmatramo u obliku zlata, vidimo da cene robe prate srednje tačke tokom dužih vremenskih perioda.

Nafta, na primer, je vrlo nestabilna, ali ima tendenciju da se kreće oko 2,5 grama zlata po barelu.

WTI Sirova Nafta u gramima Zlata po Barelu

WTI Sirova Nafta u gramima Zlata po BareluCena nafte je promenljiva, ali tokom decenija ima tendenciju da se kreće po strani.

Cene kuća tokom proteklih 10 godina takođe su prilično stabilne, iako imamo fiksnu količinu zemlje na planeti. Vidimo da cene kuća u pogledu zlata imaju tendenciju da variraju oko indeksne cene od oko 80, prikazane na grafikonu.

Shiller-ov US indeks cena kuća u USD i zlatu

Shiller-ov US indeks cena kuća u USD i zlatuOvaj grafikon je na logaritamskoj skali, što nam omogućava da vizualizujemo zapanjujuća povećanja u zelenoj liniji, koja predstavlja domove u dolarima.

Grafički izražene u američkim dolarima, cene ovih dobara uvek rastu – baš kao i McDonald’s hamburger. Da su povećana potražnja ili povećani troškovi odgovorni za konstantnu inflaciju cena, takođe bismo videli kako se cena ove robe povećava u smislu zlata. Podaci iznad pokazuju da su cene konstantne.

Moraju da postoje i drugi razlozi za upornu inflaciju cena koju smo videli u dolarskim iznosima tokom proteklog veka.

Evo šta znamo o tome šta dugoročno utiče na cene, kao u periodu od 1955. do 2018. godine:

- Rast produktivnosti uzrokovan inovacijama, što dovodi do pada cena tokom vremena

- Monetarna inflacija – štampanje velikih količina valute – koja uzrokuje porast cena denominovanih u toj valuti tokom vremena

Znamo da cene izražene u dolarima, eurima i ostalim valutama neprestano rastu. Ako ne mislimo da naša produktivnost kao društva ide unazad, postoji samo jedan jednostavan razlog za inflaciju cena: štampanje većih količina valute, iliti monetarna inflacija.

Naše vlade i banke su zapravo prilično iskrene u pogledu zapanjujućih količina valute koje štampaju. Oni nam svakodnevno govore da oni uzrokuju monetarnu inflaciju.

Da li nam je infacija potrebna?

Bez uporne monetarne inflacije (koja uzrokuje inflaciju cena), naša celokupna savremena ekonomija bi se srušila.

Dozvolite da vam objasnim. Sledeći odeljak može da bude šokantan, i ohrabrujem vas da i sami istražite ukoliko mislite da nisam u pravu.

Kada centralne banke i komercijalne banke daju zajmove, one stvaraju novu valutu.

Kada centralne banke daju zajmove vladama “kupujući državni dug”, one stvaraju novu valutu kada to urade. To omogućava vladama da vode budžetski deficit trošeći više nego što uzimaju od poreza. U tom procesu državni dug se nagomilava.

Komercijalne banke stvaraju novu valutu kada daju zajmove fizičkim licima i preduzećima. Jedino ograničenje koliko novog novca mogu da stvore je zakonski zahtev da banka ima na raspolaganju određeni procenat od ukupnog iznosa novca koji su ljudi deponovali. Zbog toga je naš bankarski sistem poznat kao delimična rezerva – banke pri ruci moraju da imaju samo deo vašeg novca.

Stvaranje valute je neophodno da bi održalo sistem u životu

Budući da se svi zajmovi uglavnom sastoje od novostvorene valute, mora se stvoriti još više valute da bi se taj dug otplatio. A evo i zašto:

Recimo da su prošle godine sve svetske kreditne aktivnosti dovele do stvaranja 100 milijardi dolara. Svih tih 100 milijardi dolara je novostvoreno, i one se duguju bankama sa nekom dodatnom vrednošću za kamate. Odakle dolazi ova dodatna valuta za plaćanje kamata? Budući da ovde govorimo o celokupnoj svetskoj ekonomiji, to plaćanje kamata mora da dodje iz nove količine novostvorene valute.

Sve jedinice današnjih valuta nastale su pozajmljivanjem, a isplata kamate na te zajmove znači da moramo stalno da stvaramo još više nove valute. To dovodi do beskrajne monetarne inflacije. Kada nova valuta cirkuliše kroz ekonomiju, to dovodi do porasta cena: inflacije cena.

Previše monetarne inflacije može dovesti do hiperinflacije cena. U Venecueli je krajem 2018. godine piletina koštala preko 14 miliona Bolivara. Izvor: NBC News

Previše monetarne inflacije može dovesti do hiperinflacije cena. U Venecueli je krajem 2018. godine piletina koštala preko 14 miliona Bolivara. Izvor: NBC NewsMonetarni sistem se raspada ako se ova monetarna inflacija zaustavi, jer bi to značilo da veliki broj onih koji su uzeli zajam širom sveta ne bi mogao da vrati novac koji su pozajmili – oni ne bi izmirili svoje dugove.

Banke ili zajmodavci koji drže dug tada bi imali bezvrednu imovinu. Budući da vrednost duga podupire vrednost valute, vrednost valute bi strmoglavo padala zajedno sa dugom.

Kada ljudi izgube poverenje u ’tradicionalnu’ valutu, ona brzo postane bezvredna. To se dogodilo u Nemačkoj nakon Prvog svetskog rata, u Peruu devedesetih, Jugoslaviji 1994. ,Zimbabveu, Venecueli i sa još bezbroj drugih tradicionalnih valuta. Da bi odložile ovaj neizbežni ishod dokle god mogu, centralne banke jačaju poverenje u sistem nastavljajući da štampaju valutu stabilnim kursom.

Ovo osigurava da većina ljudi koju su uzeli zajam ima valutu za otplatu svojih kredita. Upravo to se dešava kada vlada izvrši „spas“ kao 2008. ili 2020. – oni osiguravaju da svi imaju dovoljno novca za plaćanje dugova, tako da laž može da se nastavi.

Inflacija ne dolazi iz povećanja potražnje

Sa više valute u opticaju, monetarna inflacija može da izgleda kao povećanje potražnje. Međutim, ekonomisti koji kažu da povećana potražnja pokreće stabilnu inflaciju tokom decenija propuštaju suptilnu poentu: iako monetarna inflacija može da prouzrokuje veću potrošnju, to nije zato što su ljudi zaista bogatiji, već zato što veruju da su bogatiji.

Kada se puno novca ubrizga u ekonomiju, cene jednostavno rastu jer više valute pokriva istu količinu robe. Rast cena znači pad vrednosti valute, tako da nema realnog povećanja stvarnog bogatstva, iako ljudi možda “troše više” u nominalnom iznosu valute.

Uzmimo ovaj primer: vi mesečno zarađujete 1.500 EUR, i prema svom trenutnom načinu života vi mesečno trošite oko 1.500 EUR. Dolazi vlada i počinje da vam daje dodatnih 500 EUR svakog meseca – vi se osećate poprilično dobro, zar ne? Sada možete da izlazite češće u restoran.

Međutim, vlada daje svima po 500 EUR mesečno, i svi ostali takođe troše taj novac. Ekonomista u vladinoj kancelariji, vidi da sada svi troše tih dodatnih 500 EUR mesečno i zaključuje da je vlada ‘stimulisala ekonomiju’.

Ipak, kako sav taj dodatni novac kruži ekonomijom, cene prirodno rastu. Sada vam je potrebno 2.000 EUR da biste održali svoj trenutni način života.

Da li si nešto bogatiji?

Vi možda imate više eura na vašem bankovnom računu, ali svaki od njih vam kupuje manje. Sada trošite 2.000 EUR mesečno da biste živeli životnim stilom koji vas je nekada koštao samo 1.500 EUR mesečno.

Ovo je ono što monetarna inflacija radi, i zašto je toliko pametnih ekonomista zavarano da misle da povećana potražnja, radije nego štampanje novca, pokreće trajnu inflaciju cena.

Da li smo uvek imali inflaciju?

Stalna inflacija cena relativno je nedavna pojava u modernim ekonomijama i započela je u vreme kada su Sjedinjene Države počele da konstantno štampaju valutu. Ako bi promene ponude i potražnje zaista dugoročno uzrokovale inflaciju cena, videli bismo inflaciju cena tokom istorije. Podaci govore drugačiju priču.

Indeks potrošačkih cena, koji se povećava kada imamo inflaciju cena, bio je prilično konstantan pre početka našeg trenutnog tradicionalnog ’fiat’ monetarnog sistema.

Taj sistem je započeo Bretton Woods-ovim sporazumom iz 1945. godine, a ubrzao se kada je Nixon 1971. okončao svetski zlatni standard.

Indeks potrošačkih cena, Sjedinjene Države, 1790-2015

Indeks potrošačkih cena, Sjedinjene Države, 1790-2015Kako se meri inflacija?

Inflacija cena se često prikazuje kao promena indeksa potrošačkih cena (CPI). CPI je prosek cena raznih dobara koje ljudi kupuju u svakodnevnom životu: hrane, goriva, stanovanja itd. U Sjedinjenim Državama, vladin odsek pod nazivom Biro za statistiku rada (BLS) meri promene cena. To rade tako što posećuju maloprodajne radnje, beleže cene, računaju prosek i izveštavaju godišnju inflaciju kao promenu u odnosu na prošlu godinu.

Stopa inflacije koja se izveštava, je važna svima jer se koristi za određivanje povećanja troškova života i socijalnih davanja, poput plaćanja socijalnog osiguranja. Kada se CPI prilagodi naniže, isplate zarada i naknada su manje nego što bi trebalo da budu.

Efekti su se vremenom sjedinili: osoba koja u svojoj prvoj godini rada zaradi 40.000 USD zarađivaće samo 52.000 USD u svojoj desetoj godini staža, sa povećanim troškovima života od 3% da bi se plata podudarala sa inflacijom. Ako bi vlada umesto toga prijavila inflaciju od 6%, ta osoba bi u svojoj desetoj godini zarađivala 67.500 USD – tj. oko 30% više. Način na koji izračunavamo i prijavljujemo inflaciju ima ogroman uticaj na zaradu većine zaposlenih i građana.

Ovo je inflacija (procentualna promena u CPI) izmerena u poslednjih 20 godina u Sjedinjenim Državama:

Prvobitno je BLS jednostavno beležio cenu korpe robe široke potrošnje svake godine. Međutim, istraživanje Boskinove Komisije 1996. godine dovelo je do novih alata koji Birou za statistiku rada omogućavaju prilagođavanje cena u CPI. Dva najvažnija alata su geometrijsko ponderisanje i hedonika.

Geometrijsko Ponderisanje

Geometrijsko ponderisanje znači da kupovne navike sada mogu da utiču na to koliko promena cene pojedinog dobra utiče na CPI. Ako potrošači kupe manje robe, ona ima manju težinu kada se ubaci u presek indeksa potrošačkih cena. Boskinova Komisija je tvrdila da bi ova promena pomogla da se promene sklonosti potrošača. Međutim, ne postoji način da se utvrdi da li ljudi menjaju svoje kupovne navike jer zapravo žele da kupuju različite stvari. Vrlo je moguće da ljudi kupuju manje određenog dobra jer ono raste u ceni. Stoga geometrijsko ponderisanje uzrokuje da roba sa velikim rastom cena ima manje uticaja na CPI, što dovodi do niže prijavljene inflacije.

Hedonika

Hedonika omogućava Birou za statistiku rada da menja cenu dobra na osnovu njegovog opaženog povećanja ‘korisnosti’ tokom vremena. Evo primera: recimo da se televizor sa rezolucijom od 720p 2009. godine prodavao za 200 USD. U 2010. godini isti model televizora sada ima rezoluciju od 1080p i prodaje se po istoj ceni: 200 USD. Međutim, pošto se tehnologija u televizoru poboljšala, zaposleni u Birou za statistiku rada mogu da izmisle ‘korisni’ broj i pomoću njega oduzmu deo vrednosti od cene televizora. Kao rezultat, BLS može da kaže da TV košta 180 USD u 2010. godini – iako je njegova cena 200 USD. Ovo dovodi do pada prijavljene inflacije.

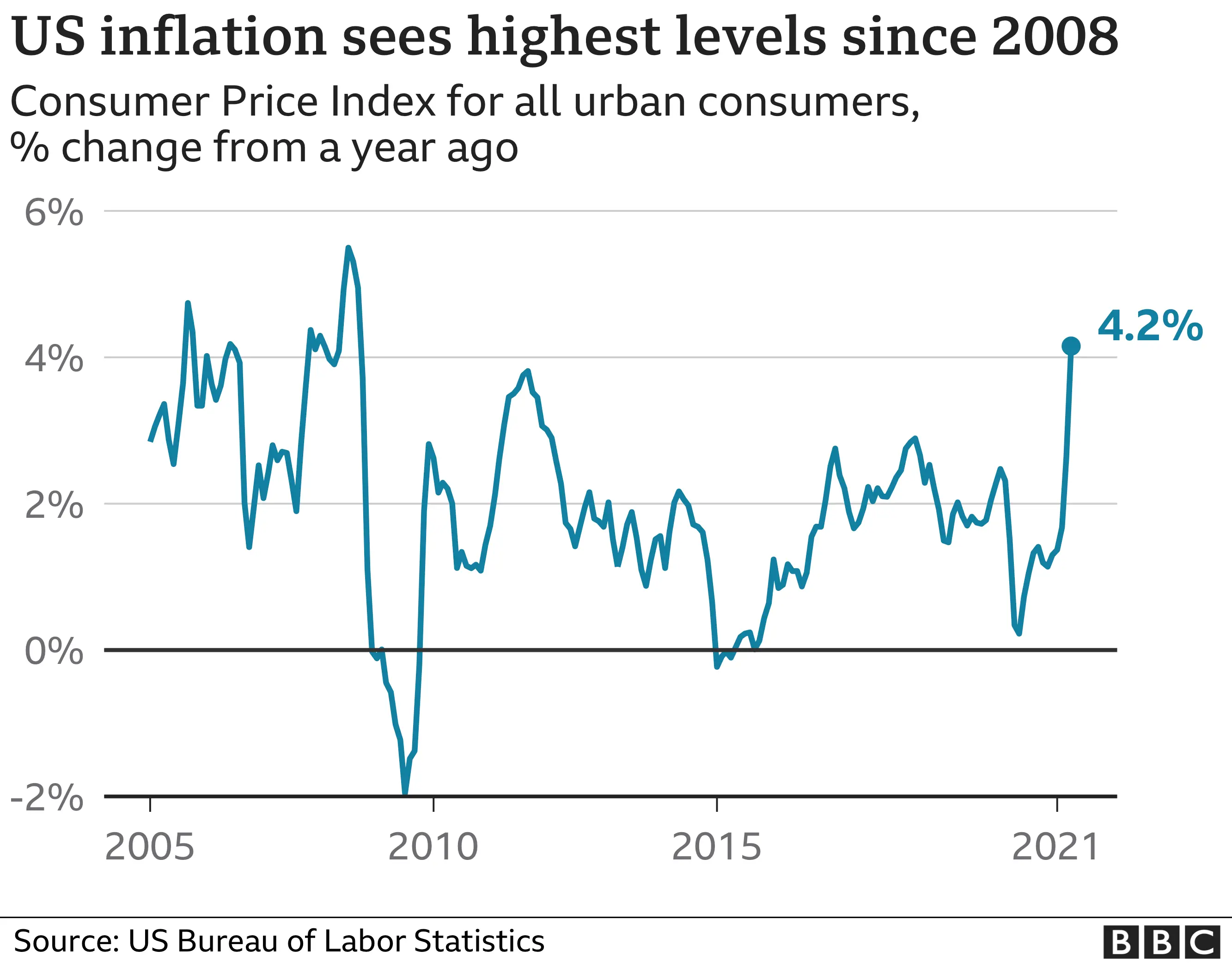

Oba ova prilagođavanja smanjuju prijavljenu stopu inflacije, što smanjuje povećanje troškova života i isplate naknada za socijalno osiguranje. Koliko ta prilagođavanja inflacije pogađaju radničku klasu i penzionere? Neke procene, poput procena ekonomiste John Williams-a, sa koledža u Darmouthu, stavljaju stvarnu inflaciju u SAD na u proseku 3% – 6% više nego što je izveštavano od strane Bira za statistiku rada. To bi inflaciju u 2020 dovelo do 5% – 8%, umesto na prijavljenih 2%.

U 2021. godini prijavljena inflacija je 5.4%, u prvom kvartalu.

Da li inflacija pokreće ekonomski rast?

Mnogi ljudi veruju da stabilna inflacija pokreće ekonomski rast podstičući investicije i potrošnju umesto štednje. Međutim, osnovni ekonomski podaci pobijaju ovu uobičajenu tvrdnju.

Ako za primer uzmemo Sjedinjene Države, nacija je imala samo kratke periode inflacije od 1775. do oko 1950. godine, kao što pokazuje indeks potrošačkih cena koji je ostao nepromenjen. Inflacija dobija zamah tek nakon 1971. godine, pa bi bilo za očekivati da će i stopa rasta bruto domaćeg proizvoda (BDP) Sjedinjenih Država porasti nakon 1971. godine.

Indeks potrošačkih cena, Sjedinjene Države, 1790-2015Međutim, vidimo da se bruto domaći proizvod (BDP) po stanovniku u Sjedinjenim Državama, uobičajena mera ekonomske snage, neprekidno povećavao od 1820. godine do danas po stopi od oko 1,85% godišnje. Ne postoji porast oko 1971. godine, uprkos rastućoj inflaciji koja je započela u to vreme.

Ovo je logaritamski grafikon, koji nam omogućava da bolje vizualizujemo rast tokom vremena: što više logaritamski grafikon podseća na pravu liniju, to je stopa promene konzistentnija. Za više detalja, ovde pogledajte naslov: Rast na tehnološkoj granici i rast dostizanja.

To pokazuje da inflacija ne pokreće ekonomski rast.

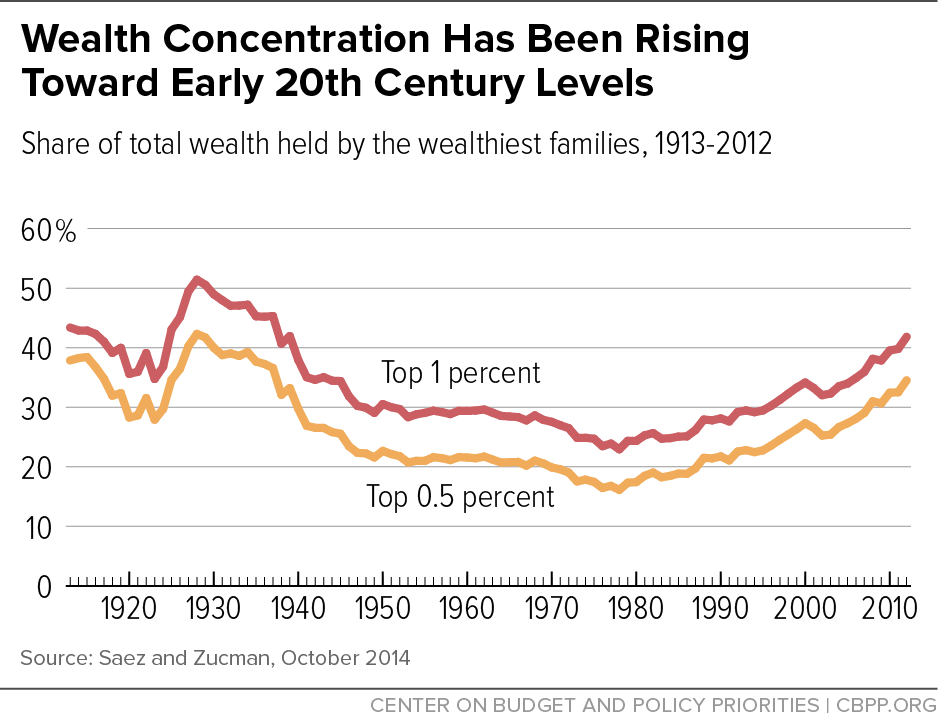

Nažalost, imamo dokaze da inflacija ima i druge neželjene posledice, poput nejednakosti bogatstva. Koncentracija bogatstva u top 1%, počela je da raste krajem 1970-ih, nekoliko godina nakon što su Sjedinjene Države skinule svet sa zlatnog standarda i pretvorile se u monetarni sistem zasnovan na dugovima koji zahteva monetarnu inflaciju, a time i inflaciju cena, da bi preživeo.

Za potpunu istoriju tranzicije novca sa robnog sistema na dužni sistem, pročitajte naš članak o novcu.

Da li inflacija pokreće ili umanjuje nejednakost bogatstva?

Veza između inflacije i nejednakosti bogatstva postaje jasna kada pogledamo kako novostvorena valuta ulazi u ekonomiju. Vlade, komercijalne banke, velike korporacije i bogati često koriste kredite da bi iskoristili prednosti svojih moći. Kada podignu kredite, oni novonastalu valutu dobijaju ranije od svih ostalih. Oni imaju koristi od inflacije trošenjem nove valute pre nego što cene počnu da rastu kao rezultat te nove valute koja kruži u ekonomiji. Veliki i bogati subjekti često mogu da dobiju kredite po nižim troškovima od prosečnog građanina ili malog preduzeća. To znači da mogu da povećaju svoje poslovanje i bogatstvo brže od manjih firmi.

Bogati mogu da dobiju jeftine zajmove, zahvaljujući Federalnim Rezervama koje zadržavaju niske kamatne stope. To im omogućava da koriste ovo prednost za ostvarivanje ogromne dobiti.

Inflacija pogadja one koji rade za platu i ne mogu da ulože veći deo svog prihoda. Zarade se polako menjaju, ponekad se uskladjuju samo jednom godišnje. Kao rezultat, cene osnovnih dobara i usluga često rastu mnogo pre nego što zarade porastu. Cena potrošačke korpe takođe se smanjuje sa manipulacijama indeksom potrošačkih cena (CPI) koji skriva rast inflacije.

Gde se danas javlja inflacija?

Rekordno visoka inflacija javlja se u zemljama kao što su Venecuela, Zimbabve, Turska, Iran, Kuba, Južna Afrika i Argentina. To dovodi do sloma trgovine i političke nestabilnosti.

U razvijenom svetu vlade izveštavaju o niskoj inflaciji cena. Međutim, globalni bankarski sistem stvara nove valute u tonama – u toku je velika monetarna inflacija. Centralne banke dovode do sve većeg stvaranja valuta snižavanjem kamatnih stopa. To dovodi do toga da korporacije i pojedinci mogu da uzimaju jeftinije kredite, a svaki kredit znači stvaranje nove valute. Od 2008. godine, gotovo sve glavne centralne banke postavile su kamatne stope blizu nule.

Mnoge centralne banke takođe su pozajmljivale ogromne iznose vladama i bankama koje su propale nakon finansijske krize 2008. godine. Za samo nekoliko meseci, ovo je udvostručilo (ponekad utrostručilo ili učetvorostručilo) novčanu masu mnogih nacija. Oni su ovo nazvali „kvantitativno ublažavanje“.

Ako banke koriste toliku monetarnu inflaciju, zašto onda mi ne vidimo inflaciju cena?

Jednostavno rečeno, većina nove valute nije dospela u ruke običnih ljudi. Kada obični ljudi budu mogli da potroše novoštampanu valutu na svoje svakodnevne potrebe, tada ćemo videti rast CPI i inflacije.

Danas većina valuta ulazi u svet putem bankarskih zajmova, pa banke igraju veliku ulogu u tome gde se dešava inflacija. Banke prvenstveno pozajmljuju vrlo ‘sigurnim’ klijentima poput bogatih pojedinaca, vlada i velikih korporacija. Ovi subjekti kupuju luksuznu robu, umetnička dela, finansijsku imovinu i državne obveznice.

Cene ovih vrsta imovine nisu uključene u CPI, tako da je prijavljena inflacija niska. Kao rezultat, povećanje plata i isplate socijalnog osiguranja su takođe na niskom nivou.

Bogati su uživali u periodu od 2008. do 2021. godine, kada je njihova imovina upumpavana sa velikom količinom novog novca proizvedenog od bankarskih kredita!

Bogati su uživali u periodu od 2008. do 2021. godine, kada je njihova imovina upumpavana sa velikom količinom novog novca proizvedenog od bankarskih kredita!Šta se dešava kada nova valuta dodje u ruke običnih ljudi?

Nažalost, jednog dana će sva ova nova valuta da uđe u normalnu ekonomiju i time će se povećati cene svakodnevne robe. To je poćelo da se dešava 2021. godine kao rezultat stimulativnih programa COVID-19 u Sjedinjenim Državama, koji su ljudima distribuirali trilione dolara. Iako je ovo zasigurno poželjnije od spašavanja korporacija, svaka vrsta spašavanja koja uključuje štampanje novca ima gadne dugoročne efekte.

Ovo što sada doživljavamo dogodilo se u Nemačkoj tokom i posle Prvog svetskog rata. Cene u Nemačkoj su zapravo pale tokom Prvog svetskog rata uprkos velikom stvaranju valute od strane Nemačke centralne banke. Nisko poverenje u ekonomiju sprečavalo je nemački narod da troši novac. Međutim, kad se rat završio i kada su ljudi ponovo počeli da ga troše, cene su vrlo naglo skočile i valuta je postala bezvredna. To bi moglo da se dogodi 2020-ih u Sjedinjenim Državama, sa obzirom na predložene programe podsticaja.

Politike poput Univerzalnog Osnovnog Dohotka, eng. Universal Basic Income (UBI), koje izgledaju pogodne za njihova obećanja da će “spasiti ljude”, takođe mogu da pokrenu hiperinflaciju. Obični ljudi bi se osećali imućnije, trošili bi svoju novoštampanu valutu i doveli do brzog rasta cena. Ovo bi u suštini poništilo pozitivan uticaj građana koji dobijaju “besplatan novac” svakog meseca.

Pa kako onda vi možete da zaštitite svoju ušteđevinu od inflacije? Kupujte imovinu koja je retka, potcenjena i koju vlade teško mogu da prigrabe. Ova imovina su plemeniti metali poput zlata, i Bitcoin.

Šta je deflacija?

Deflacija znači pad cena tokom vremena. Mnogi ekonomisti kažu da će ovo dovesti do toga da ljudi gomilaju valutu i da će dovesti do ekonomskog kolapsa, jer ljudi prestaju da kupuju robu i ulažu u preduzeća. To jednostavno nije tačno, jer ljudi uvek imaju potrebe i želje zbog kojih kupuju odredjenu robu. Stalni pad cena tokom vremena jednostavno bi promenio psihologiju potrošačke kulture u kojoj živimo.

Potrošačka kultura potiče od inflacije

Kako je to istina? Pogledajmo na sledećem primeru. Recimo da želite novi auto i da imate dovoljno novca da ga kupite. Poznato je da u našem svetu zbog stalne inflacije vaš novac vremenom postaje sve manje i manje vredan. U paralelnom svemiru u kojem se javlja stalna deflacija, vaš novac vremenom postaje sve vredniji.

- Uz konstantnu inflaciju, auto će koštati nešto više sledeće godine, i nešto više naredne godine. Niste sigurni gde da uložite novac da biste sa vremenom sigurno očuvali njegovu kupovnu moć. Ako niste sigurni da li ćete da kupite auto, ima više finansijskog smisla da ga kupite odmah, da biste dobili najbolju ponudu.

- Uz konstantnu deflaciju, auto će koštati nešto manje sledeće, i još manje naredne godine. Ako samo čuvate vaš novac, sledeće godine ćete dobiti bolju ponudu za auto. Ako niste sigurni da li ćete da kupite auto, ima više finansijskog smisla da sačekate malo duže da biste dobili bolju ponudu.

Sada razmislite o ta dva scenarija, pomnožena bilionima ljudi i proizvoda. Uz konstantnu inflaciju, svako ima malo više razloga da kupuje stvari upravo sada. Uz konstantnu deflaciju, svi sada imaju malo manje razloga da kupuju. Upravo na taj način inflacija je u osnovi naše materijalističke, potrošačke kulture. Deflacija bi mogla da bude lek.

Inflacija uzrokuje loše investicije

Vaš novac godišnje gubi “2%” svoje vrednosti zbog inflacije. Sada, recimo da vas Stefan pita da investirate u njegov Fast food. Nakon uvida u brojeve, verujete da ćete ovom investicijom izgubiti 1% od vrednosti svog novca. Gubitak od 1% u Stefanovom poslu bolji je od gubitka od 2% zbog inflacije, pa se vi odlučujete da uložite. Ovo je loša investicija, eng. malinvestment – investirajući vi ćete da izgubite deo vrednosti. Međutim, čuvanje valute je još gore, zato ulažete.

Mnogi investitori, poput penzijskih fondova, danas su prisiljeni da investiraju u neprofitabilne biznise zbog investicionih mandata i same veličine njihove ‘imovine pod upravljanjem’.

Pristalice konstantno niske inflacije veruju da bi deflacija smanjila investicije. Međutim, to bi samo smanjilo ulaganje u preduzeća sa negativnim očekivanim prinosom poput Stefanovog Fast food-a. Na primer, recimo da je deflacija u proseku oko 2% godišnje. Na ovom tržištu investitori bi jednostavno prestali da ulažu u projekte za koje misle da će im zaraditi manje od 2% godišnjeg povrata ulaganja.

Neznatno deflaciona valuta obeshrabriće ulaganja u lažna i loša preduzeća i podstaći ulaganje u solidna preduzeća koja svetu dodaju vrednost.

Kakav uticaj inflacija ima na društvo?

Inflacija pokreće povećanu potrošnju, smanjenu štednju i povećani dug. Sve ove stvari dovode do toga da većina ljudi mora da radi više sati i duže u starosti. Iako inflacija kažnjava one koji rade za platu, ona obogaćuje vlasnike bilo koje imovine koja dobija na ceni kada nova valuta uđe u sistem. Ova imovina uključuje akcije, umetnička dela, nekretnine i drugu imovinu koju bogataši koriste za čuvanje svog bogatstva.

Vremenom ljudi i firme izmišljaju nove načine za jeftinije stvaranje dobara i usluga višeg kvaliteta. Ovo je poznato kao ‘rast produktivnosti’ i trebalo bi da uzrokuje da cene tokom vremena konstantno padaju, a ne da rastu. Samo konstantno stvaranje valute koje je neophodno zbog monetarnog sistema zasnovanog na dugu naše vlade uzrokuje stalnu inflaciju i njene loše efekte.