-

@ c9badfea:610f861a

2025-05-20 19:49:20

@ c9badfea:610f861a

2025-05-20 19:49:20- Install Sky Map (it's free and open source)

- Launch the app and tap Accept, then tap OK

- When asked to access the device's location, tap While Using The App

- Tap somewhere on the screen to activate the menu, then tap ⁝ and select Settings

- Disable Send Usage Statistics

- Return to the main screen and enjoy stargazing!

ℹ️ Use the 🔍 icon in the upper toolbar to search for a specific celestial body, or tap the 👁️ icon to activate night mode

-

@ 04c915da:3dfbecc9

2025-05-20 15:53:48

This piece is the first in a series that will focus on things I think are a priority if your focus is similar to mine: building a strong family and safeguarding their future.

Choosing the ideal place to raise a family is one of the most significant decisions you will ever make. For simplicity sake I will break down my thought process into key factors: strong property rights, the ability to grow your own food, access to fresh water, the freedom to own and train with guns, and a dependable community.

A Jurisdiction with Strong Property Rights

Strong property rights are essential and allow you to build on a solid foundation that is less likely to break underneath you. Regions with a history of limited government and clear legal protections for landowners are ideal. Personally I think the US is the single best option globally, but within the US there is a wide difference between which state you choose. Choose carefully and thoughtfully, think long term. Obviously if you are not American this is not a realistic option for you, there are other solid options available especially if your family has mobility. I understand many do not have this capability to easily move, consider that your first priority, making movement and jurisdiction choice possible in the first place.

Abundant Access to Fresh Water

Water is life. I cannot overstate the importance of living somewhere with reliable, clean, and abundant freshwater. Some regions face water scarcity or heavy regulations on usage, so prioritizing a place where water is plentiful and your rights to it are protected is critical. Ideally you should have well access so you are not tied to municipal water supplies. In times of crisis or chaos well water cannot be easily shutoff or disrupted. If you live in an area that is drought prone, you are one drought away from societal chaos. Not enough people appreciate this simple fact.

Grow Your Own Food

A location with fertile soil, a favorable climate, and enough space for a small homestead or at the very least a garden is key. In stable times, a small homestead provides good food and important education for your family. In times of chaos your family being able to grow and raise healthy food provides a level of self sufficiency that many others will lack. Look for areas with minimal restrictions, good weather, and a culture that supports local farming.

Guns

The ability to defend your family is fundamental. A location where you can legally and easily own guns is a must. Look for places with a strong gun culture and a political history of protecting those rights. Owning one or two guns is not enough and without proper training they will be a liability rather than a benefit. Get comfortable and proficient. Never stop improving your skills. If the time comes that you must use a gun to defend your family, the skills must be instinct. Practice. Practice. Practice.

A Strong Community You Can Depend On

No one thrives alone. A ride or die community that rallies together in tough times is invaluable. Seek out a place where people know their neighbors, share similar values, and are quick to lend a hand. Lead by example and become a good neighbor, people will naturally respond in kind. Small towns are ideal, if possible, but living outside of a major city can be a solid balance in terms of work opportunities and family security.

Let me know if you found this helpful. My plan is to break down how I think about these five key subjects in future posts.

-

@ bf47c19e:c3d2573b

2025-05-22 21:07:02

Originalni tekst na bitcoin-balkan.com.

Pregled sadržaja

- Šta je Bitcoin?

- Šta Bitcoin može da učini za vas?

- Zašto ljudi kupuju Bitcoin?

- Da li je vaš novac siguran u dolarima, kućama, akcijama ili zlatu?

- Šta je bolje za štednju od dolara, kuća i akcija?

- Po čemu se Bitcoin razlikuje od ostalih valuta?

- kako Bitcoin spašava svet?

- Kako mogu da saznam više o Bitcoin-u?

Bitcoin čini da štednja novca bude kul – i praktična – ponovo. Ovaj članak objašnjava kako i zašto.

Šta je Bitcoin?

Bitcoin se naziva digitalno zlato, mašina za istinu, blockchain, peer to peer mreža čvorova, energetski ponor i još mnogo toga. Bitcoin je, u stvari, sve ovo. Međutim, ova objašnjenja su često toliko tehnička i suvoparna, da bi većina ljudi radije gledala kako trava raste. Što je najvažnije, ova objašnjenja ne pokazuju kako Bitcoin ima bilo kakve koristi za vas.

iPod nije postao kulturološka senzacija jer ga je Apple nazvao „prenosnim digitalnim medijskim uređajem“. Postao je senzacija jer su ga zvali “1,000 pesama u vašem džepu.”

Ne zanima vas šta je Bitcoin. Vas zanima šta on može da učini za vas.

Baš kao i Internet, vaš auto, vaš telefon, kao i mnogi drugi uređaji i sistemi koje svakodnevno koristite, vi ne treba da znate šta je Bitcoin ili kako to funkcioniše da biste razumeli šta on može da učini za vas.

Šta Bitcoin može da učini za vas?

Bitcoin može da sačuva vaš teško zarađeni novac.

Bitcoin je stekao veliku pažnju u 2017. i 2018. godini zbog svoje spekulativne upotrebe. Mnogi ljudi su ga kupili nadajući se da će se obogatiti. Cena je naglo porasla, a zatim se srušila. Ovo nije bio prvi put da je Bitcoin uradio to. Međutim, niko nikada nije izgubio novac držeći bitcoin duže od 3,5 godine – ćak i ako je kupio na apsolutnim vrhovima.

Zašto Bitcoin konstantno raste? Ljudi počinju da shvataju koliko je Bitcoin moćan, kao način uštede novca u svetu u kojem je ’novac’ poput dolara, eura i drugih nacionalnih valuta dizajniran da gubi vrednost.

Ovo čini Bitcoin odličnom opcijom za štednju novca na nekoliko godina ili više. Bitcoin je bolji od štednje novca u dolarima, akcijama, nekretninama, pa čak i u zlatu.

Zato pokušajte da zaboravite na trenutak na razumevanje blockchaina, digitalne valute, kriptografije, seed fraza, novčanika, rudarstva i svih ostalih nerazumljivih termina. Za sada, razgovarajmo o tome zašto ljudi kupuju Bitcoin: razlog je prostiji nego što vi mislite.

Zašto ljudi kupuju Bitcoin?

Naravno, svako ima svoj razlog za kupovinu Bitcoin-a. Jedan od razloga, koji verovatno često čujete, je taj što mu vrednost raste. Ljudi žele da se obogate. Uskoče kao spekulanti, krenu u vožnju i najverovatnije ih prodaju ubrzo nakon kupovine.

Međutim, čak i kada cena krene naglo prema gore i strmoglavo padne nazad, mnogi ljudi ostanu i nakon tog pada. Otkud mi to znamo? Broj aktivnih novčanika dnevno, koji je otprilike sličan broju korisnika Bitcoin-a, nastavlja da raste. Takođe, nakon svakog balona u istoriji Bitcoin-a, cena se nikada ne vraća na svoju cenu pre balona. Uvek ostane malo višlja. Bitcoin se penje, a svaka masovna spekulativna serija dovodi sve više i više ljudi.

Broj aktivnih Bitcoin novčanika neprekidno raste

„Aktivna adresa“ znači da je neko tog dana poslao Bitcoin transakciju. Donji grafikon je na logaritamskoj skali.

Izvor: Glassnode

Izvor: GlassnodeCena Bitcoina se neprestano penje

Kroz istoriju Bitcoin-a možemo videti divlje kolebanje cena, ali nakon svakog balona, cena se ostaje višlja nego pre. Ovo je cena Bitcoin-a na logaritamskoj skali.

Izvor: Glassnode

Izvor: GlassnodeTo pokazuje da se ljudi zadržavaju: potražnja za Bitcoin-om se povećava. Da je svaki masovni rast cena bio samo balon koji su iscenirali prevaranti koji žele brzo da se obogate, cena bi se vratila na nivo pre balona. To se dogodilo sa lalama, ali ne i sa Bitcoin-om.

I zašto se onda cena Bitcoin-a stalno povećava? Sve veći broj ljudi čuva Bitcoin dugoročno – oni razumeju šta Bitcoin može učiniti za njihovu štednju.

Zašto ljudi štede svoj novac u Bitcoin-u umesto na štednim računima, kućama, deonicama ili zlatu? Hajde da pogledajmo sve te metode štednje, i zatim da ih uporedimo sa Bitcoin-om.

Da li je vaš novac siguran u dolarima, kućama, akcijama ili zlatu?

Tokom mnogo godina, to su bile pristojne opcije za štednju. Međutim, sistem koji podržava vrednost svega ovoga je u krizi.

Dolari, Euri, Dinari

Dolari i sve ostale „tradicionalne“ valute koje proizvode vlade, stvorene su da izgube vrednost kroz inflaciju. Banke i tradicionalni monetarni sistem uzrokuju inflaciju stalnim stvaranjem i distribucijom novog novca. Kada Američke Federalne Rezerve objave ciljanu stopu od 2% inflacije, to znači da žele da vaš novac svake godine izgubi 2% od svoje vrednosti. Čak i sa inflacijom od samo 2%, vaša štednja u dolarima izgubiće polovinu vrednosti tokom 40-godišnjeg radnog veka.

Izveštena inflacija se danas opasno povečava, uprkos rastućem „buretu sa barutom“ koji bi mogao da explodira i dovede do masivne hiperinflacije. Što je više valute u opticaju, to je više baruta u buretu.

Naše vlade su ekonomiju napunile valutama da bankarski sistem ne bi propao nakon finansijske krize koja se dogodila 2008. godine. Od tada je većina glavnih centralnih banaka postavila vrlo niske kamatne stope, što pojedincima i korporacijama omogućava dobijanje jeftinijih kredita. To znači da mnogi pojedinci i korporacije podižu ogromne kredite i koriste ih za kupovinu druge imovine poput deonica, umetničkih dela i nekretnina. Sve ovo pozajmljivanje znači da stvaramo tone novog novca i stavljamo ga u opticaj.

Računi za podsticaje (stimulus bills) COVID-19 za 2020. godinu unose trilione u sistem. Ovoliko stvaranje valuta na kraju dovodi do inflacije – velikog gubitka u vrednosti valute.

Količina američkog dolara u opticaju gotovo se udvostručila od marta 2020. godine. Izvor

Količina američkog dolara u opticaju gotovo se udvostručila od marta 2020. godine. IzvorRačuni za podsticaje su bez presedana, toliko da je neko izmislio meme da opiše ovu situaciju.

Resurs koji vlade mogu da naprave u većem broju da bi platile svoje račune? Ne zvuči kao dobro mesto za štednju novca.

Kuće

Kuće su tokom prošlog veka bile pristojan način štednje novca. Međutim, pad cena nekretnina 2007. godine doveo je do toga da su mnogi vlasnici kuća izgubili svu ušteđevinu.

Danas su kuće gotovo nepristupačne za prosečnog čoveka. Jedan od načina da se ovo izmeri je koliko godišnjih zarada treba prosečnom čoveku da zaradi ekvivalent vrednosti prosečne kuće. Prema CityLab-u, publikaciji Bloomberg-a koja pokriva gradove, porodica može da priuštiti određenu kuću ako košta manje od 2,6 godišnjih prihoda domaćinstva te porodice.

Međutim, prema RZS (Republički zavod za statistiku) prosečan prihod porodičnog domaćinstva u Srbiji iznosi oko 570 EUR mesečno ili otprilike 7.000 EUR godišnje. Nažalost, samo najjeftinija područja van gradova imaju srednje cene kuća od oko 2,6 prosečnih godišnjih prihoda domaćinstva. U većim gradovima poput Beograda i Novog Sada srednja cena kuće je veća od 10 prosečnih godišnjih prihoda jednog domaćinstva.

Ako nekako možete sebi da priuštite kuću, ona bi mogla biti pristojna zaliha vrednosti. Dokle god ne doživimo još jedan krah i izvršitelji zaplene ovu imovinu mnogim vlasnicima kuća.

Akcije

Berza je u prošlosti takođe dobro poslovala. Međutim, sporo i stabilno povećanje tržišta događa se u dosadnom, predvidljivom svetu. Svakog dana vidimo sve manje toga. Nakon ubrzanja korona virusa, videli smo smo najbrži pad američke berze u istoriji od 25% – brži od Velike depresije.

Neki se odlučuju za ulaganje u obveznice i drugu finansijsku imovinu, ali ’prinosi’ za tu imovinu – procenat kamate zarađene na imovinu iz godine u godinu – stalno opada. Sve veći broj odredjenih imovina ima čak i negativne prinose, što znači da posedovanje te imovine košta! Ovo je veliki problem za sve koji se oslanjaju na penziju. Plus, s obzirom na to da su akcije denominovane u tradicionalnim valutama poput dolara i evra, inflacija pojede prinos koji investitor dobije.

Najgore od svega je to što ti isti ekonomski krahovi koji uzrokuju masovna otpuštanja i teško tržište rada takođe znače i nagli pad cena akcija. Čuvanje ušteđevine u akcijama može značiti i gubitak štednje i gubitak posla zbog recesije. Teška vremena mogu da vas prisile da svoje akcije prodate po vrlo malim cenama samo da biste platili svoje račune.

A to nije baš siguran način štednje novca.

Zlato

Vrednost zlata neprekidno se povećavala tokom 5000 godina, obično padajući onda kada berza obećava jače prinose.

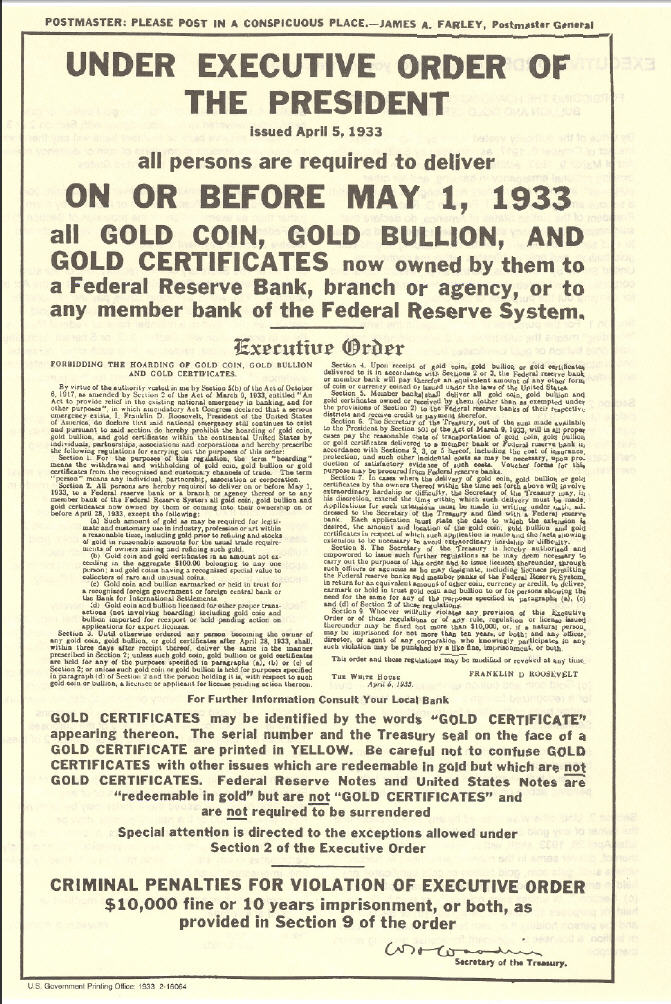

Evidencija vrednosti zlata je solidna. Međutim, zlato nosi i druge rizike. Većina ljudi poseduje zlato na papiru. Oni fizički ne poseduju zlato, već ga njihova banka čuva za njih. Zbog toga je zlato veoma podložno konfiskaciji od strane vlade.

Zašto bi vlada konfiskovala nečije zlato, a kamoli u demokratskoj zemlji u „slobodnom svetu“? Ali to se dešavalo i ranije. 1933. godine Izvršnom Naredbom 6102, predsednik Roosevelt naredio je svim Amerikancima da prodaju svoje zlato vladi u zamenu za papirne dolare. Vlada je iskoristila pretnju zatvorom za prikupljanje zlata u fizičkom obliku. Znali su da se zlato više poštuje kao zaliha vrednosti širom sveta od papirnih dolara.

Ako posedujete svoje zlato na nekoj od aplikacija za trgovanje akcijama, možete se kladiti da će vam ga država oduzeti ako joj zatreba. Čak i ako posedujete fizičko zlato, onda ga izlažete mogućnosti krađe – od strane kriminalca ili vaše vlade.

Vaša uštedjevina nije bezbedna.

Rast cena svih gore navedenih sredstava zavisi od našeg trenutnog političkog i ekonomskog sistema koji se nastavlja kao i tokom proteklih 100 godina. Međutim, danas vidimo ogromne pukotine u ovom sistemu.

Sistem ne funkcioniše dobro za većinu ljudi.

Od 1971. plate većine američkih radnika nisu rasle. S druge strane, bogatstvo koje imaju najbogatiji u društvu nalazi se na nivoima koji nisu viđeni više od 80 godina. U međuvremenu, ljudi sve manje i manje veruju institucijama poput banaka i vlada.

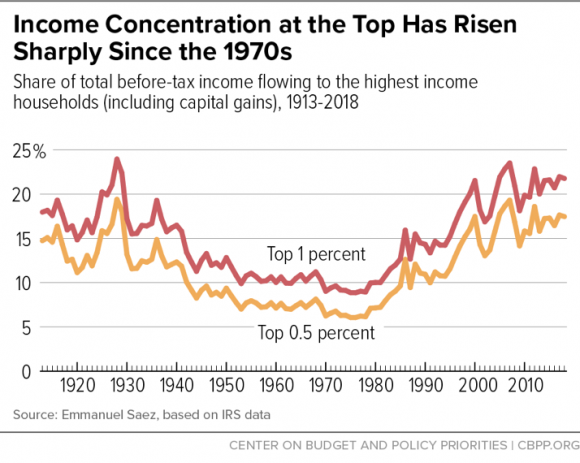

CBPP Nejednakost Bogatstva Tokom Vremena

CBPP Nejednakost Bogatstva Tokom VremenaŠirom sveta možemo videti dokaze o slamanju sistema kroz politički ekstremizam: izbor Trampa i drugih ekstremističkih desničarskih kandidata, Bregzit, pokret Occupy, popularizacija koncepta univerzalnog osnovnog dohotka, povratak pojma „socijalizam“ nazad u modu. Ljudi na svim delovima političkog i društvenog spektra osećaju problematična vremena i posežu za sve radikalnijim rešenjima.

Šta je bolje za štednju od dolara, kuća i akcija?

Pa kako ljudi mogu da štede novac u ovim teškim vremenima? Ili ne koriste tradicionalne valute, ili kupuju sredstva koja će zadržati vrednost u teškim vremenima.

Bitcoin ima najviše potencijala da zadrži vrednost kroz politička i ekonomska previranja od bilo koje druge imovine. Na tom putu će biti rupa na kojima će se rušiti ili pumpati, međutim, njegova svojstva čine ga takvim da će verovatno preživeti previranja kada druga imovina ne bude to mogla.

Šta Bitcoin čini drugačijim?

Bitcoini su retki.

Proces ‘rudarenja’ bitcoin-a, proizvodnju bitcoin-a čini veoma skupom, a Bitcoin protokol ograničava ukupan broj bitcoin-a na 21 milion novčića. To čini Bitcoin imunim na nagle poraste ponude. Ovo se veoma razlikuje od tradicionalnih valuta, koje vlade mogu da štampaju sve više kad god one to požele. Zapamtite, povećanje ponude vrši veliki pritisak na vrednost valute.

Bitcoini nemaju drugu ugovornu stranu.

Bitcoin se takođe razlikuje od imovine kao što su obveznice, akcije i kuće, jer mu nedostaje druga ugovorna strana. Druge ugovorne strane su drugi subjekti uključeni u vrednost sredstva, koji to sredstvo mogu obezvrediti ili vam ga uzeti. Ako imate hipoteku na svojoj kući, banka je druga ugovorna strana. Kada sledeći put dođe do velikog finansijskog kraha, banka vam može oduzeti kuću. Kompanije su kvazi-ugovorne strane akcijama i obveznicama, jer mogu da počnu da donose loše odluke koje utiču na njihovu cenu akcija ili na „neizvršenje“ duga (da ga ne vraćaju vama ili drugim poveriocima). Bitcoin nema ovih problema.

Bitcoin je pristupačan.

Svako sa 5 eura i mobilnim telefonom može da kupi i poseduje mali deo bitcoin-a. Važno je da znate da ne morate da kupite ceo bitcoin. Bitcoin-i su deljivi do 100-milionite jedinice, tako da možete da kupite Bitcoin u vrednosti od samo nekoliko eura. Neuporedivo lakše nego kupovina kuće, zlata ili akcija!

Bitcoin se ne može konfiskovati.

Banke drže većinu vaših eura, zlata i akcija za vas. Većina ljudi u razvijenom svetu veruje bankama, jer većina ljudi koji žive u današnje vreme nikada nije doživela konfiskaciju imovine ili ’šišanje’ od strane banaka ili vlada. Nažalost, postoji presedan za konfiskaciju imovine čak i u demokratskim zemljama sa snažnom vladavinom prava.

Kada vlada konfiskuje imovinu, ona obično ubedi javnost da će je menjati za imovinu jednake vrednosti. U SAD-u 1930-ih, vlada je davala dolare vlasnicima zlata. Vlada je znala da uvek može da odštampa još više dolara, ali da ne može da napravi više zlata. Na Kipru 2012. godine, jedna propala banka je svojim klijentima dala deonice banke da pokrije dolare klijenata koje je banka trebala da ima. I dolari i deonice su strmoglavo opali u odnosu na imovinu koja je uzeta od ovih ljudi.

Doći do bitcoin-a koji ljudi poseduju, biće mnogo teže jer se bitcoin-i mogu čuvati u novčaniku koji ne poseduje neka treća strana, a vi možete čak i da zapamtite privatne ključeve do vašeg bitcoin-a u glavi.

Bitcoin je za štednju.

Bitcoin se polako pokazuje kao najbolja opcija za dugoročnu štednju novca, posebno s obzirom na današnju ekonomsku klimu. Posedovanje čak i malog dela, je polisa osiguranja koja se isplati ako svet i dalje nastavi da ludi. Cena Bitcoin-a u dolarima može divlje da varira u roku od godinu ili dve, ali tokom 3+ godine skoro svi vide slične ili više cene od trenutka kada su ga kupili. U stvari, doslovno niko nije izgubio novac čuvajući Bitcoin duže od 3,5 godine – čak i ako je kupio BTC na apsolutnim vrhovima tržišta.

Imajte na umu da nakon ove tačke ti ljudi više nikada nisu videli rizik od gubitka. Cena se nikada nije smanjila niže od najviše cene u prethodnom ciklusu.

Po čemu se Bitcoin razlikuje od ostalih valuta?

Bitcoin funkcioniše tako dobro kao način štednje zbog svog neobičnog dizajna, koji ga čini drugačijim od bilo kog drugog oblika novca koji je postojao pre njega. Bitcoin je digitalna valuta, prvi i verovatno jedini primer valute koja ima ograničenu ponudu dok radi na otvorenom, decentralizovanom sistemu. Vlade strogo kontrolišu valute koje danas koristimo, poput dolara i eura, i proizvode ih za finansiranje ratova i dugova. Korisnici Bitcoin-a – poput vas – kontrolišu Bitcoin protokol.

Evo šta Bitcoin razlikuje od dolara, eura i drugih valuta:

Bitcoin je otvoren sistem.

Svako može da odluči da se pridruži Bitcoin mreži i primeni pravila softverskog protokola, što je dovelo do vrlo decentralizovanog sistema u kojem nijedan pojedinac ili entitet ne može da blokira transakciju, zamrzne sredstva ili da ukrade od druge osobe.Današnji savremeni bankarski sistem se uveliko razlikuje. Nekoliko banaka je dobilo poverenje da gotovo sve valute, akcije i druge vredne predmete čuvaju na “sigurnom” za svoje klijente. Da biste postali banka, potrebni su vam milioni dolara i neverovatne količine političkog uticaja. Da biste pokrenuli Bitcoin čvor i postali „svoja banka“, potrebno vam je nekoliko stotina dolara i jedno slobodno popodne.

Tako izgleda Bitcoin čvor – Node

MyNode čvor vam omogućava da postanete svoja banka za samo nekoliko minuta.

Tako izgleda Bitcoin čvor – Node

MyNode čvor vam omogućava da postanete svoja banka za samo nekoliko minuta.Bitcoin ima ograničenu ponudu.

Softverski protokol otvorenog koda koji upravlja Bitcoin sistemom ograničava broj novih bitcoin-a koji se mogu stvoriti tokom vremena, sa ograničenjem od ukupno 21.000.000 bitcoin-a. S druge strane, valute koje danas koristimo imaju neograničenu ponudu. Istorija i sadašnje odluke centralnih banaka govore nam da će vlade uvek štampati sve više i više valuta, sve dok valuta ne bude bezvredna. Sve ovo štampanje uzrokuje inflaciju, što pravi štetu običnim radnim ljudima i štedišama.

Tradicionalne valute su dizajnirane tako da opadaju vremenom. Svaki put kada centralna banka kaže da cilja određenu stopu inflacije, oni ustvari kažu da žele da vaš novac svake godine izgubi određeni procenat svoje vrednosti.

Bitcoin-ova ograničena ponuda znači da je on tako dizajniran da raste vremenom kako se potražnja za njim povećava.

Bitcoin putuje oko sveta za nekoliko minuta.

Svako može da pošalje bitcoin-e za nekoliko minuta širom sveta, bez obzira na granice, banke i vlade. Potrebno je manje od minuta da se transakcija pojavi na novčaniku primaoca i oko 60 minuta da se transakcija u potpunosti „obračuna“, tako da primaoc može da bude siguran da su primljeni bitcoin-i sada njegovi (6 konfirmacija bloka). Slanje drugih valuta širom sveta traje danima ili čak mesecima ako se šalju milionski iznosi, a podrazumeva i visoke naknade.

Neke vlade i novinari tvrde da ova sloboda putovanja koju pruža Bitcoin pomaže kriminalcima i teroristima. Međutim, transakciju Bitcoin-a je lakše pratiti nego većinu transakcija u dolarima ili eurima.

Bitcoin se može čuvati na “USB-u”.

Dizajn Bitcoin-a je takav da vam treba samo da čuvate privatni ključ do svojih ‘bitcoin’ adresa (poput lozinke do bankovnih računa) da biste pristupili svojim bitcoin-ima odakle god poželite. Ovaj privatni ključ možete da sačuvate na disku ili na papiru u obliku 12 ili 24 reči na engleskom jeziku. Kao rezultat toga, možete da držite Bitcoin-e vredne milione dolara u svojoj šaci.

Sve ostale valute danas možete ili da strpate u svoj dušek ili da ih poverite banci na čuvanje. Za većinu ljudi koji žive u razvijenom svetu, i koji ne osporavaju autoritet i poverenje u banku, ovo deluje sasvim dobro. Međutim, oni kojima je potrebno da pobegnu od ugnjetavačke vlade ili koji naljute pogrešne ljude, ne mogu verovati bankama. Za njih je sposobnost da nose svoju ušteđevinu bez potrebe za ogromnim koferom neprocenjiva. Čak i ako ne živite na mestu poput ovog, cena Bitcoin-a se i dalje povećava kada ih neko kome oni trebaju kupi.

Kako Bitcoin spašava svet?

Bitcoin, kao ultimativni način štednje, je cakum pakum, ali da li on pomaže u poboljšanju sveta u celini?

Kao što ćete početi da shvatate, ulazeći sve dublje i u druge sadržaje na ovoj stranici, mnogi temeljni delovi našeg današnjeg monetarnog sistema i ekonomije su duboko slomljeni. Međutim, oni koji upravljaju imaju korist od ovakvih sistema, pa se on verovatno neće promeniti bez revolucije ili mirnog svrgavanja od strane naroda. Bitcoin predstavlja novi sistem, sa nekoliko glavnih prednosti:

- Bitcoin popravlja novac, koji je milenijumima služio kao važan alat za rast i poboljšanje društva.

- Bitcoin vraća zdrav razum pozajmljivanju, uklanjanjem apsurdnih situacija poput negativnih kamatnih stopa (gde zajmitelj plaća da bi se zadužio).

- Bitcoin pokreće ulaganja u obnovljive izvore energije i poboljšava energetsku efikasnost u mreži, služeći kao „krajnji kupac“ za sve vrste energije.

Kako mogu da saznam više o Bitcoin-u?

Ovaj članak vam je dao osnovno razumevanje zašto biste trebali razmišljati o Bitcoin-u. Ako želite da saznate više, preporučujem ove resurse:

- Film Bitcoin: Kraj Novca Kakav Poznajemo

- Još uvek je rano za Bitcoin

- Zasto baš Bitcoin?

- Šta je to Bitcoin?

- The Bitcoin Whitepaper ← objavljen 2008. godine, ovo je izložio dizajn za Bitcoin.

-

@ 04c915da:3dfbecc9

2025-05-20 15:47:16

Here’s a revised timeline of macro-level events from The Mandibles: A Family, 2029–2047 by Lionel Shriver, reimagined in a world where Bitcoin is adopted as a widely accepted form of money, altering the original narrative’s assumptions about currency collapse and economic control. In Shriver’s original story, the failure of Bitcoin is assumed amid the dominance of the bancor and the dollar’s collapse. Here, Bitcoin’s success reshapes the economic and societal trajectory, decentralizing power and challenging state-driven outcomes.

Part One: 2029–2032

-

2029 (Early Year)\ The United States faces economic strain as the dollar weakens against global shifts. However, Bitcoin, having gained traction emerges as a viable alternative. Unlike the original timeline, the bancor—a supranational currency backed by a coalition of nations—struggles to gain footing as Bitcoin’s decentralized adoption grows among individuals and businesses worldwide, undermining both the dollar and the bancor.

-

2029 (Mid-Year: The Great Renunciation)\ Treasury bonds lose value, and the government bans Bitcoin, labeling it a threat to sovereignty (mirroring the original bancor ban). However, a Bitcoin ban proves unenforceable—its decentralized nature thwarts confiscation efforts, unlike gold in the original story. Hyperinflation hits the dollar as the U.S. prints money, but Bitcoin’s fixed supply shields adopters from currency devaluation, creating a dual-economy split: dollar users suffer, while Bitcoin users thrive.

-

2029 (Late Year)\ Dollar-based inflation soars, emptying stores of goods priced in fiat currency. Meanwhile, Bitcoin transactions flourish in underground and online markets, stabilizing trade for those plugged into the bitcoin ecosystem. Traditional supply chains falter, but peer-to-peer Bitcoin networks enable local and international exchange, reducing scarcity for early adopters. The government’s gold confiscation fails to bolster the dollar, as Bitcoin’s rise renders gold less relevant.

-

2030–2031\ Crime spikes in dollar-dependent urban areas, but Bitcoin-friendly regions see less chaos, as digital wallets and smart contracts facilitate secure trade. The U.S. government doubles down on surveillance to crack down on bitcoin use. A cultural divide deepens: centralized authority weakens in Bitcoin-adopting communities, while dollar zones descend into lawlessness.

-

2032\ By this point, Bitcoin is de facto legal tender in parts of the U.S. and globally, especially in tech-savvy or libertarian-leaning regions. The federal government’s grip slips as tax collection in dollars plummets—Bitcoin’s traceability is low, and citizens evade fiat-based levies. Rural and urban Bitcoin hubs emerge, while the dollar economy remains fractured.

Time Jump: 2032–2047

- Over 15 years, Bitcoin solidifies as a global reserve currency, eroding centralized control. The U.S. government adapts, grudgingly integrating bitcoin into policy, though regional autonomy grows as Bitcoin empowers local economies.

Part Two: 2047

-

2047 (Early Year)\ The U.S. is a hybrid state: Bitcoin is legal tender alongside a diminished dollar. Taxes are lower, collected in BTC, reducing federal overreach. Bitcoin’s adoption has decentralized power nationwide. The bancor has faded, unable to compete with Bitcoin’s grassroots momentum.

-

2047 (Mid-Year)\ Travel and trade flow freely in Bitcoin zones, with no restrictive checkpoints. The dollar economy lingers in poorer areas, marked by decay, but Bitcoin’s dominance lifts overall prosperity, as its deflationary nature incentivizes saving and investment over consumption. Global supply chains rebound, powered by bitcoin enabled efficiency.

-

2047 (Late Year)\ The U.S. is a patchwork of semi-autonomous zones, united by Bitcoin’s universal acceptance rather than federal control. Resource scarcity persists due to past disruptions, but economic stability is higher than in Shriver’s original dystopia—Bitcoin’s success prevents the authoritarian slide, fostering a freer, if imperfect, society.

Key Differences

- Currency Dynamics: Bitcoin’s triumph prevents the bancor’s dominance and mitigates hyperinflation’s worst effects, offering a lifeline outside state control.

- Government Power: Centralized authority weakens as Bitcoin evades bans and taxation, shifting power to individuals and communities.

- Societal Outcome: Instead of a surveillance state, 2047 sees a decentralized, bitcoin driven world—less oppressive, though still stratified between Bitcoin haves and have-nots.

This reimagining assumes Bitcoin overcomes Shriver’s implied skepticism to become a robust, adopted currency by 2029, fundamentally altering the novel’s bleak trajectory.

-

-

@ 9ca447d2:fbf5a36d

2025-05-22 14:01:52

Gen Z (those born between 1997 and 2012) are not rushing to stack sats, and Oliver Porter, Founder & CEO of Jippi, understands the challenge better than most. His strategy revolves around adapting Bitcoin education to fit seamlessly into the digital lives of young adults.

“We need to meet them where they are,” Oliver explains. “90% of Gen Z plays games. 70% expect to earn rewards.”

So, what will effectively introduce them to Bitcoin? In Oliver’s mind, the answer is simple: games that don’t feel preachy but still plant the orange pill.

Learn more at Jippi.app

That’s exactly what Jippi is. Based in Austin, Texas, the team has created a mobile augmented reality (AR) game that rewards players in bitcoin and sneakily teaches them why sound money matters.

“It’s Pokémon GO… but for sats,” Oliver puts it succinctly.

Jippi is like Pokemon Go, but for sats

Oliver’s Bitcoin journey, like many in the space, began long before he was ready. A former colleague had tried planting the seed years earlier, handing him a copy of The Bitcoin Standard. But the moment passed.

It wasn’t until the chaos of 2020 when lockdowns hit, printing presses roared, and civil liberties shrank that the message finally landed for him.

“The government got so good at doing reverse Robin Hood,” Oliver explains. “They steal from the working population and reward the rich.”

By 2020, though, the absurdity of the covid hysteria had caused his eyes to be opened and the orange light seemed the best path back to freedom.

He left the UK for Austin “one of the best places for Bitcoiners,” he says, and dove headfirst into the industry, working at Swan for a year before founding Jippi on PlebLab’s accelerator program.

Jippi’s flagship game lets players roam their cities hunting digital creatures, Bitcoin Beasts, tied to real-world locations. Catching them requires answering Bitcoin trivia, and the reward is sats.

No jargon. No hour-long lectures. Just gameplay with sound money principles woven right in.

The model is working. At a recent hackathon in Austin, Jippi beat out 14 other teams to win first place and $15,000 in prize money.

Oliver of Jippi won Top Builder Season 2 — PlebLab on X

“We’re backdooring Bitcoin education,” Oliver admits. “And while we’re at it, encouraging people to get outside and touch grass.”

Not everyone’s been thrilled. When Jippi team members visited one of the more liberal-leaning places in Texas, UT Austin, to test interest in Bitcoin, they found some seriously committed no-coiners on the campus.

“One young woman told me, ‘I would rather die than talk about Bitcoin,'” Oliver recalls, highlighting the cultural resistance that’s built up among younger demographics.

This resistance is backed by hard data. According to Oliver, some of the Bitcoin podcasters they met with in the space to do market research reported that less than 1% of their listeners are from Gen Z and that number is dropping.

“Unless we find a way to capture their interest in a meaningful way, there’s going to be a big problem around trying to sway Gen Z away from the siren call of s***coins and crypto casinos and towards Bitcoin,” Oliver warns.

Jippi’s next big move is Las Vegas, where they’ll launch the Beast Catch experience at the Venetian during a major Bitcoin event. To mark the occasion, they’re opening up six limited sponsorship spots for Bitcoin companies, each one tied to a custom in-game beast.

Jippi looks to launch a special event at Bitcoin 2025

“It’s real estate inside the game,” Oliver explains. “Brands become allies, not intrusions. You get a logo, company name, and call to action, so we can push people to your site or app.”

Bitcoin Well—an automatic self-custody Bitcoin platform—has claimed Beast #1. Only five exclusive spots remain for Bitcoin companies to “beastify their brand” through Jippi’s immersive AR game.

“I love the Jippi mission. I think gamified learning is how we will onboard the next generation and it’s exciting to see what the Jippi team is doing! I love working with bitcoiners towards our common mission – bullish!” said Adam O’Brien, Bitcoin Well CEO.

Jippi’s sponsorship model is simple: align incentives, respect users, and support builders. Instead of throwing ad money at tech giants, Bitcoin companies can connect with new users naturally while they’re having fun and earning sats in the process.

For Bitcoin companies looking to reach a younger demographic, this represents a unique opportunity to showcase their brand to up to 30,000 potential customers at the Vegas event.

Jippi Bitcoin Beast partnership

While Jippi’s current focus is simple, get the game into more cities, Oliver sees a future where AR glasses and AI help personalize Bitcoin education even further.

“The magic is going to really happen when Apple releases the glasses form factor,” he says, describing how augmented reality could enhance real-world connections rather than isolate users.

In the longer term, Jippi aims to evolve from a free-to-play model toward a pay-to-play version with higher stakes. Users would form “tribes” with friends to compete for substantial bitcoin prizes, creating social connections along with financial education.

Unlike VC-backed startups, Jippi is raising funds pleb style via Timestamp, an open investment platform for Bitcoin companies.

“You don’t have to be an accredited investor,” Oliver explains. “You’re directly supporting the parallel Bitcoin economy by investing in Bitcoin companies for equity.”

Anyone can invest as little as $100. Perks include early access, exclusive game content, and even creating your own beast design with your name/pseudonym and unique game lore. Each investment comes with direct ownership of an early-stage Bitcoin company like Jippi.

For Oliver, this is more than just a business. It’s about future-proofing Bitcoin adoption and ensuring Satoshi’s vision lives on, especially as many people are lured by altcoins, NFTs, and social media dopamine.

“We’re on the right side of history,” he says firmly. “I want my grandkids to know that early on in the Bitcoin revolution, games like Jippi helped make it stick.”

In a world increasingly absorbed by screens and short attention spans, Jippi’s combination of outdoor play, sats rewards, and Bitcoin education might be exactly the bridge Gen Z needs.

Interested in sponsoring a Beast or investing in Jippi? Reach out to Jippi directly by heading to their partnerships page on their website or visit their Timestamp page to invest in Jippi today.

-

@ 21335073:a244b1ad

2025-05-21 16:58:36

The other day, I had the privilege of sitting down with one of my favorite living artists. Our conversation was so captivating that I felt compelled to share it. I’m leaving his name out for privacy.

Since our last meeting, I’d watched a documentary about his life, one he’d helped create. I told him how much I admired his openness in it. There’s something strange about knowing intimate details of someone’s life when they know so little about yours—it’s almost like I knew him too well for the kind of relationship we have.

He paused, then said quietly, with a shy grin, that watching the documentary made him realize how “odd and eccentric” he is. I laughed and told him he’s probably the sanest person I know. Because he’s lived fully, chasing love, passion, and purpose with hardly any regrets. He’s truly lived.

Today, I turn 44, and I’ll admit I’m a bit eccentric myself. I think I came into the world this way. I’ve made mistakes along the way, but I carry few regrets. Every misstep taught me something. And as I age, I’m not interested in blending in with the world—I’ll probably just lean further into my own brand of “weird.” I want to live life to the brim. The older I get, the more I see that the “normal” folks often seem less grounded than the eccentric artists who dare to live boldly. Life’s too short to just exist, actually live.

I’m not saying to be strange just for the sake of it. But I’ve seen what the crowd celebrates, and I’m not impressed. Forge your own path, even if it feels lonely or unpopular at times.

It’s easy to scroll through the news and feel discouraged. But actually, this is one of the most incredible times to be alive! I wake up every day grateful to be here, now. The future is bursting with possibility—I can feel it.

So, to my fellow weirdos on nostr: stay bold. Keep dreaming, keep pushing, no matter what’s trending. Stay wild enough to believe in a free internet for all. Freedom is radical—hold it tight. Live with the soul of an artist and the grit of a fighter. Thanks for inspiring me and so many others to keep hoping. Thank you all for making the last year of my life so special.

-

@ 57d1a264:69f1fee1

2025-05-22 13:13:36

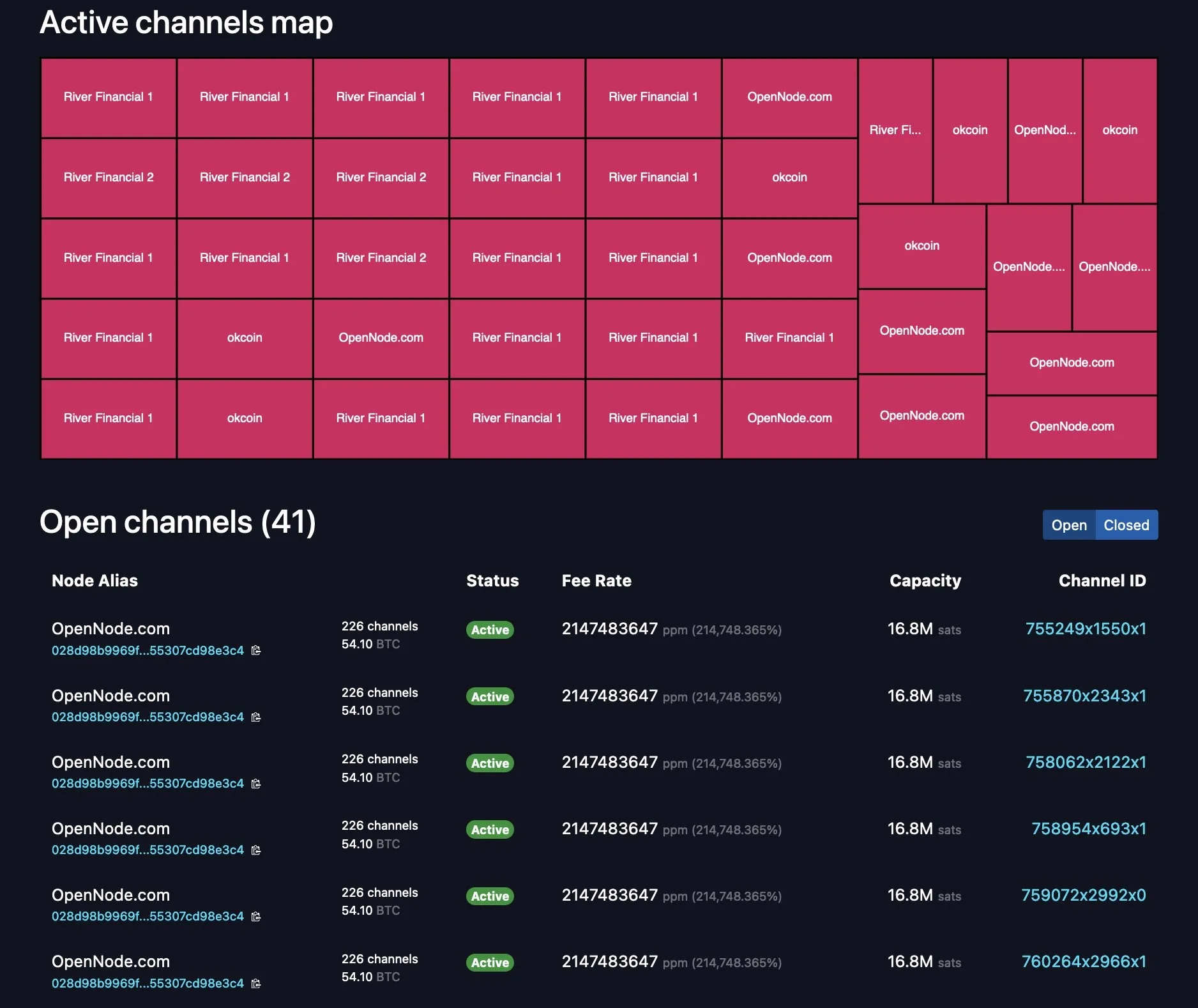

Graphics materials for Bitcoin Knots https://github.com/bitcoinknots branding. See below guide image for reference, a bit cleaner and scalable:

Font family "Aileron" is provided free for personal and commercial use, and can be found here: https://www.1001fonts.com/aileron-font.html

Source: https://github.com/Blissmode/bitcoinknots-gfx/tree/main

https://stacker.news/items/986624

-

@ 57d1a264:69f1fee1

2025-05-22 12:36:20

Graphics materials for Bitcoin Knots https://github.com/bitcoinknots branding. See below guide image for reference, a bit cleaner and scalable:

Font family "Aileron" is provided free for personal and commercial use, and can be found here: https://www.1001fonts.com/aileron-font.html

Source: https://github.com/Blissmode/bitcoinknots-gfx/tree/main

https://stacker.news/items/986587

-

@ 7e6f9018:a6bbbce5

2025-05-22 18:17:57

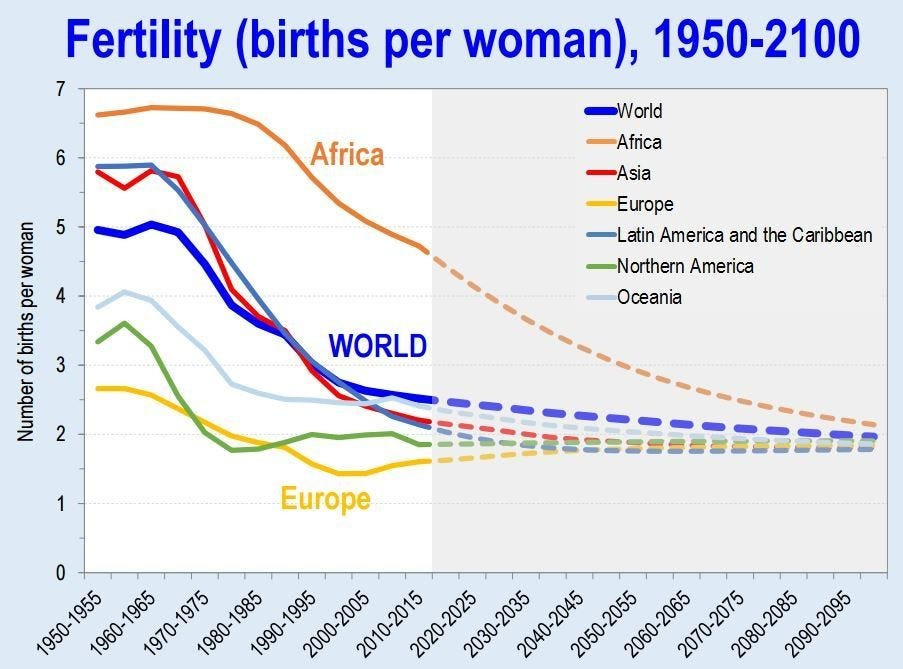

Governments and the press often publish data on the population’s knowledge of Catalan. However, this data only represents one stage in the linguistic process and does not accurately reflect the state of the language, since a language only has a future if it is used. Knowledge is a necessary step toward using a language, but it is not the final stage — that stage is actual use.

So what is the state of Catalan usage? If we look at data on regular use, we see that the Catalan language has remained stagnant over the past hundred years, with nearly the same number of regular speakers. In 1930, there were around 2.5 million speakers, and in 2018, there were 2.7 million.

Regular use of Catalan in Catalonia, in millions of speakers. The dotted segments are an estimate of the trend, based on the statements of Joan Coromines and adjusted according to Catalonia’s population growth.

Regular use of Catalan in Catalonia, in millions of speakers. The dotted segments are an estimate of the trend, based on the statements of Joan Coromines and adjusted according to Catalonia’s population growth.These figures wouldn’t necessarily be negative if the language’s integrity were strong, that is, if its existence weren’t threatened by other languages. But the population of Catalonia has grown from 2.7 million in 1930 to 7.5 million in 2018. This means that today, regular Catalan speakers make up only 36% of Catalonia’s population, whereas in 1930, they represented 90%.

Regular use of Catalan in Catalonia, as a percentage of speakers. The dotted segments are an estimate of the trend, based on the statements of Joan Coromines and adjusted according to Catalonia’s population growth.

Regular use of Catalan in Catalonia, as a percentage of speakers. The dotted segments are an estimate of the trend, based on the statements of Joan Coromines and adjusted according to Catalonia’s population growth.The language that has gained the most ground is mainly Spanish, which went from 200,000 speakers in 1930 to 3.8 million in 2018. Moreover, speakers of other foreign languages (500,000 speakers) have also grown more than Catalan speakers over the past hundred years.

Notes, Sources, and Methodology

The data from 2003 onward is taken from Idescat (source). Before 2003, there are no official statistics, but we can make interpretations based on historical evidence. The data prior to 2003 is calculated based on two key pieces of evidence:

-

1st Interpretation: In 1930, 90% of the population of Catalonia spoke Catalan regularly. Source and evidence: The Romance linguist Joan Coromines i Vigneaux, a renowned 20th-century linguist, stated in his 1950 work "El que s'ha de saber de la llengua catalana" that "In this territory [Greater Catalonia], almost the entire population speaks Catalan as their usual language" (1, 2).\ While "almost the entire population" is not a precise number, we can interpret it quantitatively as somewhere between 80% and 100%. For the sake of a moderate estimate, we assume 90% of the population were regular Catalan speakers, with the remaining 10% being immigrants and officials of the Spanish state.

-

2nd Interpretation: Regarding population growth between 1930 and 1998, on average, 60% is due to immigration (mostly adopting or already using Spanish language), while 40% is natural growth (likely to acquire Catalan language from childhood). Source and evidence: Between 1999 and 2019, when more detailed data is available, immigration accounted for 68% of population growth. From 1930 to 1998, there was a comparable wave of migration, especially between 1953 and 1973, largely of Spanish-speaking origin (3, 4, 5, 6). To maintain a moderate estimate, we assume 60% of population growth during that period was due to immigration, with the ratio varying depending on whether the period experienced more or less total growth.

-

-

@ bf47c19e:c3d2573b

2025-05-22 21:03:52

Originalni tekst na bitcoin-balkan.com.

Pregled sadržaja

- Šta je finansijski samo-suverenitet?

- Zašto smo prestali da koristimo zlatni standard?

- Šta fali tradicionalnoj valuti i centralnim bankama?

- Kako mogu ljudi da mi ukradu novac ako je u banci?

- Kako ljudi koriste moje finansijske podatke protiv mene?

- Kako ljudi kontrolišu sa kim obavljam transakcije?

- Kako da povratimo svoj finansijski samo-suverenitet?

- Kako Bitcoin funkcioniše?

- Pa onda, zašto Bitcoin?

- Po čemu je Bitcoin bolji od sistema tradicionalnih valuta?

- Kako Bitcoin štiti od Inflacije?

- Kako Bitcoin štiti od Zaplene?

- Kako Bitcoin štiti Privatnost?

- Kako Bitcoin štiti od Cenzure?

- Šta će vlada i banke učiniti sa Bitcoin-om?

- Da li je vrednost Bitcoin-a nestabilna?

- Da li je Bitcoin novac?

- Bitcoin kao Zaliha Vrednosti

- Bitcoin kao Sredstvo Razmene

- Bitcoin kao Obračunska Jedinica

- Bitcoin kao Sistem Kontrole

- Šta je sa „Sledećim Bitcoin-om“?

- Na kraju

Kratki uvod u bezbednost, privatnost i slobodu vašeg novca.

Pre nego što saznate kako morate znati zašto.

Šta je finansijski samo-suverenitet?

Zamislite da u ruci imate zlatni novčić, jedan od najjednostavnijih i najčistijih oblika finansijskog samo-suvereniteta.

Da biste držali taj zlatni novčić, ne morate da se složite sa bilo kojim Uslovima korišćenja ili Politikom privatnosti, da se pridržavate bilo kojih KYC ili AML propisa, da pokažete ličnu kartu, da navedete svoje ime ili jedinstveni matični broj.

Samo ga držite u ruci i njime možete platiti bilo šta, davanjem tog novčića nekom drugom da ga drži u ruci. To je čista sloboda.

Pored slobode onoga što kupujete svojim novčićem, niko ne može magično znati kome plaćate ili koju robu/usluge kupujete tim zlatni novčićem, jer vaša privatnost nije ugrožena sa zlatom.

A pošto imate svoju privatnost, niko ne može znati za vaše transakcije, pa niko ne može da odluči da ograniči ili kontroliše za šta koristite taj zlatni novčić.

Hiljadama godina zlato je bilo globalni standard novca.

Svi su održavali svoj finansijski samo-suverenitet, a privatnost i sloboda svačijeg novca su poštovani.

Zaista je bilo tako jednostavno.

Zašto smo prestali da koristimo zlatni standard?

Trenutni globalni bankarski sistem i sistem tradicionalnih valuta, bankari su vrlo polako implementirali u proteklih 100+ godina.

Udružili su se sa svetskim vladama koje su svima oduzele zlato pod pretnjom nasilja.

Na primer, nakon što je Federalna banka rezervi osnovana u SAD-u 1913. godine, američka vlada je nasilno oduzela svo zlato 1933. godine, prisiljavajući sve da koriste nove centralne banke i sistem novčanica Federalnih rezervi.

„Dostavite svoje celokupno zlato u naše sefove u zamenu za bezvredni papir, ili ćemo upotrebiti silu nad vama.“

„Dostavite svoje celokupno zlato u naše sefove u zamenu za bezvredni papir, ili ćemo upotrebiti silu nad vama.“Banke su u početku zamenile zlatni standard papirnim priznanicama zvane zlatni sertifikati, ali nakon što je prošlo dovoljno vremena, banke su u osnovi jednostavno prestale da ih otkupljuju za zlato.

Zlatni sertifikati izdavani od banaka (novčanice ili „gotovina“) u tom trenutku bili su samo bezvredni papir, ali zbog vladine pretnje nasiljem, svi su bili primorani da nastave da koriste novčanice Federalnih rezervi.

Od skora, banke koriste digitalnu bazu podataka, u kojoj doslovno mogu stvoriti novac ni iz čega, čak i da ga ne moraju štampati na papiru.

Predsednik Federalnih rezervi priča kako oni „štampaju“ novac.

Oni su učvrstili svoju moć da manipulišu i naduvaju globalnu novčanu masu, nadgledaju finansijske transakcije svih i kontrolišu protok svih tradicionalnih valuta u svom bankarskom sistemu.

Banke sada kontrolišu sve.

Jednom kada su centralni bankari uspešno preuzeli kontrolu nad novčanom masom u svetu, zajedno sa sposobnošću svih da slobodno vrše transakcije i trguju, svet je kolektivno izgubio bezbednost, slobodu i privatnost svog novca.

Šta fali tradicionalnoj valuti i centralnim bankama?

Nakon impelentacije trenutnog globalnog bankarskog sistema i sistema tradicionalnih valuta, svetu nije preostao drugi izbor nego da veruje bankarima i političarima da vode globalni finansijski sistem na pošten način.

„Koren problema tradicionalne valute je potpuno poverenje potrebno za njeno funkcionisanje. Centralnoj banci se mora verovati da neće devalvirati valutu, ali istorija tradicionalnih valuta je puna kršenja tog poverenja. Bankama se mora verovati da čuvaju naš novac i prenose ga elektronskim putem, ali ga daju u talasima kreditnih balona sa malim delićem rezerve. ““ — Satoshi Nakamoto

Istorija zloupotrebe tradicionalnih valuta može se grupisati u 3 kategorije:

• Bezbednost. Loši ljudi kradu vaš novac ili vrednost vašeg novca, ponekad na očigledne načine, ponekad na podle načine.

• Privatnost. Loši ljudi nadgledaju sve vaše privatne finansijske transakcije, i koriste vaše lične finansijske podatke protiv vas.

• Sloboda. Loši ljudi kontrolišu na koji način možete da trošite sopstveni novac, sa kim možete da obavljate transakcije, koliko možete da potrošite itd.

Kako mogu ljudi da mi ukradu novac ako je u banci?

Evo nekoliko primera:

-

Krađa inflacijom: Ovo je primarni način na koji banke kradu vaš novac i jedan od najpodlijih. Kada centralne banke izdaju novi novac, bilo štampanjem na bezvrednom papiru, ili samo dodavanjem knjigovodstvenog unosa u bazu podataka koju kontrolišu, one naduvaju globalnu novčanu masu. Inflacija krade kupovnu moć svih koji drže deo te valute, jednostavno zato što je sada više te valute u opticaju. Zlato se ne može stvoriti, pa su bankari umesto toga izmislili sistem papirnog novca.

-

Krađa zaplenom: Ovo je jedan od načina na koji vlade mogu ukrasti vaš novac. Da li ste ikada čuli za zaplenu imovine? Ako policajac posumnja da je vaša imovina korišćena u krivičnom delu, može je zapleniti, a vi se morate boriti da biste povratili vašu ukradenu imovinu. Ili, drugi primer: Pokušajte da uđete u zemlju sa više od 10.000 USD u džepu, a ne da je prijavite, i pogledajte šta će se dogoditi. Sve je isto: krađa od strane drugih ljudi sa oružjem.

-

Krađa putem oporezivanja: Ovo je još jedan način na koji vam vlade kradu novac. Ne sporim da li je oporezivanje etično ili ne, samo konstatujem činjenicu da vaša vlada može da primora vašu banku da im da vaš novac, a ovo je bezbednostna ranjivost. Da bi novac bio siguran, mora biti nezaplenjiv, a vlade mogu da zaplene vaše bankovne račune.

Kako ljudi koriste moje finansijske podatke protiv mene?

Ako fizičku tradicionalnu valutu predate drugoj osobi, u obliku papirnog novca ili kovanica, relativno je lako zaštititi privatnost svoje transakcije, baš kao što bi bilo da koristite zlatnike.

Međutim, ako koristite kreditne kartice, debitne kartice, bankovne transfere, PayPal, Venmo, LINE Pay, WeChat Pay ili bilo koju drugu mrežu za plaćanje koja je centralno kontrolisana, aktivno pristajete da se odreknete privatnosti podataka svih svojih privatnih finansijskih transakcija i sve ih dajete poverljivoj trećoj strani.

Kada su svi podaci i metapodaci vaših finansijskih transakcija prijavljeni u centralnu bazu podataka, onaj ko ima pristup toj bazi podataka može da koristi vaše podatke protiv vas.

Evo nekoliko osnovnih primera:

- Ako ste kupili robu rizičnog životnog stila poput cigareta, banka može reći vašoj osiguravajućoj kompaniji da poveća vaše osiguranje.

- Ako ste kupili nešto što je ilegalno, poput droga za rekreaciju, vaša banka može reći vašoj vladi da vas zakonski goni.

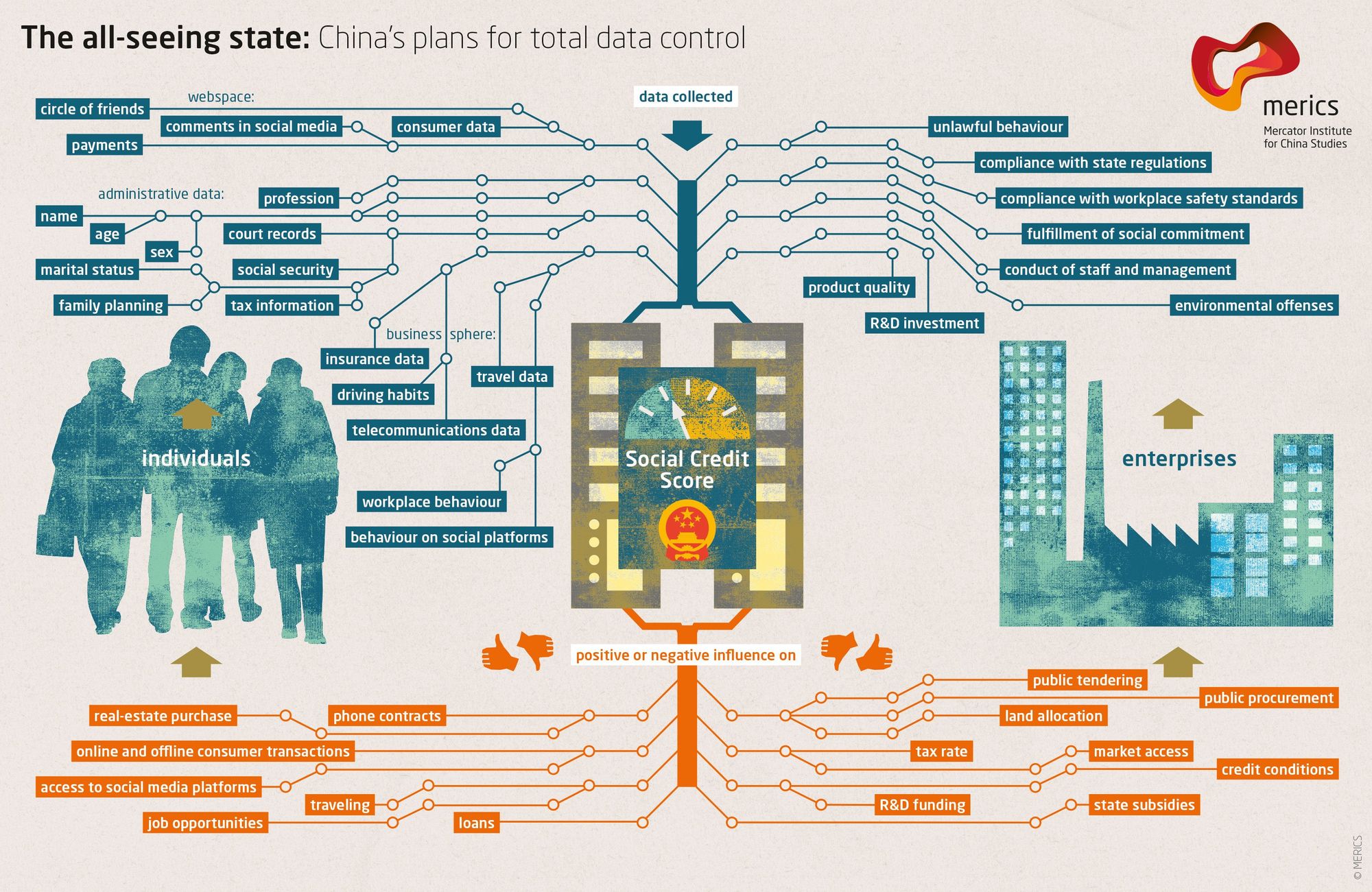

Ali u slučaju nekih represivnih vlada, oni su to odveli do ekstrema. Oni centralno prikupljaju sve finansijske transakcije i druge podatke svih svojih građana i stvorili su totalitarni Sistem Socijalnih Bodova (eng. Social Credit Score):

Prepoznavanje lica je jedan od elemenata kineskih napora za praćenje

Prepoznavanje lica je jedan od elemenata kineskih napora za praćenjeZapisi George Orwell-a već su postali stvarnost u Kini zbog sistema tradicionalnih valuta centralne banke i platnih mreža koje su izgrađene na njemu.

Ako mislite da se to neće dogoditi u vašoj zemlji, razmislite ponovo.

To se dešava vrlo polako, ali na kraju će sve svetske vlade primeniti Sistem Socijalnih Bodova, dok je Kina to tek prva učinila.

Kako ljudi kontrolišu sa kim obavljam transakcije?

U prvom primeru sa zlatnim novčićem, kada ga predate nekom drugom kao plaćanje za robu ili uslugu, ne postoji centralizovana evidencija vaše platne transakcije i imate savršenu privatnost.

Međutim, u centralnom bankarskom sistemu, budući da banka ima i znanje o podacima o vašim transakcijama i moć da kontroliše vaša sredstva, oni mogu proceniti niz pravila da bi odlučili da li žele da dozvole vašu transakciju ili da to odbiju, takođe kao i izvršenje te odluke kontrolišući vaša sredstva.

Tako su vlade naoružale tradicionalne valute i centralni bankarski sistem kao Sistem Kontrole nad svojim građanima.

Da rezimiramo: Pošto ste se odrekli bezbednosti i privatnosti svog novca, izgubili ste i svoju finansijsku slobodu.

“Privatnost nije o tome da nešto treba sakriti. Privatnost je o tome da nešto treba zaštititi.” — Edward Snowden

Kako da povratimo svoj finansijski samo-suverenitet?

Pokret Cypherpunk pokrenuli su pojedinci koji su shvatili važnost zaštite privatnosti i slobode pojedinačnih korisnika na Internetu.

Cypherpunk-ovi su verovali da se gore opisani problemi mogu rešiti samo potpuno novim novčanim sistemom, koji poštuje i štiti bezbednost, privatnost i slobodu pojedinca.

Mnogi od Cypherpunk-era pokušali su da izgrade nove etičke sisteme e-gotovine koji bi mogli da zamene tradicionalne valute i centralno bankarstvo.

Bilo je mnogo teških računarskih problema koje je trebalo prevazići u stvaranju tako istinski decentralizovanog sistema, i ako su neki od njih bili blizu cilja, svi su propali.

Odnosno, sve dok jedan pseudonim Cypherpunk-a to konačno nije shvatio 2008. godine: kombinacijom digitalnih potpisa, distribuirane knjige i peer-to-peer mreže, rođen je Bitcoin.

Kako Bitcoin funkcioniše?

Baš kao što ne treba da znate kako Internet funkcioniše da bi gledali slike mačaka na Internetu, razumevanje tehničke složenosti načina na koji Bitcoin radi „ispod haube“ nije neophodno da biste ga koristili i postigli sopstveni finansijski samo-suverenitet.

Važna stvar koju želim da saznate iz ovog članka je da iako većina novih tehnologija u početku ima loše korisničko iskustvo, Bitcoin svesno i vrlo namerno ne žrtvuje svoje osnovne filozofske principe da bi brže pridobio nove korisnike, ili da bi poboljšao korisničko iskustvo.

Najpametniji Cypherpunk-ovi rade na poboljšanju korisničkog iskustva.

Tehnologija će se sa vremenom poboljšavati, baš kao i za Internet.

Pa onda, zašto Bitcoin?

Reći ću vam zašto:

Jer Bitcoin poštuje bezbednost, privatnost i slobodu pojedinca.

Po čemu je Bitcoin bolji od sistema tradicionalnih valuta?

Za početak, Bitcoin nema Uslove korišćenja, Politiku privatnosti i Propise o usklađenosti sa KYC/AML. (Know Your Costumer & Anti-money Laundering)

Bitcoin je uspešan primer implementacije kripto-anarhije, gde su jedina pravila kriptografija, matematika i jak skup konsenzusnih pravila.

To je distribuirani i nepoverljivi sistem zasnovan na finansijskim podsticajima i nijedna osoba ili centralizovani entitet ne može da kontroliše Bitcoin.

Ono što je najvažnije, Bitcoin vam omogućava da odustanete od tradicionalnih valuta, sistema delimičnih rezervi i centralnog bankarstva rešavanjem osnovnih problema poverenja:

- Sigurnost od inflacije korišćenjem fiksnog snabdevanja

- Sigurnost od zaplene korišćenjem ključeva za kontrolu sredstava

- Privatnost plaćanja korišćenjem pseudonimnih identiteta

- Sloboda protiv cenzure korišćenjem peer to peer mreže

Kako Bitcoin štiti od Inflacije?

Jedno od najkritičnijih pravila konsenzusa o Bitcoin-u je da može postojati najviše 21,000,000 Bitcoin-a.

Nakon izdavanja svih Bitcoin-a, nikada više ne može doći do stvaranja novih Bitcoin-a.

Stoga je Bitcoin deflaciona valuta, koja sprečava ljude da ukradu vaš novac ili njegovu vrednost naduvavanjem novčane mase.

Monetarna Inflacija Bitcoin-aKako Bitcoin štiti od Zaplene?

Bitcoin se može preneti samo pomoću kriptografskog privatnog ključa koji kontroliše sredstva.

Nijedan bitcoin nikada ne izadje van sistema.

Nijedna vlada, banka ili sudski nalog ne mogu zapleniti ta sredstva.

Jednostavno ne postoji način da se takva odredba ili naredba sprovede od bilo kog „organa vlasti“, jer Bitcoin ne priznaje nijedno „ovlašćenje“ u svom sistemu.

Bitcoin je potpuno samo-suveren sistem i zbog svoje distribuirane prirode ne može se ugasiti.

Postoji zbog sopstvenih zasluga, samo zato što ljudi veruju u to.

Kako Bitcoin štiti Privatnost?

Bitcoin ne traži vaše ime ili druge detalje koji mogu lično da vas identifikuju.

Vaš identitet je kriptografski, a ne vaše stvarno ime.

Dakle, vaš identitet izgleda otprilike kao 1vizSAISbuiKsbt9d8JV8itm5ackk2TorC, a ne kao „Stefan Petrovič“.

Pored toga, niko ne zna ko kontroliše sredstva na datoj Bitcoin adresi, a nova tehnologija se neprestano razvija kako bi se poboljšala privatnost Bitcoin-a.

Kako Bitcoin štiti od Cenzure?

Peer-to-peer Bitcoin mreža je u potpunosti distribuirana.

To znači da ako jedan čvor pokuša da cenzuriše vašu transakciju, neće uspeti ukoliko * svaki * čvor(Node) ne izvrši cenzuru vaše transakcije.

Šta će vlada i banke učiniti sa Bitcoin-om?

Neke zemlje su pokušale da ga regulišu, kontrolišu, isključe itd., ali nijedna od njih nije uspela.

Čini se da uglavnom samo žele da koriste postojeći sistem centralnih banaka da bi kontrolisali kako ljudi trguju tradicionalnim valutama za Bitcoin, i naravno žele da oporezuju Bitcoin na bilo koji mogući način.

Evo nekoliko uobičajenih tvrdnji vlada i banaka o Bitcoin-u:

Evropska centralna banka kaže da Bitcoin nije valuta i upozorava da je vrlo nestabilna.

Evropska centralna banka kaže da Bitcoin nije valuta i upozorava da je vrlo nestabilna.„Bitcoin, izgleda samo kao prevara“, rekao je gospodin Tramp. „Ne sviđa mi se jer je to još jedna valuta koja se takmiči sa dolarom.“

Da li je vrednost Bitcoin-a nestabilna?

Ako umanjite grafikon cena, videćete da Bitcoin-u neprekidno raste vrednost od kada je stvoren, trgujući sa manje od 0,01 USD i polako se penje na preko 60.000 USD na nedavnom vrhuncu početkom 2021. godine.

Cena Bitcoina od 2011. godine

Cena Bitcoina od 2011. godineTo je zato što je njegova ponuda fiksna i ljudi cene njegovu nestašicu.

Sa većom potražnjom i fiksnom ponudom, cene vremenom rastu.

Kako godine odmiču, njegova vrednost će se povećavati kako novi korisnici počinju da drže Bitcoin. (U svetu Bitcoina držanju kažemo HODL. Drži bitcoin. Hodl bitcoin.)

Da li je Bitcoin novac?

Da biste odgovorili na pitanje da li je Bitcoin novac ili ne, prvo morate definisati pojam „novac“.

Nažalost, reč „novac“ koristimo da bismo opisali nekoliko vrlo različitih komplikovanih koncepata, koji su svi potpuno odvojeni.

Termin „novac“ se zapravo odnosi na:

- Zaliha Vrednosti (Store of Value)

- Sredstvo Razmene ( Medium of Exchange)

- Obračunska Jedinica (Unit of Account)

- Sistem Kontrole (System Control)

Bitcoin kao Zaliha Vrednosti

Ovaj tweet to savršeno objašnjava:

Sinov prijatelj: “Matt, šta će se dogoditi ako novčić od 1 funte usitnite na pola?”

Dobijaš dva komada bezvrednog metala. Ako zlatnik usitnite na pola, dobićete dva zlatnika, od kojih svaki vredi polovinu onoga što je novčić bio.

Sin: „… isto tako kao sa zlatom jeste sa bitcoinima“.

Bitcoin je potpuno deljiv i deluje kao izvrsna zaliha vrednosti, baš kao što je i zlato već hiljadama godina.

Bitcoin kao Sredstvo Razmene

Bitcoin je dobro služio kao sredstvo razmene za svoje rane korisnike.

Ali skaliranje Bitcoin-a na globalni nivo koji bi mogao da posluži svim ljudima je veliki izazov, jer se osnovna „blockchain“ tehnologija ne skalira na globalni nivo.

Da bi rešio ovaj problem skaliranja, Satoshi je izumeo koncept kanala plaćanja, a u kombinaciji sa malo pomoći drugih briljantnih računarskih naučnika Cipherpunk-a koji su poboljšali koncept tokom poslednjih 10 godina, sada imamo mrežu Lightning, koja omogućava da se Bitcoin koristi kao odlično Sredstvo Razmene, koje se vremenom može proširiti na globalni nivo.

Bitcoin kao Obračunska Jedinica

Najmanja obračunska jedinica Bitcoin-a nazvana je po njenom tvorcu, Satoshi-u.

Jedan Bitcoin je jednak 100.000.000 Satoshi-a.

Na kraju, kako se robe i usluge sve češće razmenjuju za Bitcoin, sve više ljudi će koristiti Bitcoin ili „Sats“ kao obračunsku jedinicu.

Bitcoin kao Sistem Kontrole

Budući da je Bitcoin dizajniran da poštuje i štiti ljudska prava pojedinca, posebno bezbednost, privatnost i slobodu novca; ne bi bio dobar Sistem Kontrole i ne može se koristiti za ugnjetavanje ljudi, kao što se dešava sa tradicionalnim valutama i sistemima centralnog bankarstva koji to trenutno vrlo dobro rade.

Šta je sa „Sledećim Bitcoin-om“?

Kao što može biti samo jedan „globalni“ Internet, tako može biti i samo jedan globalni novac, a stigao je i novi Bitcoin Standard.

Sve ostalo je ili direktna prevara ili gubljenje vremena.

Ako bi neko želeo da vam proda „Sledeće Zlato“, da li biste ga kupili?

Na kraju

Nadam se da vam je ovaj članak pomogao da razumete zašto je Bitcoin stvoren i kako može da pomogne svetu da se oslobodi tradicionalnih valuta i sistema centralnog bankarstva koji je veoma duboko integrisan u naše trenutno društvo.

Evo nekoliko misli koje treba poneti sa sobom:

- Bitcoin nije izmišljen radi zarade, već je izmišljen da bi promenio svet.

- Bitcoin će to učiniti poštujući korisnikovu bezbednost, privatnost i slobodu.

- Bitcoin se već koristi kao novac, na nekoliko načina na koji se novac može koristiti.

- Bitcoin nije nestabilan, njegova vrednost vremenom polako raste (odzumirajte).

- Bitcoin ima mnogo kopija i prevaranata koji će pokušati da vam prodaju svoju kopiju Bitcoin-a. Ne zavaravajte se lažnim Bitcoin-om baš kao što vas ne bi prevarili ni Lažnim Zlatom.

- Bitcoin će postati najveći prenos bogatstva u našem životu, tako da ćete možda želeti da ih uzmete pre nego kasnije.

- Ostanite skromni i skupljajte satošije.

-

@ 57d1a264:69f1fee1

2025-05-22 06:21:22

You’ve probably seen it before.

You open an agency’s website or a freelancer’s portfolio. At the very top of the homepage, it says:

We design for startups.

You wait 3 seconds. The last word fades out and a new one fades in:

We design for agencies.

Wait 3 more seconds:

We design for founders.

I call this design pattern The Wheel of Nothing: a rotating list of audience segments meant to impress through inclusion and draw attention through motion… for absolutely no reason.

Revered brand studio Pentagram recently launched a new website. To my surprise, the homepage features the Wheel of Nothing front and center, boldly claiming:

We design Everything for Everyone…before cycling through more specific combinations every few seconds.

Dan Mall, a husband, dad, teacher, creative director, designer, founder, and entrepreneur from Philly. I share as much as I can to create better opportunities for those who wouldn’t have them otherwise. Most recently, I ran design system consultancy SuperFriendly for over a decade.

Read more at Dans' website https://danmall.com/posts/the-wheel-of-nothing/

https://stacker.news/items/986392

-

@ 9ca447d2:fbf5a36d

2025-05-22 21:01:39

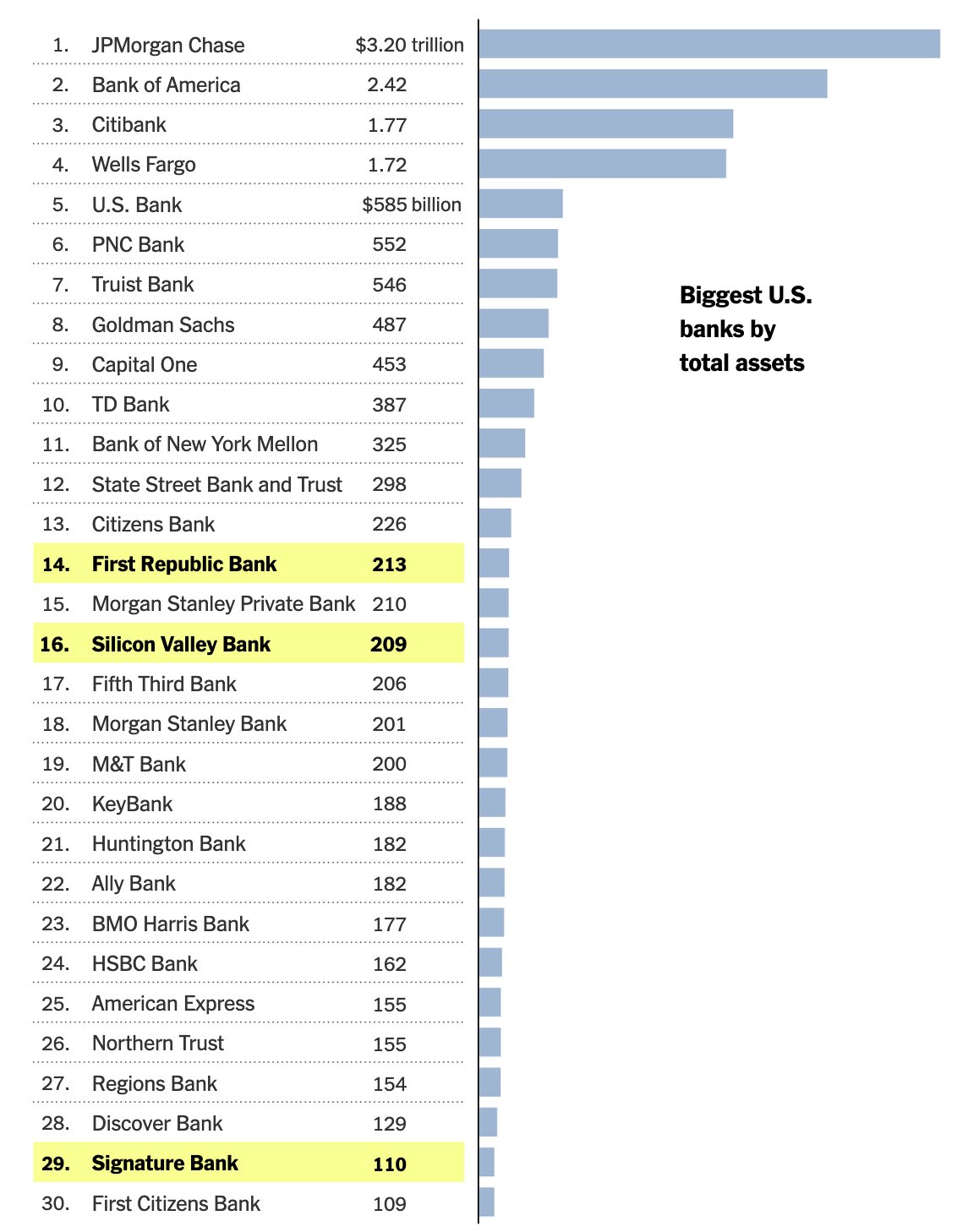

Tokyo-listed investment firm Metaplanet has officially surpassed El Salvador in bitcoin holdings after its biggest-ever single purchase of the scarce digital asset.

On May 12, 2025, the company announced it had bought 1,241 Bitcoin (BTC) for approximately $123.8 million, or ¥18.4 billion. The average price per coin was about $102,111, marking the firm’s largest purchase to date.

This latest buy brings Metaplanet’s total bitcoin reserves to 6,796 BTC, worth over $700 million.

Metaplanet on X

That puts Metaplanet ahead of El Salvador, the Central American nation that made headlines in 2021 for adopting bitcoin as legal tender. According to its National Bitcoin Office, El Salvador currently holds 6,174 BTC, worth roughly $642 million.

El Salvador bitcoin holdings — bitcoin.gob.sv

“Metaplanet now holds more bitcoin than El Salvador. From humble beginnings to rivaling nation-states, we’re just getting started,” said CEO Simon Gerovich on X after the company’s announcement.

The Japanese investment company started its bitcoin treasury strategy in April 2024 and has become the largest corporate holder of bitcoin in Asia and 11th globally. It aims to hold 10,000 BTC by the end of 2025.

Metaplanet is now the 11th largest corporate holder of bitcoin — BitcoinTreasuries

To fund these purchases, the firm has turned to bond issuances, including zero-percent bonds. In early May, Metaplanet issued $25 million worth of 0% bonds under its EVO FUND program to finance bitcoin buys without diluting shares or taking on traditional debt.

And Metaplanet’s strategy seems to be working. Its BTC Yield — a proprietary metric that measures bitcoin accumulation per share — is 38% for Q2 2025 so far. In previous quarters, the firm reported 95.6% in Q1 and a whopping 309.8% in Q4 2024.

The stock price has also gone up 1,800% since May 2024 and 51% in 2025 alone, currently trading above 550 JPY.

Metaplanet is often called “Japan’s MicroStrategy”, a reference to the U.S.-based company Strategy (formerly MicroStrategy) led by Bitcoin advocate Michael Saylor. Strategy is the world’s largest corporate bitcoin holder with over 568,840 BTC in its coffers, worth more than $58 billion.

Like Strategy, Metaplanet is using creative financing tools such as convertible bonds and non-dilutive bond issuance to build a big bitcoin treasury. These financial instruments give the company the ability to fund further bitcoin purchases without diluting shareholders’ value.

Metaplanet is buying bitcoin very rapidly. This has become a trend in the corporate world, where private companies are challenging nation-states in the digital asset space.

Unlike governments which face regulatory and political hurdles, corporations like Metaplanet can move quickly and decisively. Since 2020 over 80 publicly traded companies have collectively bought more than 632,000 BTC worth over $65 billion.

This is a fundamental shift in how companies manage their treasuries — moving away from cash or bonds and towards the digital scarcity that bitcoin presents.

This creates a new form of financial power where corporations can hold a significant portion of a finite asset, unlike fiat currencies which governments can print to infinity.

-

@ 7e6f9018:a6bbbce5

2025-05-22 16:33:07

Per les xarxes socials es parla amb efusivitat de que Bitcoin arribarà a valer milions de dòlars. El mateix Hal Finney allà pel 2009, va estimar el potencial, en un cas extrem, de 10 milions $:

\> As an amusing thought experiment, imagine that Bitcoin is successful and becomes the dominant payment system in use throughout the world. Then the total value of the currency should be equal to the total value of all the wealth in the world. Current estimates of total worldwide household wealth that I have found range from $100 trillion to $300 trillion. Withn 20 million coins, that gives each coin a value of about $10 million. <https://satoshi.nakamotoinstitute.org/emails/bitcoin-list/threads/4/>

No estic d'acord amb els càlculs del bo d'en Hal, ja que no consider que la valoració d'una moneda funcioni així. En qualsevol cas, el 2009 la capitalització de la riquesa mundial era de 300 bilions $, avui és de 660 bilions $, és a dir ha anat pujant un 5,3% de manera anual,

$$(660/300)^{1/15} = 1.053$$La primera apreciació amb aquest augment anual del 5% és que si algú llegeix aquest article i té diners que no necessita aturats al banc (estalvis), ara és bon moment per començar a moure'ls, encara sigui amb moviments defensius (títols de deute governamental o la propietat del primer habitatge). La desagregació per actius dels 660 bilions és:

-

Immobiliari residencial = 260 bilions $

-

Títols de deute = 125 bilions $

-

Accions = 110 bilions

-

Diners fiat = 78 bilions $

-

Terres agrícoles = 35 bilions $

-

Immobiliari comercial = 32 bilions $

-

Or = 18 bilions $

-

Bitcoin = 2 bilions $

La riquesa mundial és major que 660 bilions, però aquests 8 actius crec que són els principals, ja que s'aprecien a dia d'avui. El PIB global anual és de 84 bilions $, que no són bromes, però aquest actius creats (cotxes, ordinadors, roba, aliments...), perden valor una vegada produïts, aproximant-se a 0 passades unes dècades.

Partint d'aquest nombres com a vàlids, la meva posició base respecte de Bitcoin, ja des de fa un parell d'anys, és que te capacitat per posar-se al nivell de capitalització de l'or, perquè conceptualment s'emulen bé, i perquè tot i que Bitcoin no té un valor tangible industrial com pot tenir l'or, sí que te un valor intangible tecnològic, que és pales en tot l'ecosistema que s'ha creat al seu voltant:

-

Creació de tecnologies de pagament instantani: la Lightning Network, Cashu i la Liquid Network.

-

Producció d'aplicacions amb l'íntegrament de pagaments instantanis. Especialment destacar el protocol de Nostr (Primal, Amethyst, Damus, Yakihonne, 0xChat...)

-

Industria energètica: permet estabilitzar xarxes elèctriques i emprar energia malbaratada (flaring gas), amb la generació de demanda de hardware i software dedicat.

-

Educació financera i defensa de drets humans. És una eina de defensa contra governs i estats repressius. La Human Rights Foundation fa una feina bastant destacada d'educació.

Ara posem el potencial en nombres:

-

Si iguala l'empresa amb major capitalització, que és Apple, arribaria a uns 160 mil dòlars per bitcoin.

-

Si iguala el nivell de l'or, arribaria a uns 800 mil dòlars per bitcoin.

-

Si iguala el nivell del diner fiat líquid, arribaria a un 3.7 milions de dòlars per bitcoin.

Crec que igualar la capitalització d'Apple és probable en els pròxims 5 - 10 anys. També igualar el nivell de l'or en els pròxims 20 anys em sembla una fita possible. Ara bé, qualsevol fita per sota d'aquesta capitalització ha d'implicar tota una serie de successos al món que no sóc capaç d'imaginar. Que no vol dir que no pugui passar.

-

-

@ 51bbb15e:b77a2290

2025-05-21 00:24:36

Yeah, I’m sure everything in the file is legit. 👍 Let’s review the guard witness testimony…Oh wait, they weren’t at their posts despite 24/7 survellience instructions after another Epstein “suicide” attempt two weeks earlier. Well, at least the video of the suicide is in the file? Oh wait, a techical glitch. Damn those coincidences!

At this point, the Trump administration has zero credibility with me on anything related to the Epstein case and his clients. I still suspect the administration is using the Epstein files as leverage to keep a lot of RINOs in line, whereas they’d be sabotaging his agenda at every turn otherwise. However, I just don’t believe in ends-justify-the-means thinking. It’s led almost all of DC to toss out every bit of the values they might once have had.

-

@ b1ddb4d7:471244e7

2025-05-22 21:00:35

Starting January 1, 2026, the United Kingdom will impose some of the world’s most stringent reporting requirements on cryptocurrency firms.

All platforms operating in or serving UK customers-domestic and foreign alike-must collect and disclose extensive personal and transactional data for every user, including individuals, companies, trusts, and charities.

This regulatory drive marks the UK’s formal adoption of the OECD’s Crypto-Asset Reporting Framework (CARF), a global initiative designed to bring crypto oversight in line with traditional banking and to curb tax evasion in the rapidly expanding digital asset sector.

What Will Be Reported?

Crypto firms must gather and submit the following for each transaction:

- User’s full legal name, home address, and taxpayer identification number

- Detailed data on every trade or transfer: type of cryptocurrency, amount, and nature of the transaction

- Identifying information for corporate, trust, and charitable clients

The obligation extends to all digital asset activities, including crypto-to-crypto and crypto-to-fiat trades, and applies to both UK residents and non-residents using UK-based platforms. The first annual reports covering 2026 activity are due by May 31, 2027.

Enforcement and Penalties

Non-compliance will carry stiff financial penalties, with fines of up to £300 per user account for inaccurate or missing data-a potentially enormous liability for large exchanges. The UK government has urged crypto firms to begin collecting this information immediately to ensure operational readiness.

Regulatory Context and Market Impact

This move is part of a broader UK strategy to position itself as a global fintech hub while clamping down on fraud and illicit finance. UK Chancellor Rachel Reeves has championed these measures, stating, “Britain is open for business – but closed to fraud, abuse, and instability”. The regulatory expansion comes amid a surge in crypto adoption: the UK’s Financial Conduct Authority reported that 12% of UK adults owned crypto in 2024, up from just 4% in 2021.

Enormous Risks for Consumers: Lessons from the Coinbase Data Breach

While the new framework aims to enhance transparency and protect consumers, it also dramatically increases the volume of sensitive personal data held by crypto firms-raising the stakes for cybersecurity.

The risks are underscored by the recent high-profile breach at Coinbase, one of the world’s largest exchanges.

In May 2025, Coinbase disclosed that cybercriminals, aided by bribed offshore contractors, accessed and exfiltrated customer data including names, addresses, government IDs, and partial bank details.

The attackers then used this information for sophisticated phishing campaigns, successfully deceiving some customers into surrendering account credentials and funds.

“While private encryption keys remained secure, sufficient customer information was exposed to enable sophisticated phishing attacks by criminals posing as Coinbase personnel.”

Coinbase now faces up to $400 million in compensation costs and has pledged to reimburse affected users, but the incident highlights the systemic vulnerability created when large troves of personal data are centralized-even if passwords and private keys are not directly compromised. The breach also triggered a notable drop in Coinbase’s share price and prompted a $20 million bounty for information leading to the attackers’ capture.

The Bottom Line

The UK’s forthcoming crypto reporting regime represents a landmark in financial regulation, promising greater transparency and tax compliance. However, as the Coinbase episode demonstrates, the aggregation of sensitive user data at scale poses a significant cybersecurity risk.

As regulators push for more oversight, the challenge will be ensuring that consumer protection does not become a double-edged sword-exposing users to new threats even as it seeks to shield them from old ones.

-

@ 6ad3e2a3:c90b7740

2025-05-20 13:49:50

I’ve written about MSTR twice already, https://www.chrisliss.com/p/mstr and https://www.chrisliss.com/p/mstr-part-2, but I want to focus on legendary short seller James Chanos’ current trade wherein he buys bitcoin (via ETF) and shorts MSTR, in essence to “be like Mike” Saylor who sells MSTR shares at the market and uses them to add bitcoin to the company’s balance sheet. After all, if it’s good enough for Saylor, why shouldn’t everyone be doing it — shorting a company whose stock price is more than 2x its bitcoin holdings and using the proceeds to buy the bitcoin itself?

Saylor himself has said selling shares at 2x NAV (net asset value) to buy bitcoin is like selling dollars for two dollars each, and Chanos has apparently decided to get in while the getting (market cap more than 2x net asset value) is good. If the price of bitcoin moons, sending MSTR’s shares up, you are more than hedged in that event, too. At least that’s the theory.

The problem with this bet against MSTR’s mNAV, i.e., you are betting MSTR’s market cap will converge 1:1 toward its NAV in the short and medium term is this trade does not exist in a vacuum. Saylor has described how his ATM’s (at the market) sales of shares are accretive in BTC per share because of this very premium they carry. Yes, we’ll dilute your shares of the company, but because we’re getting you 2x the bitcoin per share, you are getting an ever smaller slice of an ever bigger overall pie, and the pie is growing 2x faster than your slice is reducing. (I https://www.chrisliss.com/p/mstr how this works in my first post.)

But for this accretion to continue, there must be a constant supply of “greater fools” to pony up for the infinitely printable shares which contain only half their value in underlying bitcoin. Yes, those shares will continue to accrete more BTC per share, but only if there are more fools willing to make this trade in the future. So will there be a constant supply of such “fools” to keep fueling MSTR’s mNAV multiple indefinitely?

Yes, there will be in my opinion because you have to look at the trade from the prospective fools’ perspective. Those “fools” are not trading bitcoin for MSTR, they are trading their dollars, selling other equities to raise them maybe, but in the end it’s a dollars for shares trade. They are not selling bitcoin for them.

You might object that those same dollars could buy bitcoin instead, so they are surely trading the opportunity cost of buying bitcoin for them, but if only 5-10 percent of the market (or less) is buying bitcoin itself, the bucket in which which those “fools” reside is the entire non-bitcoin-buying equity market. (And this is not considering the even larger debt market which Saylor has yet to tap in earnest.)

So for those 90-95 percent who do not and are not presently planning to own bitcoin itself, is buying MSTR a fool’s errand, so to speak? Not remotely. If MSTR shares are infinitely printable ATM, they are still less so than the dollar and other fiat currencies. And MSTR shares are backed 2:1 by bitcoin itself, while the fiat currencies are backed by absolutely nothing. So if you hold dollars or euros, trading them for MSTR shares is an errand more sage than foolish.

That’s why this trade (buying BTC and shorting MSTR) is so dangerous. Not only are there many people who won’t buy BTC buying MSTR, there are many funds and other investment entities who are only able to buy MSTR.

Do you want to get BTC at 1:1 with the 5-10 percent or MSTR backed 2:1 with the 90-95 percent. This is a bit like medical tests that have a 95 percent accuracy rate for an asymptomatic disease that only one percent of the population has. If someone tests positive, it’s more likely to be a false one than an indication he has the disease*. The accuracy rate, even at 19:1, is subservient to the size of the respective populations.